In this blog post, I want to share some insights on the opportunities and challenges for mobile money in the Middle East and North Africa region (MENA), based on actual facts and figures. Over the next few weeks, regional experts will also share their perspectives on the potential for mobile money in MENA in a series of blog posts.

As part of my new role within the GSMA Mobile Money team, I recently started to focus my work on the development of mobile money in the MENA. Over the last couple of months, I had the opportunity to meet with a number of public and private sector players to review the state of mobile money in this region and discuss future perspectives. While MENA [1] accounts for less than 10% of mobile money active accounts globally, there is momentum to accelerate the development of mobile money services in the region.

The mobile money opportunity in MENA: What does the financial access landscape look like in MENA?

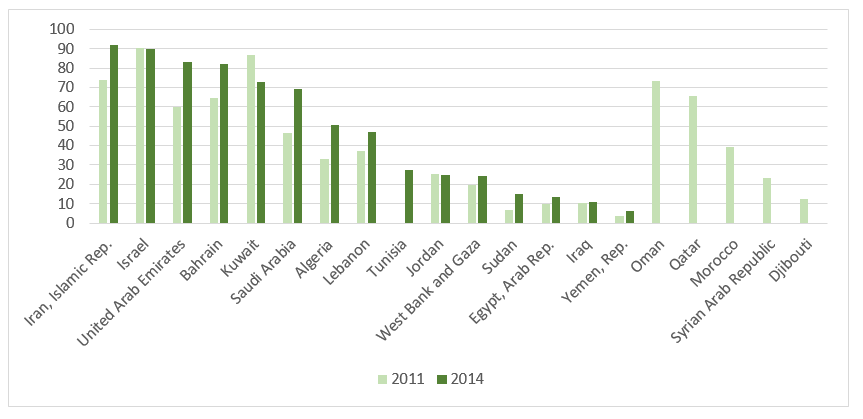

According to the World Bank’s Global Findex, in 2014, the percentage of adults with an account at a financial institution has reached 46% in the region, up from 35% in 2011 [2]. While this is an encouraging evolution, it means that the majority of adults in MENA remain unbanked. However, regional averages mask stark variations across countries:

- In Iran, Israel, UAE and Bahrain, more than 80% of adults have an account at a financial institution, as opposed to less than 20% in Yemen, Iraq, Egypt and Sudan.

- In Algeria, Bahrain, Iran, Saudi Arabia and the UAE, account penetration jumped by over 10 percentage points between 2011 and 2014, while it significantly decreased in Kuwait, and remained stable in Iraq, Israel and Jordan.

Account at a financial institution (% age 15+)

Source: World Bank’s Global Findex

Key segments and use cases

A lack of access to financial services appears to be particularly strong for three key groups:

- Unbanked women: Across MENA, 136 million adult women don’t have an account at a financial institution. [3] While a gender gap in mobile ownership is also prevalent in some countries, we found that the gap in access to financial services is typically much higher. For example in Egypt, the gender gap in account ownership reaches 49% [4], while the gap in mobile ownership stands at 2%. [5] Similarly in Jordan where the gender gap in mobile ownership is significant (21%), the gender gap in account ownership is more than twice as high (53%).

- Migrant workers: Migrant workers can represent a particularly large segment of the population in the Gulf, where many expatriates have joined the industrial work force. In the UAE for example, they represent 84% of the population. [6] These people transfer money regularly to their relatives back home and would strongly benefit from more convenient, transparent and cost-effective money transfer solutions like mobile money.[7]

- Refugees: In countries such as Jordan, where refugees represent the majority of international migrants, mobile money services could significantly help increase financial inclusion as well as access to other basic services such as education or healthcare.[8] Women and children, who make up 80% of Jordan’s Syrian refugee population, are particularly vulnerable, and suffer from limited opportunities to access safe spaces or general services.[9]

Considering that mobile penetration is above 100% in most countries of the region [10], mobile money may represent a strong opportunity to increase financial inclusion in MENA.

Finally, with the strong development of online shopping in MENA where cash-on-delivery remains the most prevalent payment mechanisms, e-commerce can also represent a strong use case for mobile money among high-end customers. In 2012, US$3.2 billion was spent by online shoppers in the GCC. Recent research indicates that the UAE, Saudi Arabia and Qatar are the regional leaders in mobile online commerce, with mobile accounting for 10% of all online transactions in these markets. This figure is forecast to increase to 20% by 2015.[11]

How can we accelerate the development of mobile money in MENA? The state of mobile money in MENA

Today, there are 15 live mobile money services in MENA. While this represents only a small share of the 261 live services globally, we are aware of another 15 planned services, which account for 15% of planned services globally.[12] At the end of December 2014, the 15 live mobile money services in MENA totaled 38 million registered mobile money accounts, of which 8.5 million were active.[13] This is less than 10% of active mobile money accounts globally.[14]

While mobile network operators are showing a strong interest to roll out mobile money services across the region, as indicated by the fact that there are more planned services than live services in MENA, a number of barriers have been slowing down their efforts.

Increasing focus and investments on mobile money services

In several markets across MENA, mobile money exists alongside other mobile payments solutions such as mobile banking, mobile wallets, and direct carrier billing.[15] While this shows operators’ appetite to move into the mobile payments space, there is also a risk that mobile money services do not receive sufficient focus nor investments[16], as providers are trying to push multiple mobile payment solutions in parallel.

