Thursday 12 August, 2021

Executive Summary

The economic benefits derived from legacy network rationalisation

The GSMA estimates that the rationalisation of legacy networks can improve capital intensity – defined as CAPEX divided by revenue (see Annex A) by 1.4% and the ratio of OPEX per revenue by 1.3%. This is due to the possibility of a 7~11% reduction in CAPEX and 4~6% reduction in OPEX for a typical mobile network operator in a developed market.

The biggest contribution to the reduction of capital intensity derives from the refarming of spectrum, specifically the low-band spectrum used in the provision of 2G/3G access. In conjunction with refarming, reducing the complexity in multi-access networks, decommissioning of ageing equipment and other optimisations in energy efficiency further contribute to decreasing the costs of operating a mobile network.

Key case study learnings

For operators considering rationalising their network, the GSMA makes the following recommendations:

- Limit the procurement of devices that support legacy networks (e.g. 2G-only devices).

- Communicate with customers to make them aware of alternative options prior to rationalisation to ensure a seamless service.

- Maintain a comprehensive mapping database that includes accurate device and subscriber-device information to help identify the best targets for rationalisation.

- Calculate the cost and complexity of replacing single-mode M2M devices as part of the rationalisation process.

- Ensure availability of affordable multimode devices or devices that support VoLTE in price sensitive markets.

Acknowledgement

Special thanks to the following Mobile Network Operators for their contributions to this document: Bharti Airtel, China Unicom, Chunghwa Telecom, Far EasTone, StarHub and Telstra

1 Overview

1.1 Data demand drives the need for network rationalisation

With each new mobile network generation, subscribers have enjoyed an increasing amount of functionality and faster data speeds. Indeed, 5G promises to continue this trend by delivering a step-change in average data speeds with latency lower than ever before. As well as improving the mobile broadband experience, 5G is also perfectly placed to efficiently support the expected phenomenal growth in the number of connected “things”.

Recent mobile network generations have also increased their spectral efficiency, that is, their capability of carrying data in a given amount of spectrum. This means they can carry far larger volumes than ever before. For example, for each hertz of spectrum, a 2G system can carry 0.1 bits of information per second while in comparison, 4G can carry 2.4 bits, or an improvement of 24 times.

While the improvement in network capacity and capabilities brought by 5G is welcomed, especially in consideration of the ever-increasing demand for mobile data (see for example CISCO VNI 2017), for many operators who offer already today services across three different network generations (2G, 3G and 4G), the deployment of 5G will result in increased complexity as well as cost in their network operations.

To address the cost and complexity problem, operators in several markets around the world are working on network rationalisation.

This document will discuss the key strategies and lessons learned for an operator wishing to rationalise its legacy mobile systems.

Note: Rationalisation of legacy networks in this document is defined to be either closure or scale-down of mobile networks that operate on second or third generation (2G/3G) mobile technologies.

1.2 Advantages of rationalising legacy networks

1.2.1 Spectrum considerations

The principal reason behind legacy network rationalisation is the improved spectral efficiency of 4G and 5G technology.

Figure 1. Illustrative spectral efficiency evolution (Source: 5G Americas)

As user consumption behaviour changes from voice-centric to data-centric, improved spectral efficiency is required to address the increased data demands of mobile subscribers. Currently, it is difficult for 2G and 3G networks to meet this demand.

Figure 1 illustrates that using the latest version of 4G makes it possible to deliver over the same amount of spectrum about 4 times the data rates that can be delivered by the most advanced 2G technology.

As well as data throughput, the improvement also benefits the delivery of voice services. By migrating from circuit-switched voice service (2G and 3G) to voice over IMS (VoLTE) it is possible to support, within the same spectrum resources, a much larger volume of voice calls.

Another important consideration is that 2G is deployed in many countries in 900MHz spectrum, which has more favourable propagation characteristics than spectrum above 1GHz, where many LTE systems operate. This means that when deployed in the traditional 2G frequencies, LTE cells can provide better coverage and in-building penetration.

Although the refarming of spectrum currently used by legacy systems requires careful planning and execution as well as, in some regions regulatory clearance, the benefits in terms of system capacity and user experience are indisputable.

1.2.2 Operational benefits

Legacy network rationalisation is beneficial because it reduces the network operation and maintenance costs in the 5G era. These cost benefits come from:

- Decommissioning of Equipment. Although the costs of the legacy equipment are fully amortised for many operators, the cost of the software licenses and the maintenance of ageing equipment can be avoided.

- Simplification of Operations. Each mobile generation has its own set of equipment, procedures and management system that are taken care by highly trained specialists in the operators’ Network Operation Centres. By rationalising the network it is possible to reduce the complexity of the network management.

