Friday 12 June, 2026

Poland’s operators are rapidly deploying mid-band 5G in an attempt to capture the growing premium market segment

Late to the game in staging a mid-band auction, Poland has lagged behind its European peers in 5G deployment in recent years. This delay has weighed on the country’s global competitiveness in mobile network performance and slowed its progress toward meeting the European Commission’s flagship 5G deployment targets, which require universal 5G coverage across every EU member state by the end of the decade.

This article examines the state of Poland’s mobile market and its broader regional 5G competitiveness in the context of ongoing mid-band deployments. A follow-up report will assess the longer-term impact of the commercialization of the recently awarded low-band spectrum and ongoing network sunsets on network coverage and availability.

Key Takeaways:

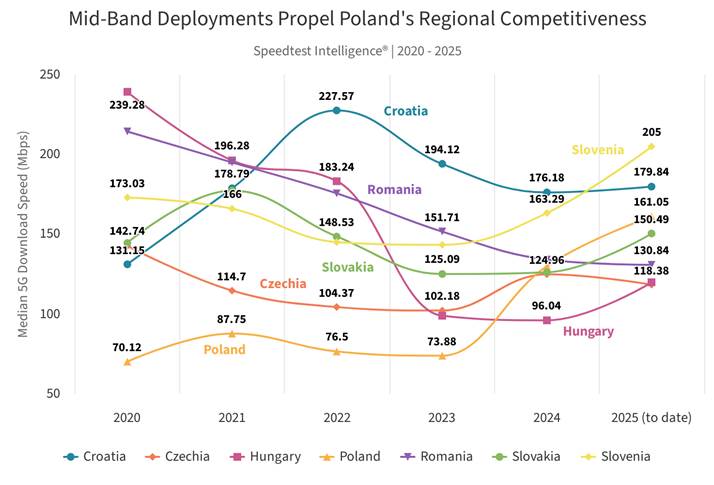

- Intensive capital spending on mid-band deployment drives substantial uplift in 5G performance across Polish operators from Q1 2024, pushing the country ahead of regional peers over the last year. Median 5G download speeds in Poland jumped by over 50% to 160.30 Mbps between Q1 2024 and Q1 2025, based on Speedtest Intelligence® data, propelling the country ahead of Czechia, Romania, and Slovakia for the first time in 5G performance. Despite this progress, Poland continues to trail its regional peers in 5G network Consistency, a measure of how reliably a mobile connection remains “fast enough” for normal use.

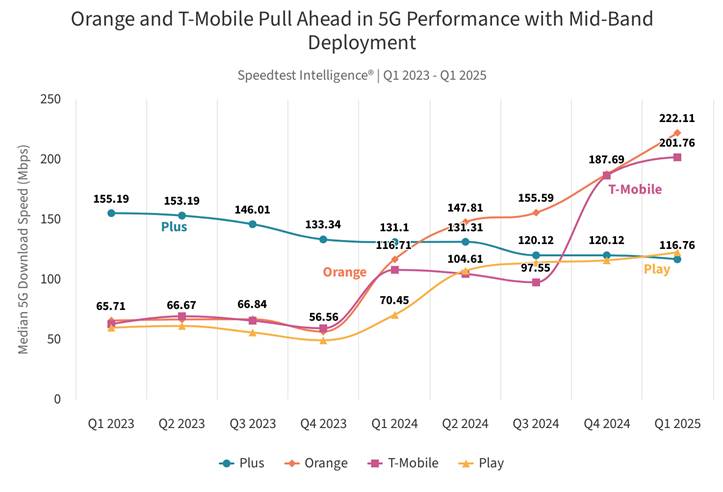

- T-Mobile and Orange surpass Play and Plus in speed and select Quality of Experience (QoE) measures. Differences in how quickly and extensively Polish operators have deployed their mid-band spectrum assets have led to a diverging market profile since Q1 2024, with T-Mobile and Orange significantly extending their speed lead over their rivals. Between Q1 2024 and Q1 2025, median 5G download speeds rose by as much as 72% on Play (to 122.64 Mbps), 86% on T-Mobile (to 201.76 Mbps), and 90% on Orange (to 222.10 Mbps)—while declining by over 10% on Plus (to 116.76 Mbps).