On the consumer side, the proliferation of different mobile payment services may be confusing, resulting in low levels of adoption. For mobile money to succeed, stronger focus and higher levels of investments will be required to ensure a quick and solid customer take up.

Developing more enabling regulatory frameworks across the region

A growing body of evidence is showing that enabling mobile money regulation is critical for the development of the market and to achieve financial inclusion.[17]

- Allowing non-banks to participate in mobile money– In most countries of the region, financial sector regulators haven’t yet enacted the reforms to allow non-banks to launch mobile money services, the same reforms that have allowed other countries worldwide to expand the availability of payment services and other financial services and foster the development of more efficient and inclusive financial sectors. In Algeria and Iraq for example, the lack of a regulatory framework for mobile money has slowed down the development of mobile money [18]. In March 2014, the Central Bank of Jordan was the first regulator in the region to establish a non-discriminatory regulatory framework that allows both banks and non-banks to participate in mobile money.

- Promoting interoperability without mandating – Service providers and policymakers should also work together to understand different types of interoperability, including the benefits, costs, and risks. Policymakers shall enable market-led solutions, ensuring that interoperability brings value to the customer, makes commercial sense, is set up at the right time, and regulatory risks are identified and mitigated. Unfortunately, in several countries in MENA, regulators have been mandating interoperability without conducting proper analysis of the costs and benefits for implementing interoperability with service providers. In fact, Morocco is the only country in MENA where non-banks – including mobile network operators – are allowed to issue e-money under an enabling regulatory framework.

In order to accelerate the adoption of mobile money in MENA, the GSMA is strengthening its Mobile Money team with dedicated resources for the region. As we continue to gather insights on mobile money in MENA, please get in touch to share your stories, either by posting comments below or by emailing me: [email protected]

Notes:

[1] The following countries have been included in the MENA region for our analysis: Algeria, Bahrain, Djibouti, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Qatar, Saudi Arabia, West Bank & Gaza, Sudan, Syria, Tunisia, UAE and Yemen.

[2] Based on countries in MENA where data was available for both 2011 and 2014: Algeria, Bahrain, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Saudi Arabia, Sudan, UAE, West Bank & Gaza, and Yemen.

[3] World Bank’s Global Findex, 2014

[4] World Bank’s Global Findex, 2014

[6] International migrants represent the majority of the population in Bahrain (54.7%), Kuwait (60.2%), Qatar (73.8%) and the UAE (83.7%). In fact, the UAE have the second highest percentage globally, and Qatar ranks fourth. United Nations, Department of Economic and Social Affairs (2013), available here.

[7] The median cost of sending USD 100 internationally using mobile money is USD 4, less than half the average cost of sending money globally via traditional money transfer channels (9% of the face value on average). “2014 State of the Industry – Mobile Financial Services for the Unbanked”, GSMA (2015)

[8] Refugees represented the majority of international migrants in 2013 in the following countries: Jordan (87.1%), Lebanon (56.4%), Syria (89.1%) and Yemen (66.5%). Jordan and Syria were actually the countries where the two highest percentages globally in 2013. United Nations, Department of Economic and Social Affairs (2013), available here.

[9] “Gender-based violence and child protection among Syrian refugees in Jordan, with a focus on early marriage”, UN Women (2013)

[10] GSMA Intelligence

[11] GSMA 2014 mobile Economy Report for the Arab States

[12] GSMA Mobile Money Tracker

[13] On a 90-day basis

[15] Mobile network operators in MENA have quickly recognized the opportunity to move into the payments space, and they have tried different models:

- Several operators offer mobile banking solutions, which allow operators to support banks to develop their digital payment channels through mobile.

- Another way for operators to support the development of mobile payments is to launch mobile wallets. These wallets are mobile applications which allow its users to access their different accounts (virtual cards, mobile money accounts, bank accounts) directly from their mobile to conduct payments. However, this model doesn’t allow operators to address the unbanked and underbanked segments properly.

- Of all models, mobile money is best suited to meet the needs of unbanked and underbanked people in MENA. In contrast to mobile banking, it allows unbanked and underbanked people to access a range of financial services directly from their mobile. Compared to carrier billing, mobile money has a stronger value proposition for unbanked customers as it goes beyond online payments of certain digital goods and services.

- Through direct carrier billing, any mobile subscriber can buy digital goods and services using airtime, by adding the cost of the purchase directly to their mobile bill. While this model is quite popular among unbanked mobile subscribers in some markets, it has a number of significant drawbacks. In particular, there are strong limitations on the type and value of goods that can be purchased. Finally, direct carrier billing is by nature limited to payments and as such, doesn’t provide the opportunity for its users to access other financial services such as transfers, savings, credit and insurance.

[16] Mireya Almazan and Nicolas Vonthron (2014), “Mobile Money Profitability: A Digital Ecosystem to Drive Healthy Margins”, GSMA MMU

[17] Simone di Castri (2015), “Is regulation holding back financial inclusion? A look at the evidence”, GSMA MMU blog.

[18] “Mobile money challenges in Iraq”, available here.