It was great to be back at the Kigali Convention Centre for GOGLA and Solar Plaza’s Unlocking Solar Capital Africa event on 7 – 8 November 2018, just a few months after the GSMA held its Mobile 360 – Africa event there. It was the perfect setting to consider what the current status of financing in the solar industry means for the mobile industry. Here are my four high-level takeaways and questions in a snapshot, some of which deserve more in-depth discussion and research than this blog alone can offer.

What does the state of financing in the off-grid solar industry mean for the mobile industry?

1. As the off-grid solar industry expands through value-chain specialisation, the GSMA’s Instant Payment Notification Hub (IPN Hub) is a crucial bridge to new markets.

The pay-as-you-go (PAYG) solar industry has seen a significant shift in the last one to two years towards more value chain specialist companies, rather than new companies pursuing vertical integration to manage it all – product, sales, financing and customer support. This means there are more locally-based distribution companies who can master sales with local knowledge, but may struggle to get the attention of a mobile operator should they want to integrate with the operator’s mobile money service. The IPN Hub helps bridge this gap by providing a single platform for the real-time notification of mobile money payments that is essential for this pre-paid service model. Through a single integration to the IPN Hub, energy service providers (and a range of other service providers) can receive payment notifications in real-time from multiple mobile operators– across multiple markets.

In Rwanda, the IPN Hub has processed notifications for nearly two million payment transactions received through MTN and AirtelTigo for PAYG solar home system companies BBOXX and Zola. The IPN Hub is scaling up with more updates coming soon, and those looking to connect can reach us at [email protected].

2. If the ‘strange beast’ that is the original PAYG solar business model continues to have finance split from retail and distribution, what does this mean for mobile operators?

