Launching today at MWC25 Las Vegas, the latest enterprise research from GSMA Intelligence reveals that operators must rethink their delivery models, bridge critical skills gaps, and embrace co-opetition if they want to seize fast-growing opportunities beyond traditional telecom services.

By Tim Hatt, Head of Research and Consulting at GSMA Intelligence & Richard Cockle, Head of GSMA Foundry and Connected Communities

According to the latest findings from the latest GSMA Intelligence report ‘The telco culture pivot: adapting sales strategies to win in the enterprise’ the addressable market for non-telco IT services, such as cyber security, cloud integration and AI, is projected to hit $500 billion in 2025, climbing to nearly $1 trillion by 2030. Yet many operators risk missing out on this windfall unless they commit to meaningful transformation – but the challenge isn’t just technical, it’s operational, cultural and deeply tied to business outcomes. And telcos need to speak that language to win big.

Manufacturing, financial services, automotive and aviation are the largest aggregate buyers, representing 40% of demand, and those sectors are investing heavily in cloud orchestration, cybersecurity, AI platforms and edge computing. Yet despite operators being their primary connectivity providers, just 10-15% of those enterprises currently buy non-connectivity services from them.

This delta represents a crossroads which forks between enterprise evolution and stagnation, as the potential revenues that are on offer slip further away to fierce competition from hyperscalers, IT service companies and software startups.

The latest research builds directly on the earlier analysis, launched at last year’s MWC Las Vegas, which outlined the opportunity and the need for operators to move beyond traditional connectivity and embrace strategic transformation.

Why the old playbook is running out of road

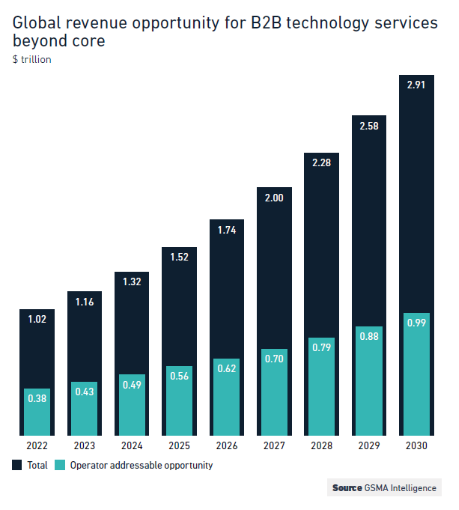

By 2030, enterprises will spend nearly $3 trillion on B2B technology services outside core telecoms. Mobile operators can potentially claim close to $1 trillion of that number, but capturing it requires significant cultural and operational change, not just new product launches.

Many operators have created enterprise business units – 62% of them, according to our research – but most remain product-led. Selling bandwidth in a B2B wrapper doesn’t work when CIOs expect embedded delivery, co-creation and flexible models that mirror the IT services world. Enterprises told us that they need industry-specific insight, flexible contracts tied to outcomes and partners comfortable working in multi-vendor ecosystems. They don’t want a one-stop-shop. They want a collaborator who understands their vertical challenges and is willing to share risk and reward.

In addition, our report highlights three cultural pivots that operators need to embrace if they want to capture the enterprise opportunity:

- Optimise delivery structures: Operators that have established B2B or tech subsidiaries with real autonomy move faster, partner more flexibly, and better serve enterprise clients who expect embedded delivery models and co-creation, not just product sales.

- Close the skills gap: With less than 30% of operator workforces trained beyond basic awareness in AI, operators must rebalance skillsets to reflect B2B demand – particularly in data and software engineering, AI expertise, and security.

- Embrace co-opetition: Operators must be ready to bid as consortia with competitors and ‘frenemies’, moving towards the embedded delivery model used by large IT service providers. The days of trying to own the entire value chain are over.

Signs of progress: Learning from the leaders

Some forward-thinking operators are already showing what this pivot looks like. Verizon has strategically expanded beyond traditional telecommunications to become a key enabler of intelligent manufacturing, focusing on advanced, non-telco-specific services such as AI and M/L to power the factory of the future. By leveraging private 5G networks, mobile edge computing (MEC), and AI-driven analytics, Verizon can support real-time insights, automation and enhanced security directly on the factory floor.

These innovations support critical components like digital twins, robotics and wireless sensor networks, helping manufacturers achieve enterprise Intelligence and transform operations for greater efficiency and resilience.

T-Mobile’s successful bid to become the official telecommunications services provider for the LA28 Olympic and Paralympic Games marks a bold evolution in its approach to delivering next-generation technologies. Moving beyond traditional connectivity, T-Mobile is leveraging its 5G Advanced network to enable immersive fan experiences, real-time data analytics and seamless operations across venues. This partnership showcases T-Mobile’s shift toward integrated, enterprise-grade solutions, combining ultra-fast wireless, edge computing and IoT innovations to support one of the world’s biggest sporting events.

These two examples aren’t just product launches, they represent the cultural and operational shifts we have outlined: dedicated B2B subsidiaries with autonomy, that welcome strategic partnerships to fill gaps and commercial models built around how enterprises want to buy.

GSMA Connected Communities drives Connected Industries

Our research into the evolving B2B landscape for operators is mirrored by the real-world discussions at MWC Las Vegas and within the GSMA Connected Communities initiative, which now includes the new GSMA Mobile AI community.

Both our findings, and the industry dialogue, point to the same imperative: success now depends on operators embracing cultural and structural transformation, prioritising collaboration over ownership, and focusing on vertical-specific outcomes rather than one-size-fits-all offerings.

The GSMA’s Connected Communities initiative acts as a bridge between industries and was originally created to help mobile operators be better informed about the needs of their customers, they stand out as a practical embodiment of this new approach, fostering the partnerships and co-creation that our research identifies as essential for future growth.

By aligning their strategies with these trends, operators can position themselves at the heart of enterprise innovation, but those who stick with yesterday’s B2B playbook run the risk of quickly being sidelined.