![]()

Kopo Kopo provides tools to facilitate mobile payments through existing platforms, focusing on merchant payments that enable small and medium businesses to accept mobile money payments from their customers. Having now reached over 12,500 merchants in East Africa, the team aims to expand to new markets, working with mobile money providers interested in rolling out merchant payments.

Year Launched : 2011

Business Model : Consumer (merchant), B2B (mobile-money service provider)

Targeted Device : Basic/Feature Phone, Smart Phone, PC/Laptop, Tablet

Primary Delivery Technology : SMS/USSD, Web

Products & Services : Merchant Payments and Other Services (payments)

Markets Deployed In : Kenya, Tanzania, Rwanda

Estimated Number of Users : 12,500 merchants

Background and opportunity:

The East African country of Kenya is home to the most advanced mobile money market in the world. In June 2013, Safaricom’s M-PESA service accounted for approximately 34% of global transactions by value. By September 2013, just over 48% of the adult population used M-PESA on a monthly basis. This growth has been continuing since the launch of M-PESA in 2007, but despite its growing popularity for money transfer and mobile phone airtime purchase, in 2011 Kopo Kopo calculated that fewer than 0.01% of businesses in Kenya had an M-PESA merchant account. This meant there was a latent opportunity to enable enterprises to capitalize on the increasing familiarity customers had with mobile money when doing business with them.

Objective:

The Kopo Kopo team set out to provide tools to small and medium businesses to enable them to accept mobile money payments and to take advantage of related value added services to help them grow and prosper.

Results:

Kopo Kopo have acquired more than 12,500 merchants in East Africa. Since its Kenyan launch in March 2012, the company has achieved a consistent increase in transaction volumes. As of March 2014, it was generating more than USD 3 million in transaction volumes per month. The number of transactions merchants make per month is around two to three times what traditional card payment acquirers expect.

Lessons Learnt:

Communication with customers is key; use technology to keep even the smallest customers updated and engaged, especially during the service set up period Above the line marketing lays an important foundation in direct sales Monitor your direct sales team to ensure their pitches are accurate and to limit fraud

Impact:

Kopo Kopo see the service as supporting the growth and prosperity of enterprises and therefore the economies in which they operate, by fundamentally changing the way business is conducted.

Approach:

The Kopo Kopo team had previously worked extensively in the microfinance industry, which informed its original approach to offer a solution to reduce the inefficiencies caused by using cash and paper-based administration systems in microfinance institutions.

However, when talks with Kenyan partner Safaricom began in late 2011, the Kopo Kopo team identified a bigger opportunity. Although Safaricom had very successfully deployed its mobile money service M-PESA to 7 out of 10 consumers across Kenya, fewer than 0.01% of businesses in Kenya had an M-PESA merchant account. At the same time, in the non-mobile money world, typical users were making around five merchant payments a day. Kopo Kopo saw this as a chance to develop and offer the tools necessary to enable businesses to accept payments via the increasingly popular mode of payment, M-PESA.

Kopo Kopo aimed to realize this opportunity by proving their hypothesis that thousands of merchants would be willing to accept payments by mobile money. The first six months of work was dedicated to proving this hypothesis, which required capturing and communicating the value proposition for accepting the electronic payment method from M-PESA wallets.

Once proved, Kopo Kopo could offer Safaricom an end-to-end solution for their merchant business. This enabled Kopo Kopo to market M-PESA acceptance to merchants; acquire and on-board those merchants; train and engage with their software tools, and ultimately use the information gathered from this process to upsell to merchants new products and services based on their payment history and payment behaviour. The business model shares the costs of investing in merchant acquisition and management, and also shares the revenues that are generated through the M-PESA transactions. This cost-and-revenue share business model now forms Kopo Kopo’s primary business model in East Africa.