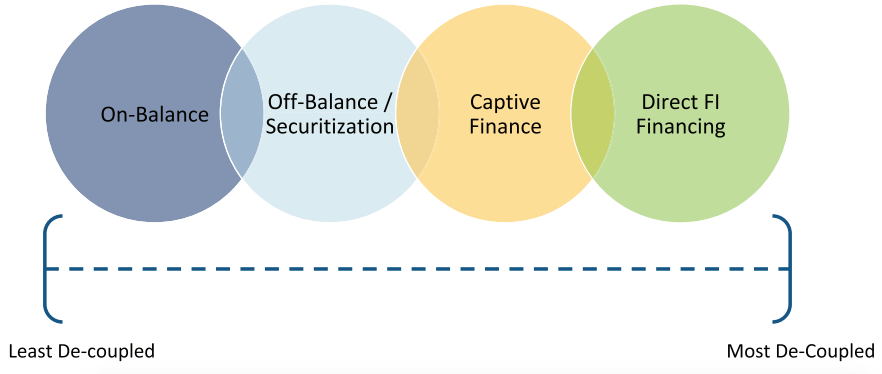

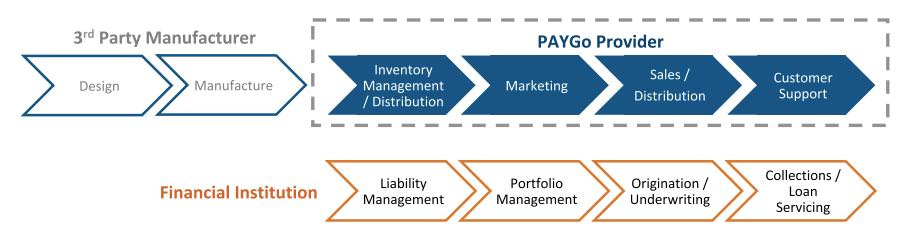

In January 2018, CGAP published analysis of vertically integrated PAYG solar companies, i.e. the strange beasts, that combined retail and financing operations, and how they could analyse their various operations, with an eye towards unlocking new financing models. In their most recent piece, ‘Taming the Strange Beasts: Servicing and the Future of PAYGo’, launched during this event, they look at receivable financing models (see Figure 1 from the report below), across a spectrum of financial decoupling. In the least decoupled model, the servicing and ownership of the loans stay on the balance sheet of the PAYG company (keeping the strange beast structure as they manage the product, sales and service). In the middle, PAYG companies can either do off-balance sheet financing through securitisation, or create captive finance companies (FinCos) which are subsidiaries of the PAYGo Group and act as a bank financing the consumers on its own balance sheet. In the most de-coupled model, the entire consumer finance piece is outsourced to an external bank or other finance institution. Figure 2 gives a visualisation of how the ‘strange beast’ might be segmented in that model, with the PAYGo company managing distribution and customer care, while finance is outsourced.

Figure 1: CGAP’s spectrum of financial decoupling for receivables financing options

Figure 2: CGAP’s proposed ‘PAYGo 3.0’ company structure in which financing can be unbundled

So, what does this evolution mean for mobile operators? This largely depends on the level of involvement the mobile operator has in the partnership. For those mobile operators who are ambitiously launching their own PAYG solar businesses, responsible for retail as well as financing, the two most de-coupled models (captive finance with a subsidiary and external financing) could be a very good fit, allowing them to isolate financial risk from their core business. Though, of course, a mobile operator setting up a financial lending subsidiary could have its own challenges with regards to regulation and beyond.

As the Mobile for Development (M4D) Utilities Innovation Fund is currently supporting a few mobile operators to launch their own PAYG solar businesses, including Orange Madagascar and the Afghan Wireless Communications Company, it will be interesting to see how their financial structure evolves with regards to CGAP’s suggested framework.

3. As the attention on investor exits grows, alongside increased mobile operator interest in off-grid energy, will we see mobile operators investing more or even acquiring more mature companies?