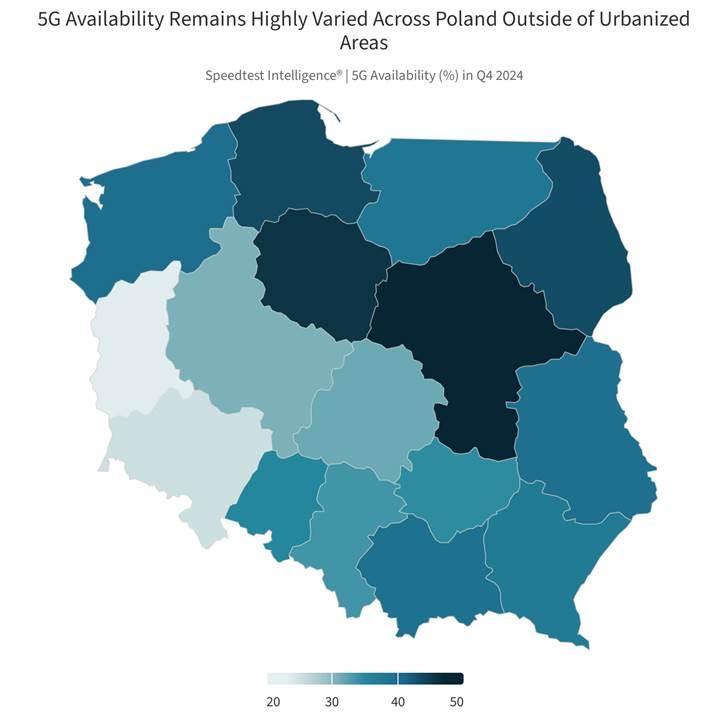

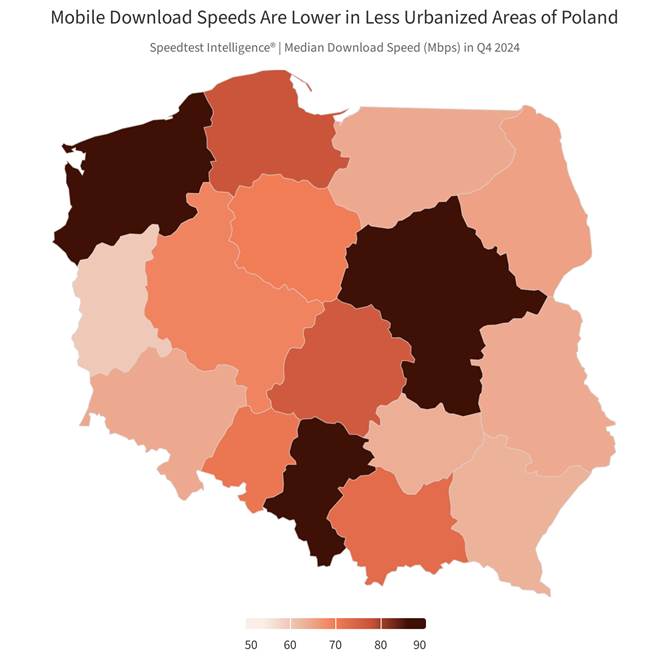

- Network investments have broadened 5G coverage in Poland, but significant regional disparities remain. Nationally, 5G availability rose from 28.5% in Q1 2024 to 43.1% in Q1 2025, driven by continued Dynamic Spectrum Sharing (DSS) rollouts and the activation of mid-band spectrum—placing the country ahead of regional peers Bulgaria, Romania, and Hungary in 5G availability. Nonetheless, by Q4 2024, a pronounced coverage gap persisted between the country’s best- and worst-served provinces, with 5G availability in the populous Masovian Voivodeship (47.2%) double that of the Lubusz Voivodeship (23.6%).

Over the last year, Polish operators have been locked in an intense four-way race to catch up with their regional peers in 5G deployment, driven by stringent coverage obligations imposed by the Polish telecoms regulator (UKE), a wave of funding support from Brussels, and a growing push to compete for a larger share of the country’s widening premium market segment, where network performance has emerged as a key competitive differentiator.

