Friday 12 June, 2026

Fixed broadband speeds in the Philippines are gradually improving. This is attributed to the combined efforts of ISPs and government agencies to expand coverage and promote the transition from legacy fixed-line technologies to faster fiber connections. However, the distribution of fixed network infrastructure across the country is uneven, and there is still room for further improvement and adoption.

Key Takeaways

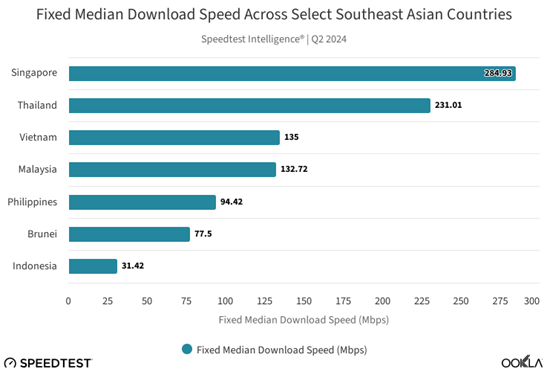

- Fixed performance in the Philippines is improving but still lags behind some neighbors. While the Philippines’ fixed broadband network performance continues to improve quarter over quarter, Ookla® Speedtest Intelligence® shows the Philippines’ speed of 94.42 Mbps in Q2 2024 was behind some of its Southeast Asian peers’ median download speeds, such as Singapore (284.93 Mbps), Thailand (231.01 Mbps), Vietnam (135.00 Mbps), and Malaysia (132.72 Mbps).

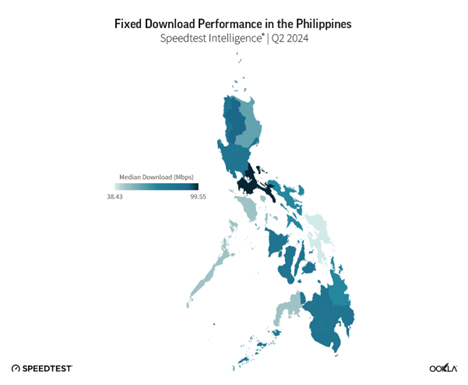

- The five fastest regions in the Philippines were in Luzon Island, highlighting the unequal distribution of fixed network infrastructure. In Q2 2024, Luzon Island had the regions with the top five fastest fixed performance in the Philippines, all reporting download and upload speeds surpassing 90 Mbps. Calabarzon had the fastest fixed median download speed of 99.55 Mbps, while the Eastern Visayas region had the lowest median fixed download speed of 38.43 Mbps.

- An increase of Starlink’s low-Earth orbit satellite-based connection is an interesting development and may make this satellite service a viable home broadband alternative. Speedtest samples for Starlink in the Philippines have significantly increased over the past year. However, Starlink’s performance lags behind that of fixed broadband, with median download speeds half of fixed download speeds for all operators, at 48.14 Mbps compared to 94.42 Mbps. Upload speeds were also significantly lower, at 12.63 Mbps compared to 94.13 Mbps reported by all fixed broadband operators.

Philippines’ fixed performance continues to trail behind neighboring counterparts

Broadband subscriptions in Southeast Asia substantially surged during the pandemic, reflecting the increased demand for connectivity. Although 92% of the total broadband subscriptions are mobile, there are efforts in the region to bolster fixed broadband access. Government initiatives in the region have led to improvements in fixed broadband performance. However, there is still a disparity in broadband performance among regional counterparts.

Looking at performance in Q2 2024 in select Southeast Asian markets, Singapore and Thailand maintained a significant performance lead compared to other countries in the region, achieving median fixed broadband download speeds in excess of 200 Mbps during Q2 2024. Malaysia and Vietnam demonstrated similar performance, both achieving median fixed download speeds of 132.72 Mbps and 135.00 Mbps, respectively, surpassing the Philippines’ speed of 94.42 Mbps in Q2 2024. Of the remaining selected markets, Brunei had a speed of 77.50 Mbps, trailing behind the Philippines, while Indonesia, which shares geographical similarities with the Philippines as both are archipelagos composed of thousands of islands, reported the slowest fixed-line market, recording a median download speed of 31.42 Mbps during the same period.