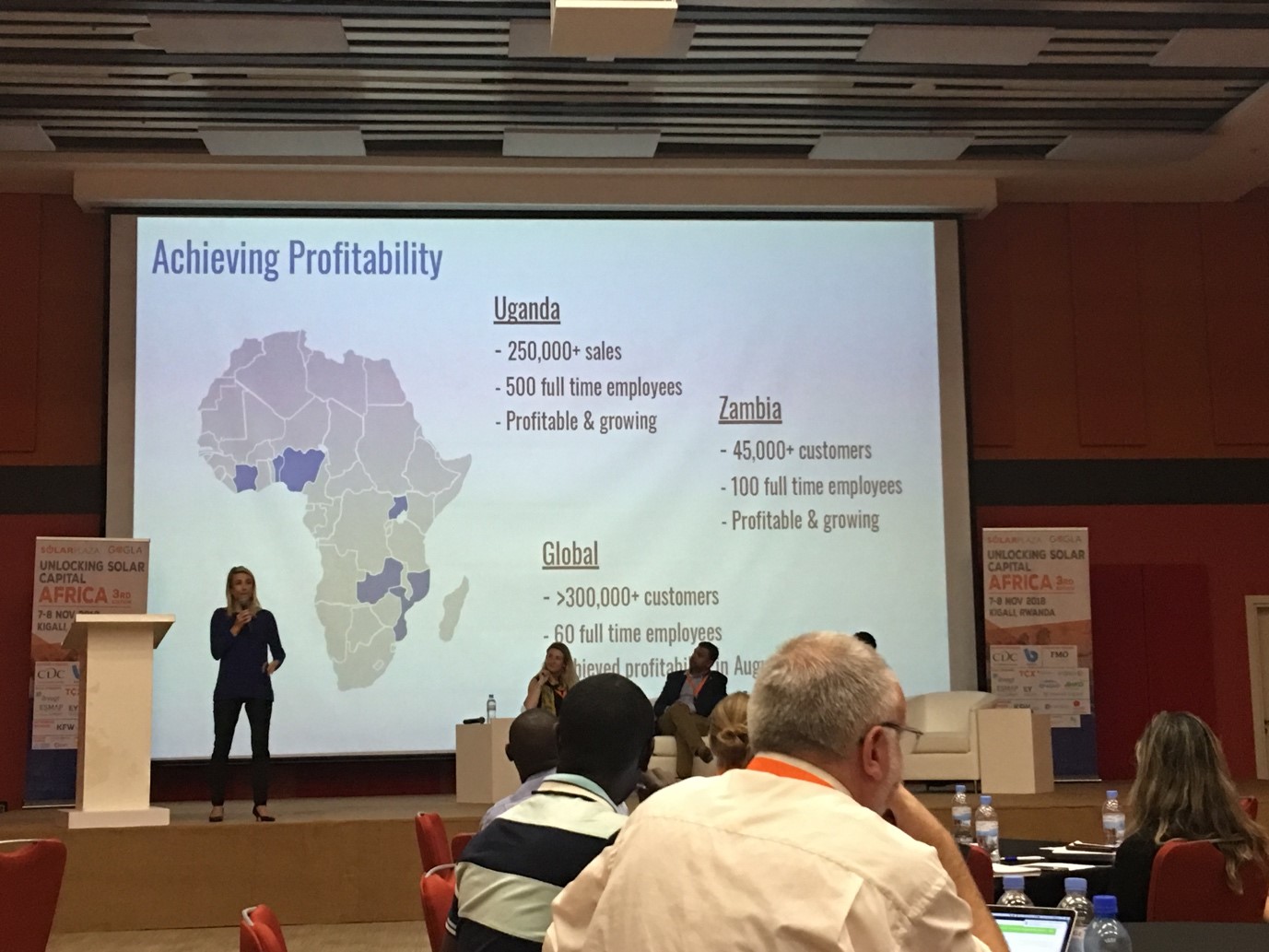

Several panels at the Unlocking Solar Capital Africa conference touched on exits, with most panellists saying that it’s important to consider these options early in order to free-up and recycle what early stage capital has already gone into the market. At the same time, some large utility organisations have invested significantly in this space. EDF, an international Energy Company invested in BBOXX, Zola and M4D Utilities grantee SunCulture. In October 2017, ENGIE announced its acquisition of solar home systems company Fenix International. This acquisition, marking the first exit of its kind in the industry, was also a proud moment for our programme, which provided Fenix International a grant in 2013 to work with MTN Uganda on growing the sales of their PAYG solar home system.

Fenix CEO Lyndsay Handler presents Fenix’s path to profitability.

This trend raises some further questions which would require more in-depth examination but which are worth stating – will there be more investments like these anytime soon? Given the more active role that some mobile operators are playing in this industry, could mobile operators make such an acquisition?

4. Consumer protection is essential for the PAYG solar industry, just as it is for mobile operators.

In April this year, the GSMA Mobile Money Certification was launched. The certification is a global initiative to bring safer, more transparent, and more resilient financial services to mobile money users around the world. Among its core principles are customer service, data privacy, quality of operations, and transparency – all related to consumer protection, and all equally important to the PAYG solar industry. The conference heard from several PAYG solar companies which are already developing robust internal policies, and investors that include this as part of their due diligence. In this context, GSMA is pleased to be supporting GOGLA in its development of consumer protection principles for the off-grid solar industry, by discussing how those used in the mobile money industry could apply. Of course, it’s not lost on the GSMA and its members that the conduct of PAYG solar companies will ultimately also reflect on the mobile operators providing the payment channels and more. Together these industries can add great value to one-another, yet they also risk negatively impacting the other if consumer protection is not of equal importance for both.

I would like to end this blog by thanking GOGLA and SolarPlaza for another highly relevant edition of the Unlocking Solar Capital Africa event and inviting GSMA to share its work at the event’s Insights booth.

This initiative is currently funded by the UK Department for International Development (DFID), the Scaling Off-Grid Energy Grand Challenge for Development and

supported by the GSMA and its members.