Poland’s mobile market is today awash with deployment activity, as operators ramp up capital spending to the highest levels in years to equip thousands of mobile sites with mid-band spectrum, accelerate the sunset of 3G networks, and lay the groundwork for launching 5G standalone (SA) in the coming years. This flurry of activity follows the completion of the 700/800 MHz auction at the end of March this year, where all Polish operators secured low-band 5G spectrum for the first time—paving the way for improved rural and deep in-building 5G coverage and rounding out the country’s 5G spectrum release plans.

While 5G capital spending has slowed across much of Europe, Poland sees different dynamics due to late spectrum auctions

Poland was notably late in releasing dedicated 5G spectrum in the ‘pioneer bands’ identified by the European Commission as critical to the timely commercialization and rollout of 5G across EU member states. The country’s mid-band (3.6 GHz) auction, initially planned for mid-2020, was repeatedly delayed—by more than three years—due to the pandemic and a protracted security legislation process.

These delays in spectrum availability have contributed to Poland’s divergence from much of the rest of Europe in both the economic and technical dimensions of the 5G rollout. Until recently, Polish mobile operators exhibited lower capital intensity (they invested less of their revenue) compared to peers in other European countries. Most of their spending went into upgrading 4G sites and preparing for the 3G shutdown, instead of building a new 5G mid-band capacity layer or expanding 5G coverage using low-band (700 MHz) spectrum.

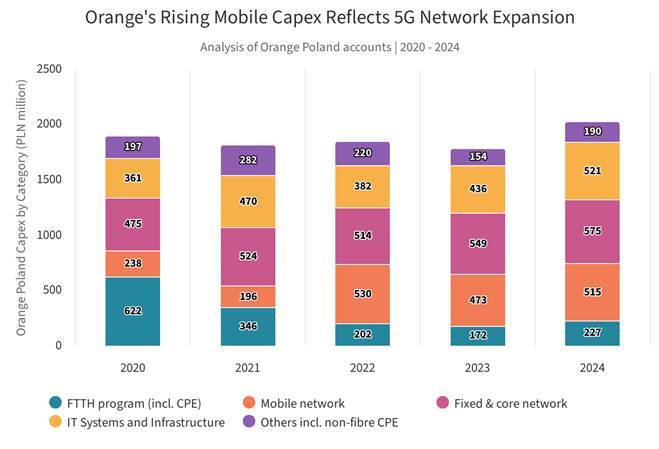

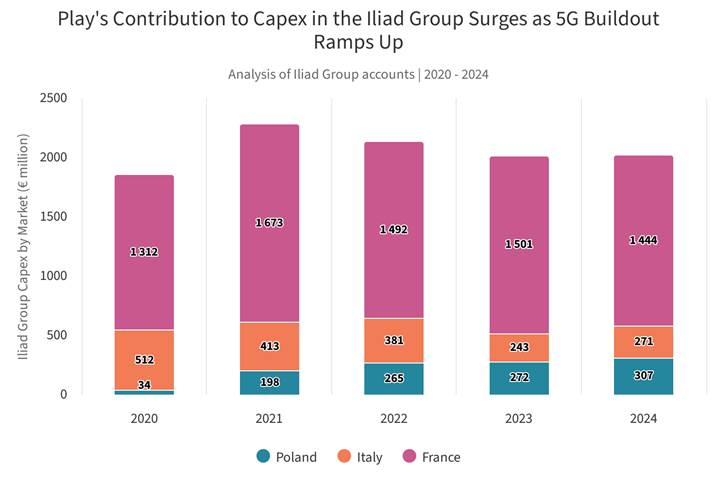

Analysis of financial data published by Orange, Poland’s largest mobile operator by subscriber count, confirms that the era of lower capital intensity (relative to elsewhere in Europe) is over. The recent spectrum auctions have triggered a new cycle of investment, with Orange doubling its mobile network spending in the past three years. Play has also rapidly increased its investment, as its French parent Iliad reported injecting record amounts into Play’s mobile infrastructure last year.