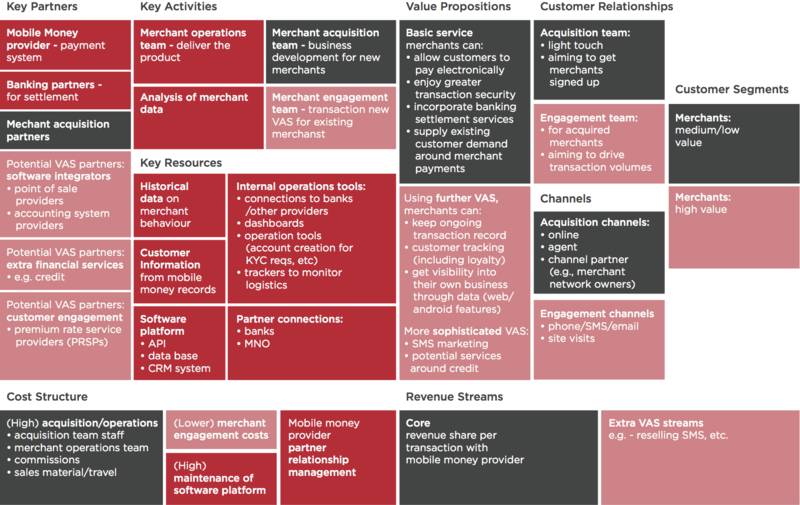

Initially Kopo Kopo focused on driving merchant acquisition (i.e. driving as many monthly merchant sign ups to the service as possible). The focus on acquisition has now shifted to increasing monthly merchant transaction volumes (i.e. usage). This corresponds to a distinction Kopo Kopo draws between two merchant customer segments (Figure 1).

Figure 1: Kopo Kopo’s business model around merchants

Source: GSMA Mobile for Development

(Note: Dark grey represents aspects of the model relating to serving merchants in the lower value segment and light red represents serving higher value merchants.)

Use and value of data:

Kopo Kopo have a wide range of merchant customers on their system, from large book stores to small corner shops in Nairobi, and from agro-vets in the remote, rural regions of Kenya to large industrial distributors in the country’s second-city Mombasa. Each of these different customer types uses the service in different ways. The challenge is to understand these differences, and how to serve the different groups most effectively.

From a purely commercial perspective, the revenue share agreement with Safaricom means that Kopo Kopo’s business is dependent upon transaction volumes. Therefore, this is the most critical operational metric. An active merchant is defined as one who conducts one transaction per month, but activity is often higher. The company says it is seeing two to three times the number of transactions traditional card payment acquirers would get, so it feels its offer to the merchants is appropriate and successful.

However, Kopo Kopo also employ a ‘break-even analysis’, which examines merchant acquisition costs versus the lifetime value of the merchants. The company has built dashboards internally so that it understands how much it costs to acquire a merchant, and in return what that merchant will provide in lifetime value. Lifetime value includes average revenue per merchant, activity rates, and transaction size. These are all operational metrics Kopo Kopo look at in order to understand how quickly they can recoup their acquisition costs.

The organization also tries to predict the lifetime value of their customers by forecasting the likelihood of a merchant becoming a high volume transactor. This can involve segmenting their merchant customer base by region, examining different merchant category codes, size of the business, what kind of bank accounts merchants have, and with whom they bank. This analysis allows them to identify merchants of the highest likely lifetime value, and help the team understand how to most effectively recoup acquisition costs.

It is vital to understand the right channels to use for customer acquisition. Kopo Kopo’s customer channels include an online channel, a sales force channel, a direct sales channel, and a merchant network partner channel. Each of these acquisition structures have different costs, so it is important for Kopo Kopo to understand which different kinds of acquisition channels are most effective in light of the lifetime value they produce.

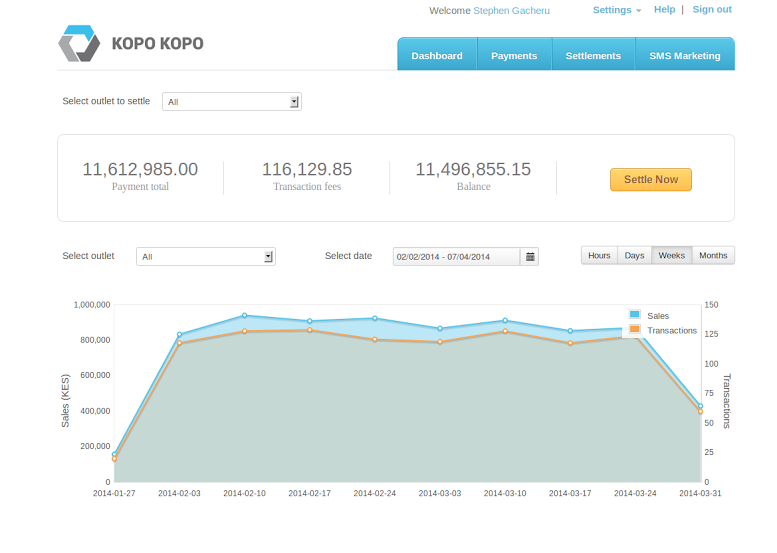

Figure 2: Kopo Kopo merchant dashboard snapshot

Source: Kopo Kopo

Scalability:

For Kopo Kopo’s business overall, scale involves penetrating new markets where there is potential to enable merchant payments via mobile money. They actively seek to do this on an ongoing basis.

