This article is part of the Spectrum Policy Trends 2026 report. Download the report for a handy compilation of the top five spectrum policy trends for 2026.

Direct-to-device (D2D) connectivity between satellites and mobile handsets has been high on the regulatory agenda for several years and business models are evolving rapidly. The regulatory world knows how D2D using mobile satellite (MSS) spectrum works but is worried that a lack of compatible handsets will prove a barrier to adoption.

Meanwhile, the concept of D2D using terrestrial mobile spectrum in bands with an IMT identification, through the terrestrial licence holder, is a new regulatory ground. The World Radiocommunication Conference in 2027 (WRC-27) will provide international regulations, but in the interim period, first-mover countries are making their own rules. D2D using mobile spectrum does not have to worry about specialised handsets (standard devices can be used), but keeping existing mobile free from interference is still being discussed.

Why does it matter?

Connecting to D2D requires access to a mobile phone and, normally, a subscription with an MNO that has a D2D contract with a satellite network operator (SNO). D2D can thus potentially be a supplementary service for the 58% of the world’s population that are connected to mobile by allowing them to stay connected while outside of coverage areas. It can also help connect the 4% of people who do not live within coverage areas (“coverage gap”), providing they can afford device and services costs (this will not be everyone in the 4% coverage gap).

However, D2D will not have a significant impact on reducing the “usage gap” of 38% of the global population that live within the footprint of a mobile network and are not using it due to issues including affordability and digital literacy. Addressing both the lack of coverage and usage will be important to expand connectivity and address digital divides. Satellite’s strength lies in its ability to reach remote areas. It cannot provide the capacity that terrestrial mobile networks can deliver, but with the correct regulation, D2D can supplement terrestrial mobile coverage.

What are the policy considerations?

SNOs may be looking at hybrid offerings through both forms of D2D – using MSS or mobile spectrum – but their regulation still differs. MSS bands have an existing international framework but using mobile spectrum requires new agreements to be made internationally, and domestic regulation to be put in place.

D2D using mobile spectrum is being permitted by regulators through the terrestrial spectrum licence. This means the rights of use by satellite for any given terrestrial band derive from the exclusive rights on MNO licences, through commercial agreements or other authorisation tools as applicable in each country. This approach allows MNOs to decide how best to use their licensed mobile spectrum bands to enable satellite connectivity for subscribers.

The capacity provided by D2D needs to be clearly understood by regulators and their political counterparts. This is not being helped by some of the media coverage on the issue which suggests mobile-like service quality. D2D will provide valuable coverage but it will not provide meaningful data to areas of significant population coverage (which include a lot of rural areas). Free space path loss weakens the satellite signal from space while the large footprint of satellite spotbeams (25km against a maximum of around 2.5km for a low-band mobile cell) limits spectrum reuse. To get any kind of data rate from D2D – say 2 Mbps – the number of people in the spot beam needs to be very small. The GSMA estimates that even with a 12,000-satellite constellation and access to 80 MHz of mobile spectrum, D2D could offer 2 Mbps to only 1.5% of the world’s rural population.

What to expect in the year ahead

In our 2025 spectrum trends piece on D2D, the GSMA wrote: “Consumers care about service quality – not the underlying technology”. This fact has rung true in the D2D world in the last year where the above distinction between the two types of D2D is being merged at a business level by many of the players.

One year ago, SNOs largely had assets for one or other form of D2D – using MSS or mobile spectrum – but that has shifted. The SpaceX purchase of Echostar’s S-band spectrum hit the headlines, but the associated purchase of its S-band satellite filings was perhaps even more critical and together they will give the company a choice of spectrum to offer service from. AST Space has also made moves in MSS spectrum while two smaller players – Lynk and OmniSpace – have merged their respective mobile spectrum and MSS approaches under their significant shareholder SES Global.

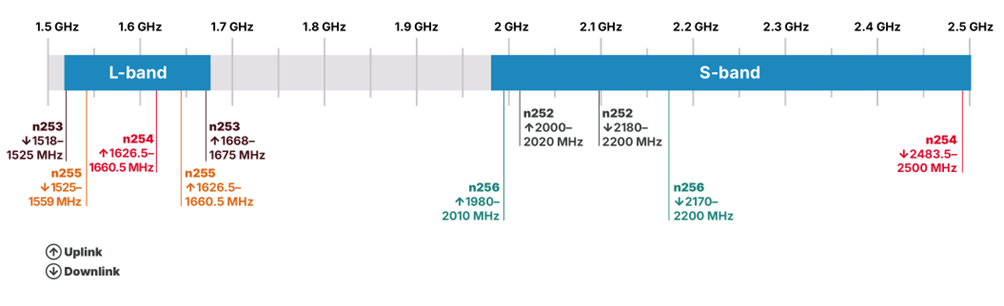

It is likely that the 2 x 30 MHz of S-band MSS spectrum around 2.1 GHz will continue to be an area of focus. Both SpaceX and AST have acquired filing rights to this spectrum at the ITU, but its local assignment will also be important. In Europe, the current spectrum licences (ViaSat, through its Inmarsat purchase, and Echostar) expire in 2027. While these were originally sold as complementary ground component (CGC) spectrum, Inmarsat has partnered with Deutsche Telekom to provide the European Aviation Network, while Echostar has provided some enterprise connectivity. The reworking or renewal of these licences are likely to include D2D – not so much complementary ground component as supplementary space component. While satellite filings at the ITU give rights to provide connectivity in space, they do not give rights to land and regulators around the world will have to decide on the best way of giving access to this spectrum. Satellite operators have traditionally paid administrative fees for in-country access, but will we see these S-band landing rights considered a scarce resource coupled with competitive bidding? This approach to auctioning landing rights is certainly being considered by some regulators.

MSS spectrum

What is certain is that more MNOs will be signing deals with satellite operators to extend their coverage this year. Some will do this to fulfil coverage requirements in very low population areas. Others will associate the services with premium subscriptions, offering their subscribers SMS/SOS and low-bandwidth data services in areas they do not currently cover, such as national parks or territorial waters.

| Policy in practice: Australia’s regulatory approach to D2D services Australia has adopted a cautious, licence-centric approach to the introduction of D2D. The Australian Communications and Media Authority (ACMA) has stipulated that satellite-based D2D operations must be conducted under the terms and conditions of an existing terrestrial mobile licence, with the mobile network operator retaining full regulatory responsibility. ACMA’s position emphasises that terrestrial spectrum licences confer rights and obligations that cannot be bypassed by satellite operators. Use of mobile spectrum for D2D therefore requires agreement with the terrestrial licence holder, with services operating in a manner consistent with licence conditions, including technical parameters, interference management and geographic constraints. This reflects a need to protect incumbent services and ensure that D2D remains supplementary to terrestrial mobile networks. ACMA has signalled that further consideration of D2D will be evidence-based and incremental, prioritising service continuity and regulatory certainty over rapid market entry. Their approach closely mirrors the US Supplemental Coverage from Space model, particularly in its reliance on mobile operator consent, use of existing IMT licences, and treatment of D2D as a supplementary service in conjunction with a terrestrial network. |