On the technical side, meanwhile, Poland’s spectrum delay meant that three of the country’s four operators were forced to rely heavily on Dynamic Spectrum Sharing (DSS)—a technology that allows 4G and 5G to operate on the same band and adjust ‘dynamically’ to demand—in an effort to deliver early 5G coverage in the 2100 MHz band while awaiting spectrum auctions. This strategy resulted in Poland’s initial 5G performance more closely resembling those typical of 4G networks, as DSS deployments are typically based on a 10 MHz carrier where part of the capacity is still reserved for 4G signals, making 5G speeds with DSS around 15–25 % lower than if the band were dedicated solely to 5G.

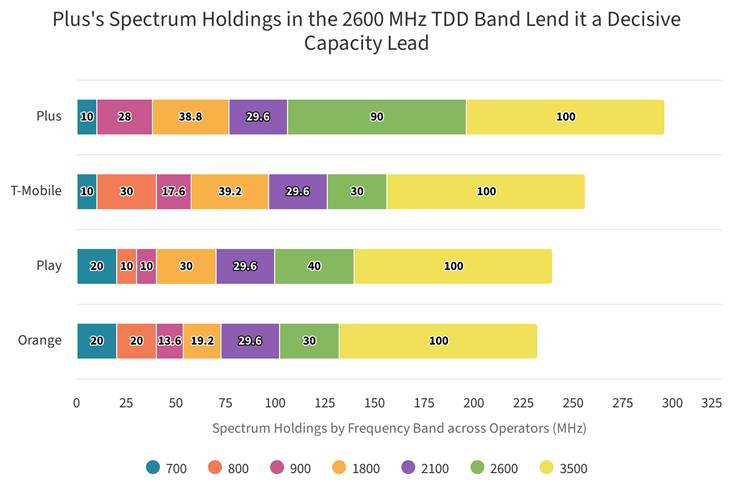

The limitations of using DSS to deliver a “5G experience” were exemplified by the speed advantage maintained by Plus earlier in the 5G rollout. Importantly, Plus was the only Polish operator that did not rely on DSS and instead dedicated a full 40 MHz carrier in the 2600 MHz (TDD) band to 5G before mid-band spectrum became available at the start of last year. Prior to the 3.5 GHz band coming online, when the other operators were still wholly dependent on DSS for 5G coverage, Plus’s median 5G download speed of 133.34 Mbps was as much as 77 % higher than T-Mobile’s, 81 % higher than Orange’s, and 92 % higher than Play’s.

Intense Mid-Band Deployment lifts Poland’s Regional 5G Competitiveness and Reshapes Operator Dynamics

Polish operators move from mid-band spectrum acquisition to mass commercial deployment in record time

The pent-up demand for mid-band spectrum in Poland was evident when mobile operators like Orange, T-Mobile, and Play launched commercial services just three months after acquiring mid-band spectrum, moving quickly from the auction in October 2023 to commercial launches by January 2024. T-Mobile reported that its mid-band 5G network already covered more than 25% of the Polish population by April 2024, with more than 2,100 sites active, while Orange announced it had reached 40% coverage by mid-June.

This rollout pace is exceptional by European standards and indicative of the increased pace of deployment possible later in the 5G technology cycle. It took Spain’s Telefónica (Movistar) about six months to reach its first 1,000 mid-band sites by comparison, and Germany’s operators needed around nine months to achieve the same milestone.