For its business activities, scale relates to both mass-market acquisition, i.e. the number of merchants signed up, and driving merchant activity: the number of transactions per merchant.

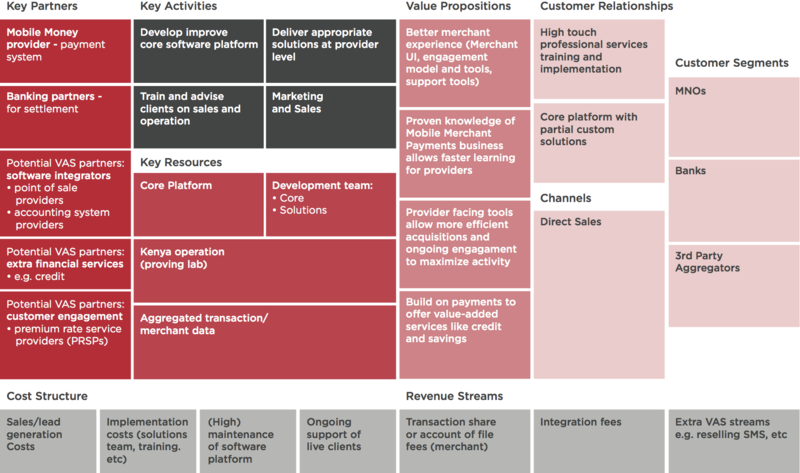

Figure 3: Kopo Kopo’s business model around mobile money providers

Source: GSMA Mobile for Development

Different strategies depend on the position of a given partner. If the mobile money service provider’s goal is to capture mindshare of customers, then Kopo Kopo will aim to sign up as many merchants in as short a timeframe as possible. On the other hand, an ARPU driven strategy (i.e. slowly acquiring merchants with high transaction volumes) will look quite different (Figure 3).

According to the company, the ideal merchant roll-out strategy is a hybrid model. This is also reflected in the marketing efforts involved. Above-the-line marketing drives awareness and use of the service by the end consumer. On the other hand, actual acquisitions need targeted, below-the-line efforts to focus on merchants likely to become active users. This strategy avoids the acquisition of a high number of merchants who do not know how to incentivize consumers, or do not have enough customers interested in using the services at their store.

While above-the-line techniques are important to drive awareness, they have not been effective at targeting specific segments. Kopo Kopo see that acquiring active merchants is hard, particularly in developing markets where e-payments acceptance is very low. Since above-the-line and other mass-market drives alone will not bring you activity, providers have to build profiles of active merchants and target those on the ground to improve activity rates. After that, above-the-line campaigns help to drive more transactions.

Partnerships:

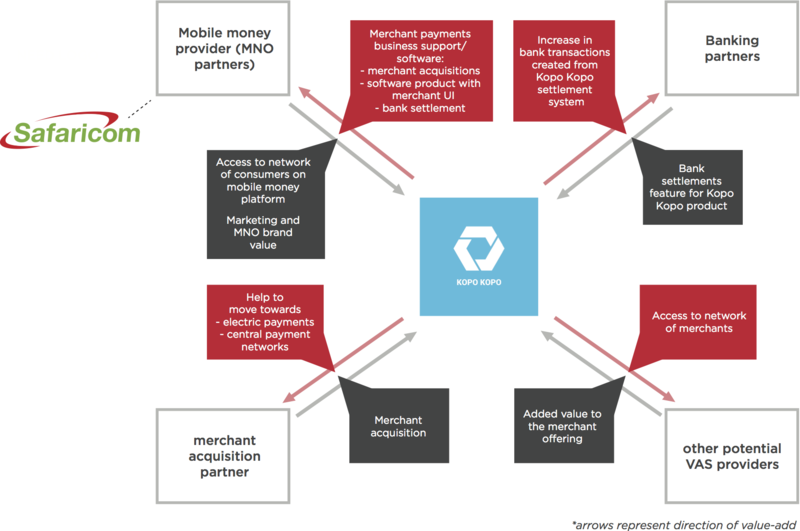

Kopo Kopo’s main partnerships are with mobile money providers, banking partners, merchant acquisition partners and other potential value added services (VAS) providers, such as premium rate service providers (Figure 4).