Fixed Median Download Speed Across Select Southeast Asian Countries

Mobile internet is the primary means of access in the Philippines, with only 33% of households having fixed broadband, which is significantly lower than the ASEAN average of 41%. Additionally, the annual charge for fixed broadband accounts for 11% of the per capita gross national income (GNI), which is twice as much as the ASEAN average, making it unaffordable for some of the lower-income population.

Accelerated fiber deployments result in a 50% improvement in broadband speeds

The Philippines was the fastest growing economy across Southeast Asia in 2023. With the improving GDP, there is more disposable income for people to afford connectivity solutions and increased demand for better broadband connectivity in the country. As a result, the fixed broadband market in the Philippines has undergone significant transformations in recent years, marked by a notable shift towards fiber networks and the implementation of 5G fixed wireless access. Both governmental initiatives and efforts by leading ISPs have resulted in substantial investments aimed at expanding and modernizing infrastructure throughout the archipelago.

According to GlobalData in 2022, DSL lines accounted for 37% of total fixed broadband subscriptions in the Philippines. This is expected to gradually decrease and be replaced by fiber, with projections indicating that fiber will constitute over 36% of all fixed broadband lines by 2027.

One key government project aimed at enhancing internet infrastructure is the National Broadband Plan (NBP). Through the Department of Information and Communications Technology (DICT), the Philippine government has rolled out the NBP, which seeks to bridge the digital divide by establishing a nationwide fiber broadband network and wireless technology to provide faster and more affordable internet access to all Filipinos.

As part of NBF, the government recently launched the first phase of its National Fiber Backbone (NFP) project. Targeted to be completed by 2026, the NFB project aims to enhance connectivity and government operational efficiency while extending internet access in Regions I, III, and NCR.

Besides government-led initiatives, ISPs such as Converge ICT, Globe Telecom, and PLDT are investing in and expanding their networks and upgrading their technologies. These efforts aim to offer faster internet speeds to their customers and enhance internet connectivity in both urban and rural areas.

PLDT started deploying fiber in 2015 and as of the end of 2023 it reached 17.3 million households with fiber.. Similarly, Converge ICT, the incumbent fixed broadband player, added 900,000 new homes to its fiber footprint in 2023 and ended the year with nearly 16 million homes passed.

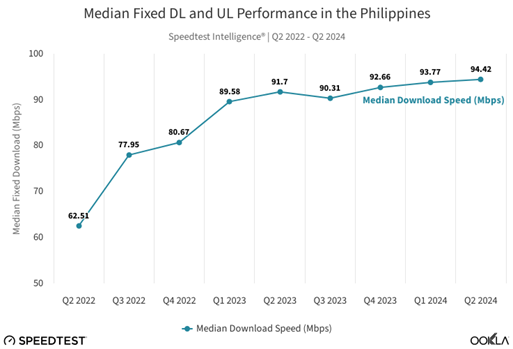

Network performance in the Philippines has improved over the past two years. Ookla Speedtest Intelligence® data indicates a steady increase in median fixed download and upload speeds across the Philippines for all fixed providers combined between Q2 2022 and Q2 2024. During this period, the median fixed download speed rose by 51% from 62.51 Mbps to 94.42 Mbps. Since most ISPs offer symmetric speeds, the median fixed upload speed also showed an upward trend, increasing from 58.65 Mbps in Q2 2022 to 94.13 Mbps in Q2 2024.

Median Fixed DL and UL Performance in the Philippines

Regions in Luzon Island dominates fixed broadband performance, underscoring disparities across the country

Despite various efforts to enhance fixed performance throughout the Philippines, there are persistent regional disparities in median download and upload speeds due to the uneven distribution of fixed network infrastructure. Based on Speedtest Intelligence® data from Q2 2024, Luzon Island stands out for its fixed internet performance, with the five fastest regions situated on the island, recording download and upload speeds surpassing 90 Mbps. Given Luzon’s economic significance and high population density, it is where the majority of the country’s investment in high-speed broadband infrastructure is concentrated, especially in the capital, Metro Manila, as well as nearby provinces, and central Luzon.

Calabarzon, the region with the largest population of 16 million, had the fastest fixed median download speed of 99.55 Mbps in Q2 2024. The region has the second-highest percentage of households with access to fixed broadband network, at 23.4%, after Metro Manila (NCR), which had the highest share, at 26.4%. At the other end of the scale, the Eastern Visayas region (Region VIII), occupying the eastern section of Visayas Island, scored the lowest median fixed download speed at 38.43 Mbps.