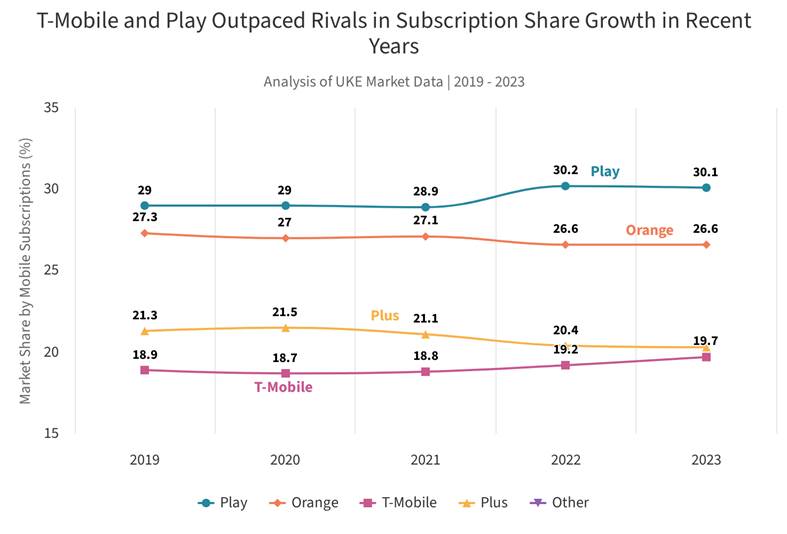

Each operator secured a contiguous 100 MHz block of spectrum in the 3.5 GHz band, which is widely regarded as optimal due to the large channel bandwidth this configuration affords. However, Plus has been notably slower to commercialise this allocation at scale. Plus’s earlier strategy of deploying 5G in the dedicated 2600 MHz band (rather than relying on DSS), alongside later using the 2100 MHz band as well, gave it more flexibility to delay a broad mid-band rollout as it previously enjoyed a significant 5G speed advantage over competitors while they were still heavily dependent on DSS deployments.

Mid-band deployment shifts 5G performance rankings among Polish operators

Mass deployment of a new capacity layer by the other three operators has since decisively altered performance dynamics in the Polish market and eroded Plus’s lead. In the space of one year between Q1 2024 and Q1 2025, Plus has moved from market leader in median 5G download speed to laggard, becoming the only Polish operator to see a year-on-year decline in 5G speed, down 10%, indicating the increasing limitations of its 2600 MHz strategy.

By contrast, mid-band deployment has boosted performance across the rest of the market, with median 5G speeds rising by as much as 72% on Play, 86% on T-Mobile, and 90% on Orange between Q1 2024 and Q1 2025. While Orange led the Polish market in Q1 with a median 5G download speed of 222.11 Mbps, the operator’s lead has narrowed significantly as T-Mobile’s mid-band buildout has progressed, with T-Mobile now recording median 5G download speeds of 201.76 Mbps, well ahead of third- and fourth-placed Play (122.64 Mbps) and Plus (116.76 Mbps), respectively.

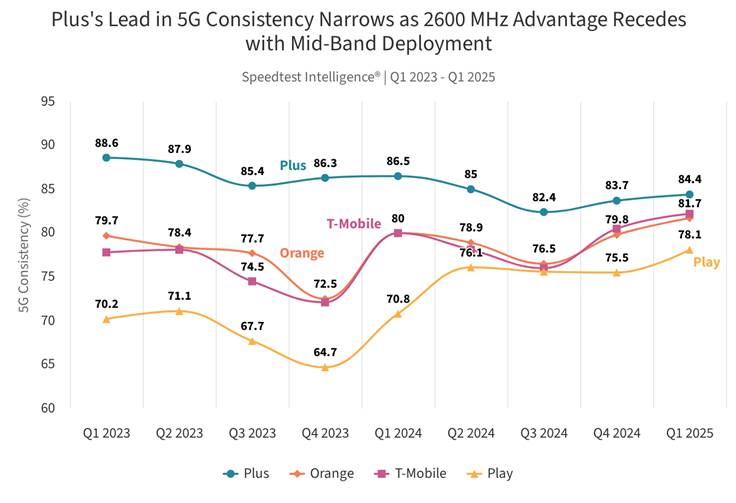

Despite losing its lead in median 5G download speed, Plus continues to lead at the 10th percentile (29.44 Mbps in Q1 2025), meaning subscribers in its lowest-performing areas still enjoy comparatively better speeds than those on rival networks. This advantage is likely linked to Plus’s lower dependence on DSS. However, T-Mobile (24.48 Mbps) and Orange (21.88 Mbps) are quickly closing the gap, with their 10th percentile 5G speeds now converging toward Plus. Plus’s 5G network consistency, measured as the proportion of Speedtest samples meeting a minimum download and upload threshold of 25/3 Mbps, has also declined over the past year, although it remains the market leader.