Figure 4: Kopo Kopo’s network of partners*

Source: GSMA Mobile for Development

Kopo Kopo use the term ‘upstream partners’ to denote those who actually have a mobile money platform and are enabling the transactions that Kopo Kopo facilitates and encourages through the tools it offers. Therefore, partnerships with mobile money payment provider are integral to its business model.

The organization’s value proposition to mobile money providers centers on extending the ‘e-money loop,’ which is the activity mobile money users conduct between putting cash into the e-wallet and taking cash out of it. Often in mobile money, this loop is one to one at best, containing minimal transactions: e.g. a son will put money into the system, send it to his mother, who will then take this cash out of the system. Certain actions, e.g. sending the money, cost a small fee and so generate revenue for the mobile money provider. Therefore, by increasing the ratio of transactions to cash-ins – that is, increasing the number of transactions a customer makes after putting cash in the e-wallet, Kopo Kopo offers the mobile money provider a chance to increase revenues by encouraging mobile money users to make multiple transactions at different merchants before cashing out, if they do so at all.

Banks remain critical partners as Kopo Kopo’s system allows bank settlement services for merchants. The organization have also developed an application programming interface (API) that works with software integrators, which may be a point of sale provider, an accounting system, or anything that requires an API to the transaction information into their system.

Kopo Kopo also work with premium rate service providers (PRSPs) to give merchants opportunities to create targeted SMS offers. There is strong potential for further value added services centered around the merchant, including access to credit, and other financial services.

On the merchant acquisition side, Kopo Kopo partner with those who already have big merchant networks, or are in the process of building merchant networks, in order to expand their reach.

Challenges:

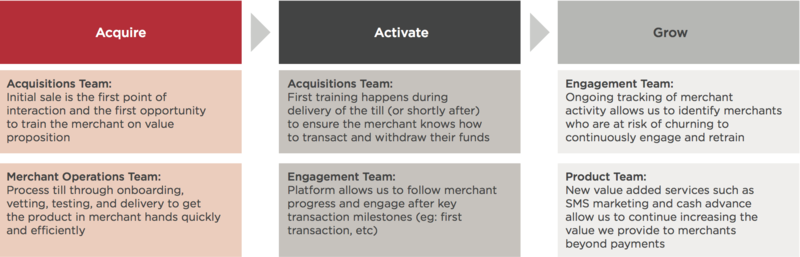

The biggest challenges for Kopo Kopo have been around providing the tools to engage a merchant sufficiently to achieve first time use. In early stage pilots with Safaricom, turnaround times from sale (i.e., merchant acquisition) to a processed application (allowing a merchant to actually use the system) could reach three weeks. The company found that in that time, merchant interest had waned.

Kopo Kopo first developed internal tools to drive this time down from three weeks to less than one week. The company then developed software to keep the merchant constantly informed regarding its application status and therefore keep the service top-of-mind. Kopo Kopo report that merchant customers were often surprised and pleased to receive an SMS or phone call update: they were not accustomed to corporates caring about them as customers and the communications made them feel valued. The lesson arising from overcoming this challenge was that regular communication with the customer—which technology allows to be automated and low cost—is vital (Figure 5).

Figure 5: Kopo Kopo merchant journey

Source: GSMA Mobile for Development

Kopo Kopo encountered challenges in initial merchant acquisition, as awareness of the potential of mobile payments was low. However, once above-the-line marketing was conducted by Safaricom, Kopo Kopo found the resultant increase in awareness facilitated sales. This showed the benefits of above-the-line marketing by a well-known brand. That being said, Kopo Kopo stress that a lesson in aquiring active merchants is to regard this as a journey (see Figure 5), not a one time task.

In addition, managing a geographically distributed sales force presented problems to overcome. Initially, Kopo Kopo found that some agents were misleading merchants as to the nature of the service to which they were signing up in order to hit targets, which led to low activity numbers and displeased merchants. Therefore Kopo Kopo developed specific tools in the form of sales management and sales fraud management dashboards to help monitor the consistency of marketing across different channels.

Future Plans:

Going forward, Kopo Kopo is looking to expand into new markets and partner with mobile money service providers with potential to roll out merchant payments and is currently in discussion with providers across markets.

The company mainly seeks mobile money providers which have already reached around 1 million subscribers, as this means merchants are more likely to be aware of and open to using mobile money payments.

Kopo Kopo understand that the traditional focus around mobile money agent networks is to first get customers on the network, and then consider additional use cases like merchant payments. However, it believes that in some cases, there are benefits to introducing merchants much earlier onto the network, to support new mobile money users in interacting with the new mode of transfer and payment.

This document was originally produced as part of the former Mobile for Development Impact programme.