There is a large funding gap for essential services in low- and middle-income countries (LMICs). The OECD estimates that $6.9 trillion a year is required up to 2030 to meet climate and SDG objectives. Start-ups and small- and medium-enterprises (SMEs) often struggle to access the right type of financing to achieve impact at scale. This is particularly the case for asset-heavy models or services targeting low-income customers. Our recent report, Digitalising Innovative Finance: Emerging instruments for early-stage innovators in low- and middle-income countries, examined how digital technologies are opening the door to new financing models for SMEs, and improving the effectiveness of more established models. In this blog we look at the emergence of the revenue share model, which was one of five instruments profiled in that report.

Key characteristics and trends in revenue share models

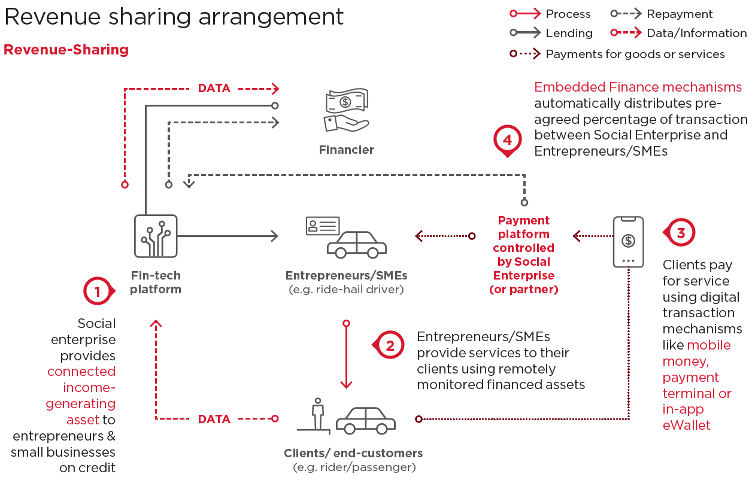

Revenue sharing is a financing arrangement where repayments are based on flow of future revenues rather than fixed repayments, aligning incentives among borrower and lender and distributing the risk. Importantly, financiers will take on a larger portion of the risk as their repayments are based on the success of the business or assets they fund. Revenue sharing has been growing and is an attractive option for many start-ups as these models do not dilute equity, require giving up board seats, or put up any collateral. The figure below outlines how revenue share arrangements can be organised.

Revenue sharing offers significant potential for financing income-generating/productive use assets in, usually, the $5,000 to $20,000 range. It offers companies an alternative path to scaling aside from traditional forms of venture capital funding that are usually aimed at a more narrow set of asset-light and high-growth companies. This can be limiting in utility sectors, which broadly speaking do have much more asset/equipment spending requirements. For example, e-mobility providers or companies supplying PAYG freezers will naturally have more hardware financing needs than fintechs or service based digital platforms.

Revenue sharing itself is of course not at all new or particularly ‘innovative’, the model has been used in joint ventures dating back centuries, was widely applied in the 19th century mining industry, is standard in entertainment in the form of royalties and has become prevalent in the models for the relationship between digital platforms and content creators. However, there are traditional barriers to the model applied in the contexts and sectors of interest that digital technology helps to overcome:

- Critical for revenue-based financiers is line of sight into source data to ensure deals are being honoured according to the agreed revenue share arrangement. Here digital records and data collection through IoT enabled devices provides both more accurate and more trustworthy data that traditional manually compiled records.

- Just as important is line of sight into the cash revenues. Mobile money and other digitalised payments ensure this, and can also automate the process side of the revenue share agreement.

- Revenue share models also work well when operating in conjunction with a digital platform that enables the asset to be used for income generation. The leading use case here is vehicle financing, where those buying the car then go on to use it to make money on ride hailing platforms. A key example here is Nigerian fintech Moove, who just closed a $100 million funding round with backing from Uber and others.

With the rise of startups and SMEs in LMICs opting for a digital first approach to payments and running their services, there will be increased opportunities for these ventures to integrate revenue share arrangements into their financing, and more lenders aiming to provide tailored services to support their growth.

How digitally-enabled revenue share models are scaling

The last few years have seen the emergence and growth of some new key funders in this space. For example, Untapped Global have developed ‘Smart Asset Financing’ offerings based on trackable assets. They exclusively fund digitally-enabled assets on a revenue share basis, and to date have financed over 24,000 micro entrepreneurs who have collectively taken over $35 million in revenues. Unconventional Capital are another financier that use revenue share. They provide collateral free loans up to €50k for entrepreneurs, initially in return for equity, which can then be bought back with future revenues. Revenue sharing models have scaled particularly quickly in India, the revenue-based financing market opportunity in India is already estimated to be at $5-8 billion and is estimated to grow to $40-50 billion by 2025. There, digitally enabled lenders such as N+1 Capital, GetVantage, Klub, and Velocity have been driving the ecosystem forward.

Drawbacks?

The flexibility of the capital provided under revenue share does come with some downsides, as lenders take on more risk under the model the effective interest rate in revenue sharing can be higher compared to other models. If a business performs well, the startups or entrepreneurs may end up paying more in the long run. The revenue share model is also relatively new in many markets and not yet well understood by all. This gives it limited appeal for some investors and makes it difficult to standardise.

Looking forward

The rise of e-commerce and the increased role of technology underpinning business’ revenues, sales, marketing and operations are all key catalyst for growth in the model. As the data and live monitoring, now possible, becomes the ‘new collateral’. The growth potential is particularly pronounced on the African continent, which as of 2022 had only 400 million e-commerce users out of a population of 1.4 billion. Increasingly digitalised transactions, combined with the acute need for financing for productive use assets are the centre of the opportunity. The extent of the scale already seen in the South Asian context, and particularly India, drive home that this is not an abstract moonshot, but rather is a very concrete opportunity for channelling new capital into countries and sectors that have an acute need. Finally, and as with other instruments profiled in the GSMA report, it is worth noting that the investments needed on the digital side to enable revenue share models have benefits that extend beyond the model. The digital monitoring, reporting, and verification (dMRV) of operational data and revenues needed in revenue share provide the foundation for accessing the carbon markets or results-based financing. Similarly, those foundations also provide a sound basis for meeting the due diligence requirements for more conventional capital.

Join our May webinar on: “Digitalising Innovative Finance – Episode Two: Receivables financing and revenue-share models”

Date: Wednesday, 29 May

Time: 11:00 BST | 13:00 EAT | 15:30 IST

LinkedIn LIVE