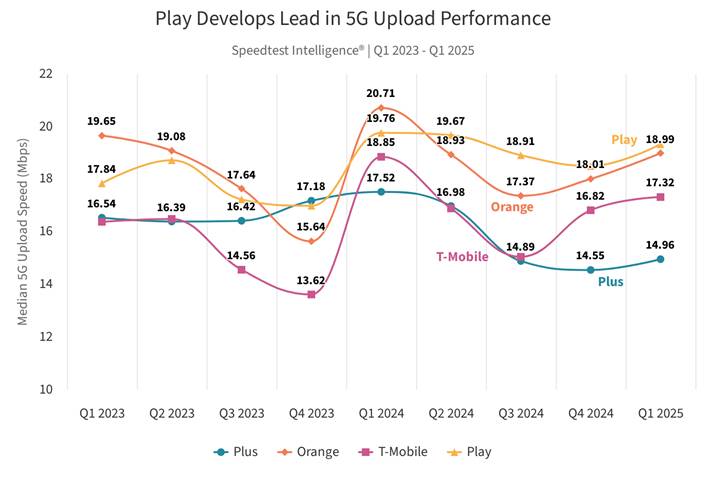

On upload performance, meanwhile, Play’s 5G network led the market in Q1 2025, recording median speeds of 19.33 Mbps, followed by Orange (18.99 Mbps), T-Mobile (17.32 Mbps), and Plus (14.96 Mbps). Unlike the substantial gains seen in download speeds, there is limited evidence so far that the mid-band rollout has materially improved upload performance, with median upload speeds about 6% lower in Q1 2025 compared to the same quarter last year. This discrepancy arises primarily because all four operators continue to deploy 5G in non-standalone (NSA) mode, requiring devices to transmit uplink traffic via existing 4G anchor bands. Consequently, the newly available 3.5 GHz spectrum enhances downlink capacity but leaves the congested 4G uplink path unchanged.

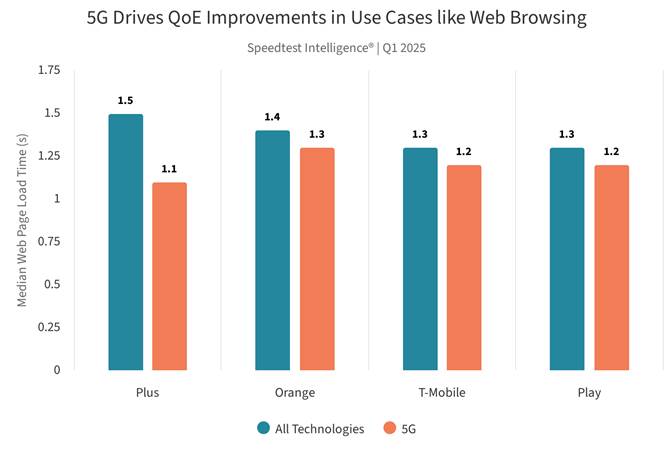

The operators’ investments in deploying a new 5G capacity layer have coincided with a broader RAN refresh effort, translating into improved quality of experience for users in key use cases such as video streaming and web browsing. Median web page load times on T-Mobile’s network, for instance, improved by around 4% between Q3 2024 and Q1 2025. Orange led in video metrics such as start time, resolution, and uninterrupted playback in the last quarter.

Capital investment expands 5G coverage, but Poland’s rural-urban digital divide persists

While investments in DSS and the mid-band rollout have enabled Polish operators to make significant strides in 5G availability, which increased nationally from 28.5% in Q1 2024 to 43.1% in Q1 2025, regional coverage disparities continue to be a feature of the mobile network experience in Poland. Operators have prioritized 5G deployments in the richest and densest parts of Poland where fiber is heavily deployed, including the Masovian (Warsaw) and Pomeranian (Tri-City) provinces. In these provinces, 5G availability reached more than 40% by the end of last year and contributed to driving materially higher median download speeds than the national average.

By contrast, border provinces along the south and west of the country continue to experience much lower levels of 5G availability. Lubusz had the lowest availability (23.6% at the end of last year), where there is lower population density and lower subscriber spending, which reduces operators’ commercial incentives for widespread 5G investment. This trend has driven the development of a notable speed gap between provinces, with mobile subscribers in Lubusz also experiencing the lowest median download speeds (59.97 Mbps) in Poland, almost 33% below the leading Masovian province.

