This is the second of a two-part blog series in conjunction with Bankable Frontiers Associates (BFA). The first blog can be read here.

In our last blog, we considered the fertile conditions for scaling mobile person-to-government (P2G) payments in Ghana, and the barriers to realising this potential. To drive change, all stakeholder groups need to appreciate the advantages and align towards this common goal. What specific benefits can mobile P2G payments unlock for consumers, government ministries, departments and agencies (MDAs) and mobile money providers?

Benefits for citizens: cost savings and better user experience

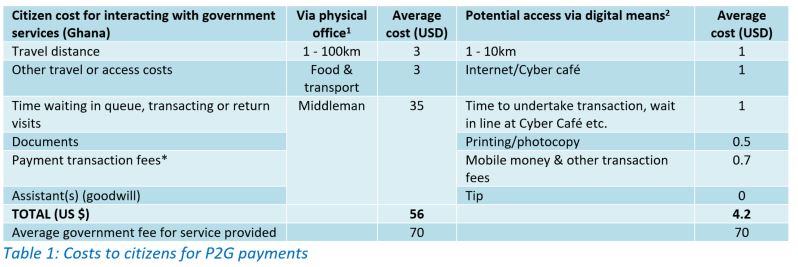

Citizens in Ghana could reduce their expenditure on P2G transactions by 90 per cent by shifting to digital, in addition to significantly saving time, as shown in Table 1 below.

Second, mobile P2G payments have the potential to significantly enhance user experience when made alongside services offered digitally on the e-Services platform. Unfortunately, this benefit is currently not recognised by many Ghanian citizens. Owing to limited knowledge and understanding of the e-Services and e-Payments portals, and complicated physical processes, many citizens could not imagine conducting the transaction online or without a middleman and do not actively seek out alternatives.

It seems unlikely that there will be major uptake of mobile money and other digital government payments until the following actions are considered:

- Streamlining the process to improve user experience and payment i.e. by reducing the need to physically visit the government office at any point in the process, therefore encouraging the uptake of self-services.

- Since middlemen have become an integral part of the process, training and converting them into formal government agents can not only create formal employment, but also increase consumer understanding and utilisation of digital services.

- Carrying out education and awareness campaigns jointly between the government MDAs and payment providers.

Benefits to Government: potential cost savings and new revenue

According to the Better Than Cash Alliance Ghana country diagnostic, only 0.2 per cent of payments by citizens to businesses are made electronically (although the diagnostic antedated the introduction of mobile money payments for utilities).

Like Kenya, the most immediate benefits Ghana can realise from digitising P2G payments are:

i. Reduction in revenue leakages and compliance costs: Accepting digital payments can reduce the exposures to pilferage of revenues such as one created in in 2016, when Driver and Vehicle Licensing Authority of Ghana lost about 40 per cent of revenue due to registering fake number plates. Digitising this process would have brought transparency and provided the relevant records that would have exposed any unprecedented losses.

ii. Increases in usage and non-tax revenue: While reducing revenue leakages is important, it would be even more valuable to increase non-tax revenues which was approximately GHS 7.2b (USD 1.6b) in 2016, according to Ghana budget of 2016/2017. If the digitisation process is successful, it is estimated to increase by about 40 per cent or GHS 2.8 billion (USD 630 million) in three years. Within the wider category of non-tax revenues, fees and charges currently stand at GHS 723 million (USD 153 million); a similar 40 per cent increase would be around GHS 290 million (USD 64 million) annually.. Kenya’s national government has seen a 78 per cent increase in non-tax revenues between 2014 and 2017, without widespread increases in fees charged.

iii. Better visibility of financial position: Kenyan agencies now have online, real-time financial data enabling them to collect additional funds, which in turn helps to extend and improve services to citizens and make quicker payments to suppliers and service providers. To incentivise MDAs to adopt digital payments and to realise the full benefits of this transition, agencies should be able to retain a good share of the incremental revenues that come from digitised processes.

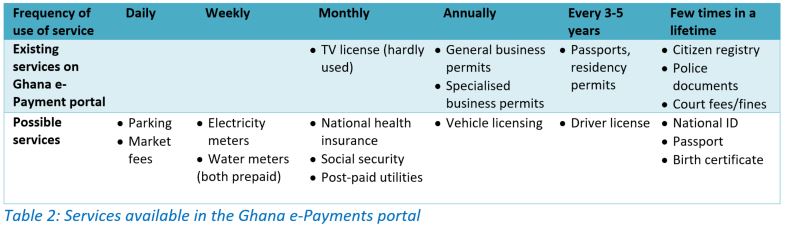

The revenue opportunity for both providers and MDAs would be more attractive if transactions with higher volumes and frequencies were available in the e-Payments portal which could in turn transform user behaviour. High-frequency transactions with large numbers of users of the portal, they would generate sufficient funds to cover their ongoing costs, especially those driven by utilities, social agencies and parking (see Table 2). Utility payments offered via mobile money to Ghana Water and The Electricity Company of Ghana could potentially kick off the drive for the increase in volume and frequency of digital payments.

To realise these benefits, the government must be prepared to invest early in the digitisation process, especially awareness campaigns to acquaint the public with the new service options, working with mobile money providers to accelerate uptake through marketing and customer service initiatives. “There is need to increase wallet limits from the current maximum daily limit of $1,000 per transaction to avoid multiple payments for a single transaction”, adds Eli Hini, General Manager, MTN Financial Services.

Mobile money providers – what’s in it for them?

Mobile money has significantly grown in Ghana since 2016, making it one of the fastest growing markets in the world. National Communications Authority in Ghana reported growth of 98.51% in the value of transactions in 2017 over 2016 while the transaction value was GHS 155.84 billion (USD 33.88 billion) vs. GHS 78.5 billion (USD 17.06 billion) over the same period.

P2G is a valuable new use case for providers to explore in order to build up transactions and wallet usage, following investments in capital costs of integration to the e-Payments platform. A potential increase in transactions supports an important business goal – to increase usage and viability of their mobile money wallets. “Digitising government payments will stimulate increased adoption and usage of mobile money wallets and we will continue to support Government efforts to digitise payments,” says Eli Hini of MTN Ghana.

With most of the preconditions for mobile money payments already in place in Ghana, the government can significantly enhance adoption with relatively minor changes in prioritisation and implementation:

- Bring high-volume high frequency services online soonest.

- Ensure the seamless functioning of the platform – minimise downtime, make the customer experience easy and convenient.

- Collaborate with MNOs in marketing and customer service efforts

- MNOs have a unrelenting role working with government and MDAs on these issues. Citizens, mobile money providers and government all stand to gain from accelerated usage of mobile money for government payments.

Footnotes

[1] Respondents quoted GHS 200-300 payment to middlemen (USD 44-67). We have assumed a government service fee of GHS 70 (USD 15).

[2] Potential values are based on the actual costs incurred in Kenya for digital payments for government services.