Fixed Wireless Access and satellite broadband as an alternative to bridge the digital gap

The Philippines’ geographical layout, consisting of over 7,000 islands, is challenging for fiber deployment. Due to the archipelago’s structure, ISPs may be reluctant to invest in fiber deployment as accessing remote parts can be difficult. In many low-density and low ARPU areas, fixed networks are neither cost-effective nor logistically viable. To this end, Fixed Wireless Access (FWA) and Satellite Communication (SatCom) are becoming attractive options for tapping into these underserved and remote populations.

FWA provides the fastest and most flexible broadband option in areas where fixed broadband is unavailable, especially since the Philippines is a predominantly mobile market. 4G FWA has been available in the Philippines for some time and MNOs use FWA to increase broadband adoption in areas with low fixed broadband coverage. As 5G coverage expands nationwide, it brings significant performance improvements, positioning FWA as a strong competitor to the existing fixed alternatives, such as fiber-to-the-home (FTTH).

The Philippines was the first country in Southeast Asia to experience commercial 5G FWA connectivity. In 2019, Globe launched its first commercially available 5G FWA service called Globe At Home AirFiber 5G. This service offers speeds of up to 100 Mbps and generous data allocations of up to 2 terabytes (TB), starting at around P1,899 (USD$36) per month. Smart Communications launched its prepaid Home Wi-Fi 5G called Smart Bro Home Wi-Fi 5G at the end of 2021.

At its peak, an estimated 4.3 million users in the Philippines access broadband through FWA. Interestingly, the FWA growth rate has declined in the last two years, as reported by ABI Research. In early 2023, Globe Telecom reported a subscriber base of 1.2 million for its fixed wireless services, a decrease from 2.4 million the previous year. Likewise, PLDT reported a 45% decline in FWA subscriptions at the end of 2023 compared to the beginning of the year. This decrease in FWA numbers was partly due to the increased availability of fiber broadband access nationwide. Both providers noted a rise in fixed fiber broadband subscriptions, which is understandable given that fiber provides more reliable connectivity than FWA.

There has also been a significant increase in satellite-based connectivity to provide internet access in areas not covered by traditional terrestrial networks. Based on Speedtest samples, Starlink’s LEO service is providing the majority of satellite internet connectivity in the country. Starlink service in the Philippines launched in early 2023. Based on the comparison between Q2 2024 and Q2 2023, there has been a substantial increase in Starlink Speedtest samples in the Philippines, growing by 228.5% over the past year, and this number is expected to increase further. According ABI Research, the Philippines is projected to become the largest Southeast Asian market for satellite broadband, with 909,000 subscriptions by 2028.

Speedtest Intelligence data indicates that Starlink underperformed compared to all fixed broadband operators combined. Starlink’s Q2 2024 median download speeds were almost half of the median fixed download for all operators, at 48.14 Mbps compared to 94.42 Mbps. Starlink’s median fixed upload speeds, at 12.63 Mbps, significantly lagged behind the 94.13 Mbps provided by fixed broadband operators, which provides symmetrical upload and download speeds.

Multi-server latency tends to be higher for satellite providers, with the significant distances between satellites and receivers resulting in long delays. For Q2 2024, Starlink’s multi-server latency was double that of all fixed operators combined, at 50 ms compared to 25 ms for the latter.

Starlink Performance Against All ISPs Combined

Besides Starlink’s performance challenges, the equipment and subscription costs are higher than terrestrial broadband options, making it inaccessible for some users. However, it provides a viable alternative, especially in locations without access to fixed broadband or with slower DSL connections.

It’s clear that the regulatory bodies and ISPs in the Philippines are committed to advancing broadband connectivity by implementing various strategies aimed at deploying fiber, promoting its adoption, and offering wireless broadband as an alternative to increase competition. These efforts have led to notable improvements in fiber accessibility and fixed broadband speed over the past two years. However, a significant gap in fixed broadband performance remains compared to some neighboring countries in the region.

Establishing a closer private-public partnership is imperative to meet the increasing demand for better fixed broadband and narrow the gap with neighboring countries. This, in turn, will drive the development of robust fiber networks and promote greater availability of higher-speed broadband services while encouraging existing customers to upgrade to faster speeds. We’ll continue to monitor the progress of the Philippines’s fixed broadband market and provide updates on the state of fixed broadband connectivity across other Southeast Asian markets. If you are interested in Ookla’s solutions and services for network intelligence and management, get in touch.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.