Mid-band deployment improves Poland’s mobile competitiveness, but 5G consistency continues to trail regional peers

From a regional competitiveness lens, intensive mid-band deployments have been successful in breaking Poland’s cycle of mobile network underperformance, with median 5G download speeds rising by over 50% on average to 160.30 Mbps between Q1 2024 and Q1 2025. This has propelled the country ahead of Czechia, Romania, and Slovakia for the first time in terms of 5G download speed performance.

Despite Poland’s progress on its mid-band 5G rollout, the lingering effects of reliance on DSS and limited 5G spectrum diversity—up until the recent 700/800 MHz auction—mean that Poland continues to trail its regional peers in terms of 5G network consistency. In Q1 2025, 82% of Speedtest samples in Poland met the minimum 5G performance threshold for a consistent mobile experience, compared to 86% in Hungary, 89% in Romania, and 93% in Bulgaria.

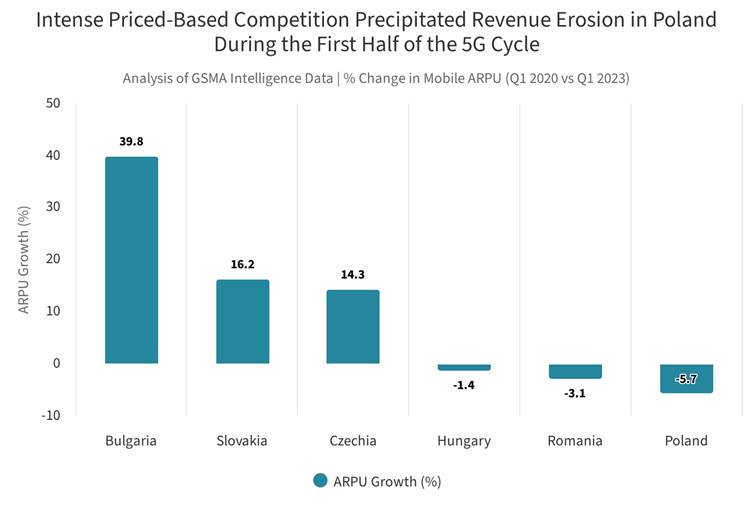

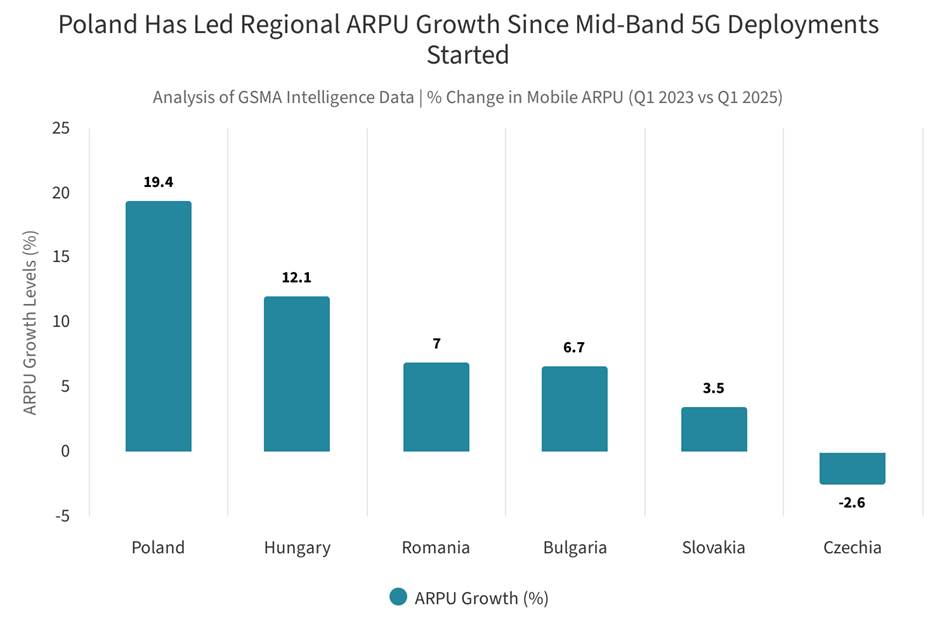

Newfound spectrum diversity lends Polish operators potent tool to stimulate ARPU growth

Poland’s previous reliance on DSS, driven by limited 5G spectrum diversity, likely contributed to its slower average revenue per user (ARPU) growth compared to neighboring countries in recent years. Polish operators initially introduced tariffs with “5G at no extra cost” bolted onto existing 4G bundles, keeping prices flat to defend market share (and thereby maintaining depressed ARPU levels relative to regional peers). Combined with the external shock induced by markedly higher energy prices, stagnant ARPU levels created challenging operating conditions in the Polish market and weighed on operator profitability.

