GSMA Europe’s summer reception in Brussels last month landed at a pivotal time in Europe’s digital journey, as the European Commission’s proposal for a long-awaited Digital Networks Act is expected by year-end. The event featured a session addressing mobile infrastructure investment and its significance for Europe’s digital ambitions.

The GSMA presented fresh insights from Mobile Infrastructure Investment Landscape, a first-of-its-kind global study by the GSMA and Kearney, including a breakdown of the investments made by mobile network operators and other stakeholders in the infrastructure that supports the mobile internet. Investment trends examined in the study offer valuable insights for informing the policy discussion in Europe by delving into the evolving dynamics across the different segments of the connectivity value chain.

Event participants highlighted the continued advancement in mobile connectivity infrastructure across the EU as the decade nears its midpoint, indicating that basic 5G and 5G mid-band coverage have reached 94% and 68%, respectively. Nevertheless, they noted that the deployment of 5G SA within the EU remains limited.

The State of the Digital Decade 2025 report showed that Europe is significantly lagging in the adoption of 5G standalone (SA) networks, with only 2% of 5G users connected via 5G SA infrastructure, compared with 77% and 24% in China and the US, respectively. According to the report, these disparities reveal a growing global divide in 5G evolution and expose the structural and policy hurdles hampering Europe’s shift from 5G non-standalone to true standalone capabilities.

The mobile infrastructure investment landscape: Top-line findings

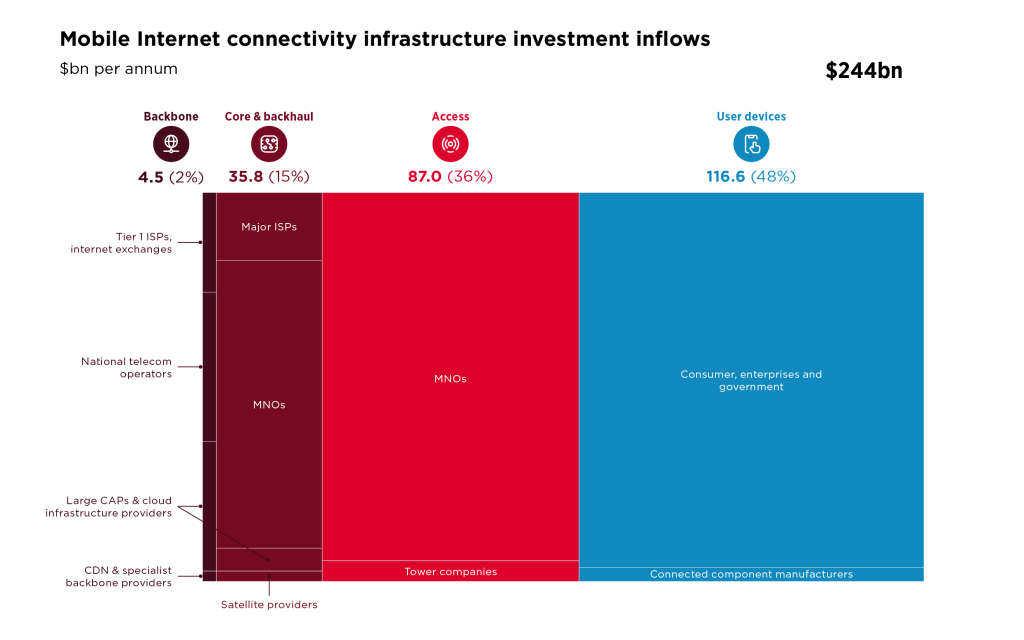

The GSMA and Kearney’s global report provides a comprehensive evaluation and quantification of investments in mobile internet connectivity infrastructure. Within the scope of connectivity infrastructure, we include all assets that make up the communication path between an end user and the end services provided by content and application providers (CAPs). The total investment in mobile internet connectivity infrastructure, averaged over the past 5 years, is $244bn annually, including spend on the connectivity module of the end-user devices.

In Europe (including Russia and Turkey), mobile internet connectivity infrastructure investments account for 16% of the global total.

