New analysis finds that customers don’t pay for improved performance and investment in concentrated markets

Brussels, 7 July 2026: More concentrated European mobile markets see significantly higher investment in key infrastructure, according to a new report from the GSMA exploring the benefits of scale.

Efficient operator scale in European mobile markets, a GSMA Intelligence study, found that Europe has the lowest level of market concentration globally among major economies.

This has led to a fragmented landscape which is constraining investment in next-generation networks, slowing 5G standalone rollout, and ultimately weakening the bloc’s digital competitiveness.

As the EU looks to revise its approach to assessing mergers, the benefits of consolidation in the mobile sector – namely better quality at the same price for customers – are outlined in the report.

An optimal level of concentration

The analysis found that operators in three-player markets have invested around 48% more than operators in four-player markets over the last decade.

More concentrated markets are often thought to lead to higher consumer prices but the report finds evidence of no price rises in consolidated markets. Instead, users in three-player markets often benefit from speeds around 15% faster, more widespread coverage and better reliability.

The report also finds limited impact on market entry, while consolidation shows clear positive effects on investment in networks and therefore on user-experienced network quality and performance.

A pronounced investment gap

This comes against the backdrop of digital underperformance in Europe, where only 3% of connections are currently across 5G standalone networks compared with around 80% in China, 50% in India and 30% in the USA.

Recent analysis found that €475 billion of investment is needed over the next decade to help Europe catch up, of which only €270 billion is expected to be available to operators – leaving an investment gap of more than €200 billion.

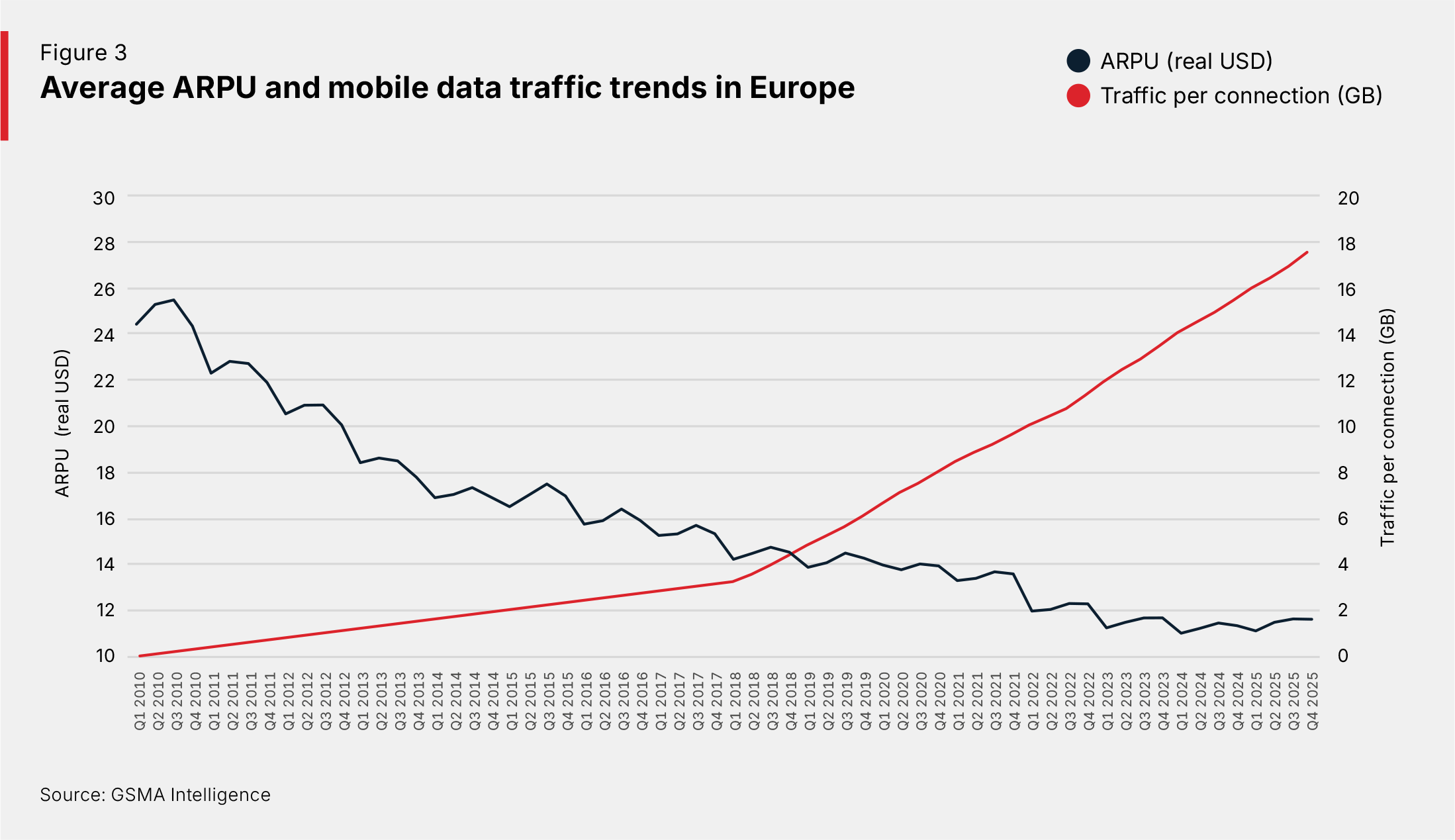

In the data era, with adoption of mobile internet services in Europe already at saturation point, exponential traffic growth has been mirrored by a steep decline in average revenue per user (ARPU).

Lower ARPU constrains the capital available for investment and demonstrates why improved scale is a necessary solution for Europe’s operators. Data traffic across the EU has grown by 550% since 2018, with similar forecasts for the years ahead.

Policy priorities

Having led the world in earlier mobile internet generations, the 5G era has seen Europe struggle to keep pace with leading global markets as a result of these investment limitations.

The risk now is twofold: additional delays in truly completing the 5G journey and the consequent missed opportunities to exploit the innovation it drives, and the likelihood of falling even further behind when the 6G era fully emerges over the next ten years.

Among the recommendations it makes to policymakers for encouraging scale and investment in Europe’s mobile market are:

- To move beyond operator count as a benchmark for competition

- To adopt a forward-looking approach to merger assessments

- To support efficient market structures for 5G and future technologies

Laszlo Toth, Head of Europe at the GSMA, comments: “Mobile is a scale-driven, investment-intensive industry, but a longstanding unattractive environment has left operators struggling for the requisite capital.

“Functional markets rely on healthy competition and when concentration is optimised, we see how consumers can enjoy better quality services at the same price point as operators are able to invest more in upgrading their networks.

“The opportunity to enable efficient operator scale is a critical one for delivering the connectivity Europe needs to compete globally.”