In neighboring markets, by contrast, operators were able to leverage mid-band spectrum deployments as both technical and marketing levers, shifting their strategies from price competition toward service-based differentiation. This enabled them to more effectively upsell premium speed tiers or monetize specific use cases, such as fixed wireless access (FWA), which dedicated mid-band 5G deployments uniquely support.

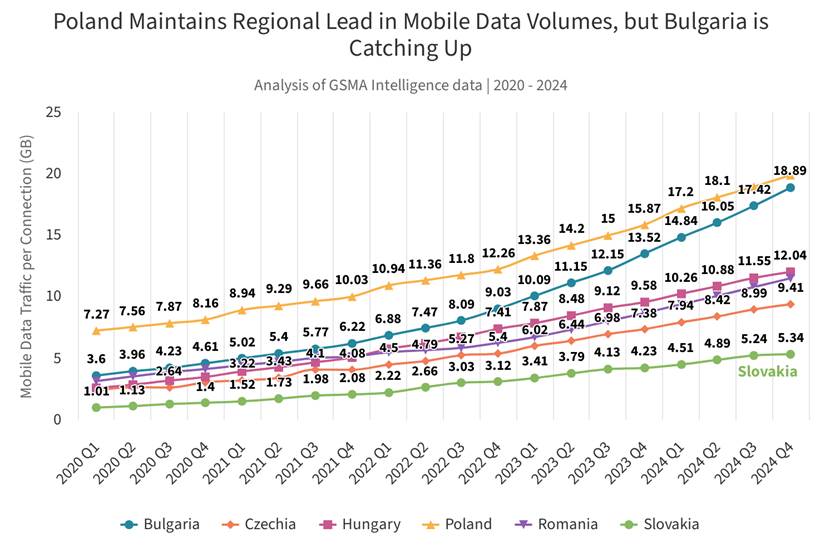

Similarly, the delayed timing of Poland’s mid-band 5G auction likely dampened supply-side factors key for driving growth in mobile data traffic. Between Q1 2020 and Q4 2024, traffic volumes in neighboring Bulgaria converged with that in Poland for the first time, increasing by 4.8x vs. Poland’s 2.6x. Meanwhile, Bulgarian operators capitalized early on mid-band spectrum availability to aggressively promote competitive FWA solutions (a major driver of mobile traffic in developed markets) and to introduce cheap unlimited data tariffs with fewer usage restrictions.

Polish operators have since sought to replicate Bulgaria’s success by debuting distinct marketing for their mid-band 5G deployments to differentiate the newer mid-band 5G rollouts from earlier DSS-based 5G networks in terms of performance and user experience. T-Mobile has leaned on ‘5G More’ branding, while Plus has used ‘5G Ultra’ to indicate the additional performance gains unlocked by their new 5G networks in locations where dedicated mid-band spectrum is deployed. This strategy has formed part of a broader shift in the market, with all operators moving away from a hyper-focus on price competition and toward ‘more for more’ pricing strategies, supporting improved profitability and renewed ARPU growth in the market with inflation-linked tariffs.

Low-band activation and network sunset progress set to reinforce mid-band 5G gains

With Poland’s telecom regulator, UKE, having set among Europe’s most ambitious coverage obligations for recent mid- and low-band spectrum auctions, operators are unlikely to delay commercial deployments in the newly acquired 700 and 800 MHz bands. These deployments are expected to start next month and will be crucial for establishing a national 5G coverage layer that, for the first time, extends deep indoors and into rural areas. This expanded coverage will also support wider rollout of voice over LTE (VoLTE) services, accelerating the 3G sunset and freeing up additional spectrum in the 900 MHz band.

We will revisit shortly to assess how Polish operators are progressing with deploying their new low-band spectrum and how effectively it is complementing the ongoing 3G sunset.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.