We summarise the key takeaways here:

MNOs shoulder the lion’s share of the mobile investment

Global mobile connectivity investments, excluding end-user devices, averaged $127 billion per annum between 2019 and 2023. Of this, mobile network operators invest 85% while the rest is split equally between fixed operators offering shared infrastructure to mobile networks (e.g., for backhaul) and other investor groups, including tower companies, satellite providers, large CAPs and cloud infrastructure providers.

MNOs will continue to own the core and access infrastructure

MNOs provide the majority of investment in mobile internet connectivity infrastructure, accounting for 95% of spending in the access segment and 74% in the core and backhaul segments. This trend is influenced by the technical demands and customised configurations of RAN and core systems.

MNOs are adopting virtualisation for their core network systems, utilising private cloud, public cloud, or hybrid environments. Investments in data centre hardware and systems make up 20% of the total investment in the core and backhaul segment, which is higher than the amount invested by public cloud providers in the core and backhaul segment (6%). This indicates that most operators operate their core applications within their own data centres rather than on public cloud infrastructure.

These access and core segments of the mobile internet connectivity value chain require significant capital investment, as their costs scale with traffic volume, have relatively short life cycles, and need continual technology upgrades.

Core and access network investment requirements are several times larger than backbone

The backbone segment of mobile internet connectivity infrastructure has experienced notable shifts in who is investing, with CAPs and cloud infrastructure providers now accounting for one-third of investments in this segment. This trend is primarily driven by these entities’ requirements to interconnect their data centres, employing both direct investments — such as in submarine cables — and the purchase of transport services.

Despite these developments, backbone investment represents only 2% of total investment in mobile internet connectivity infrastructure, excluding end-user devices. Notably, investment in backbone infrastructure is matched by a parallel and much greater investment in core and access infrastructure, which receive 8 to 19 times more funding than backbone infrastructure, respectively.

Past investment should not be taken for granted

The fact is that historical investment levels are not a guarantee of future investment. A number of factors must be in place for operators to have a sustainable business that enables sufficient investment and delivers a reasonable return. The virtual panel, which convened mobile network operators from various markets, offered the following insights regarding operators’ capacity to invest in infrastructure:

- Low return on investment: MNOs have invested heavily in recent years, with capital intensity in some markets exceeding 20%. However, revenues remain flat, with low returns on investment limiting MNOs’ future investment capacity.

- Monetisation challenges: The low average revenue per user (ARPU) in emerging markets, as well as the necessity to maintain affordability, constrain mobile network operators’ ability to monetise their investments.

- Traffic growth: The rapid rise in Large CAP services has driven a traffic explosion that requires massive investments, even as the captured value has shifted away from telcos to large CAPs.

- Efficiency and new revenue streams: Mobile operators are leveraging AI to improve operational efficiencies. Satellite direct-to-device is also being explored in certain geographies to offer public safety-type services. Operators are actively seeking opportunities to monetise their investments and diversify into adjacent markets, such as developing connectivity infrastructure for AI and providing fixed wireless access and enterprise solutions. However, challenges such as low return on investment and limited market preparedness remain significant obstacles.

- Regulatory challenges: The unlevel playing field between players operating in different segments of the connectivity value chain, complex sectoral consumer protection regulations, as well as high spectrum fees are common across different markets.

- Deregulations and simplifications: Speakers shared the views that a holistic review of regulations are needed to ensure that they remain fit for purpose in the context of the current market dynamics and the changes happening in the connectivity ecosystem. Initiatives such as the FCC’s “Delete, Delete, Delete”, the EU simplification agenda under the proposed Digital Networks Act and the Australian financial sector Regulatory Initiatives Grid exemplify governmental efforts to reduce regulatory burdens, enhance productivity, and strengthen industrial competitiveness.

A cutting-edge mobile internet connectivity infrastructure is a key enabler for economic growth, digital competitiveness and innovation. Forward-looking regulatory frameworks that encourage investment in mobile infrastructure, accelerate network expansion, and create a fair and sustainable financial environment for operators are necessary to maintain ongoing investments.