Authors: Brian Muthiora and Rishi Raithatha

Over the past ten years, East Africa has pioneered mobile money adoption and usage worldwide. As governments in the region cope with a variety of fiscal pressures, the issue of mobile money taxation has naturally emerged.

Kenya, Tanzania and Uganda have all imposed a 10% excise duty on mobile money transaction fees. Other countries have followed suit, with Zimbabwe imposing a $ 0.05 tax on each mobile money transaction and the Democratic Republic of Congo planning to introduce a 3% mobile money tax on turnover.

The mobile industry is already one of the highest taxed in sub-Saharan Africa. Those that offer mobile money thus face three layers of taxation: general taxation such as Value Added Tax; mobile sector specific taxation such as excise duties of 17% on airtime usage and mobile money taxation. While this has a material impact on the investment incentives of the provider, it also does little to support the fiscal objectives of governments.

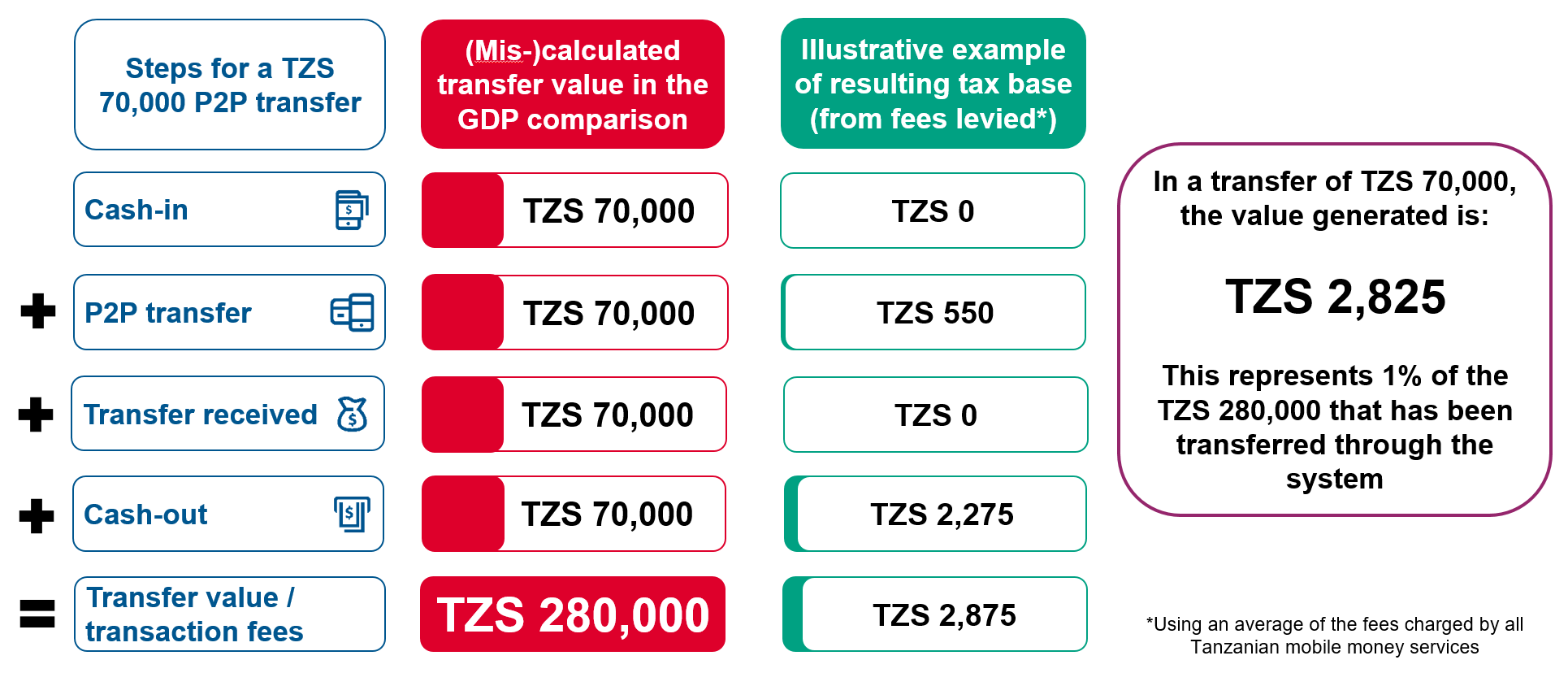

Our recent analysis in Tanzania highlighted that operator fees collected as mobile money taxes amounted to around US$ 8.7 million in the third quarter of 2016 – circa 0.09% of the Tanzanian government’s total expenditure of around US$ 9.23 billion for that quarter. The analysis also went on to demystify the idea that mobile money transactions amount to over 52% to Tanzania’s GDP. A demonstration of the value generated from a single mobile money transaction is shown below:

In this example, based on average fees, the sum of all transactions and the amount of mobile money revenue from those transactions differ by a factor of nearly 100. Any taxes levied by the state would apply to the smaller number.

The gains for public finances from working with providers to digitise payments are potentially significant. Our recent report on person-to-government payments in Kenya demonstrated how government support for mobile money can enlarge the tax base. By digitising payments due to it from motorists, the Kenya National Transportation Safety Authority saw an increase in monthly revenue from US$ 1.1 million in July 2015 to US$ 2 million in October 2016.

Exploring broad-based alternatives to mobile money taxation also stands to deliver better results. Taxation undermines the investment case at a time when mobile operators are already under significant cost pressure to expand networks, improve service quality, and address new regulatory requirements. Moreover, excise taxes, such as those imposed in Kenya, Tanzania and Uganda, are typically used to address negative externalities . They are, for example, imposed on tobacco sales to discourage people from smoking by driving businesses to raise the price of cigarettes. As the mobile sector is associated with overwhelmingly positive externalities, the same rationale does not apply. Mobile money contributes to financial inclusion. It enables more efficient payments for goods and services, reduces the informal economy, creates employment and protects vulnerable segments of society from financial shocks. The positive externalities of mobile money also spill over into other sectors, such as agriculture, healthcare and education. In short, there are strong incentives for the state to support the growth of mobile money, the opposite of what an excise duty is typically designed to achieve.

In a number of countries, mobile money has increased financial inclusion, particularly amongst marginalised segments of society. In Tanzania, for example, 46% of mobile money users are below the poverty line. The negative impact of taxing mobile money transactions is likely to fall most heavily on these individuals.

Rather than levying taxes on the fledgling mobile money industry, governments should consider enabling the growth of mobile money services by digitising the payment of fees, rates, taxes and levies due from taxpayers. This can both expand revenue mobilisation and support the growth of the mobile money sector. Our analysis has shown that taxing mobile money in Tanzania does little to support public finances and to advance the many positive contributions mobile money can make to society.