- Reducing Energy Consumption. New technologies tend to be more energy efficient than their predecessors, moreover the physical space occupied by a site could be reduced/optimised.

A further consideration in terms of operational benefits is that in advanced markets with only a small number of subscribers of legacy networks (especially 2G networks), the revenue generated from those networks is unlikely to recover the running costs of maintaining those networks.

1.4 Lessons learned from legacy network rationalisation use cases

1.4.1 Lesson #1: Focus procurement on multimode devices and away from devices that can only connect to legacy networks

It is essential to stop the supply of 2G-only (or any generation of network that an operator intends to shutdown) handsets to prepare for legacy network rationalisation. In the same context, operators should ensure that dual-SIM card handsets provide services over not only 2G but also 3G (or even VoLTE if both 2G and 3G are to be closed) for all SIM cards they serve. Furthermore, multimode devices should be configured such that they prefer next-generation networks (e.g., 3G/4G for 2G closure case) over the legacy network that is going to be rationalised.

1.4.2 Lesson #2: Make sure customers are aware of your plans to rationalise the network and create bespoke offers for them if they are going to be affected

Whilst most regulators require operators to make an announcement well ahead of legacy network rationalisation, operators should ensure that their intention to close down a legacy network is publically communicated well in advance to allow customers time to migrate to a new service and change their handsets. Following the announcement, operators should then deploy a multi-channel strategy to communicate the rationale and subsequent marketing offers and technical support to affected customers. See Table 1 for actions taken by operators in the cases discussed in this document.

| Customer Type | Channel | Actions |

| Post-paid | Phone calls, SMS, Mail | – Phone calls / SMS encouraging handset upgrade – Mail with bespoke offers for new 3G/4G handsets |

| Enterprise post-paid | Account Manager | – Letters on quarterly basis with attractive handset offer – Webpage to educate customers on 2G closure and way forward |

| Prepaid | SMS, Retail, Webpage | – Campaigns at prepaid hotspots – SMS notifying 2G closure – Posters in retail channels – Webpage to educate customers on 2G closure and way forward |

Table 1 Actions taken to communicate 2G closure to customers

Operators should also offer incentives and technical support where necessary. Attractive deals for new devices to replace legacy devices are critical to migrating the technology laggards and sceptics. Enterprise customers would need a dedicated team to manage VPN solutions and other enterprise-specific issues, such as legacy IoT devices (see section 1.4.4 below). For consumers, store lessons and online instruction videos on new devices (e.g., smartphone lessons for the benefit of 2G feature phone subscribers) would be recommended.

1.4.3 Lesson #3: Have comprehensive and accurate device information and subscriber-device mapping to identify the correct target for your 2G/3G closure campaign

Specific subscribers using devices that connect only to legacy networks (e.g., 2G-only devices) are the targets for marketing communications and subscriber engagement. This, however, first requires operators to know whether a particular device model can only connect to legacy networks and whether a particular subscriber is using that device model. To resolve this issue, operators need to have a comprehensive and accurate device map (with device capabilities) along with correct mapping of the device model with subscribers.

One method to achieve this is by capturing the IMEI of subscribers, mapping IMEIs to corresponding device models and maintaining an accurate device map that outlines capabilities of different device models. Although the first method can be handled internally (standardised device integrity check procedures are already available), the other two require consolidation of multiple industry sources and manual revisions by experts. Operators can use other device management solutions or methods to facilitate this process.

1.4.4 Lesson #4: M2M devices in legacy networks require replacement with multi-mode devices, or operators need to consider sharing national legacy network infrastructure to serve legacy devices that are difficult to replace

As many M2M devices are “life critical” (i.e. need to be constantly functioning) or may be difficult to locate and access (e.g., within dark subway tunnels), having M2M devices using the legacy network poses obstacles to full legacy network shutdown. LTE-based LPWAN solutions (NB-IoT, LTE Cat.M) standardised by 3GPP provide a good option for operators to replace these legacy devices with newer multi-mode models. Alternatively, where allowed by regulation, operators within the same market can choose to establish a joint venture that can consolidate and operate the legacy network infrastructure of these operators (i.e. infrastructure sharing). This may be more cost-effective in the short term.

1.4.5 Lesson #5: Markets with a high price sensitivity need affordable multimode or standalone 4G devices in order to effectively migrate customers from legacy networks

In markets where low-end devices are popular, affordable smartphones supporting 4G (with 4G+4G capabilities for dual-SIM devices) are required to switch customers to next-generation networks. In this context, development of low-cost devices with 4G-only capability and VoLTE support are essential, and operators should consider collaborative actions to leverage economics of scale to develop such devices.

2 Case Study: Telstra

2.1 Market overview

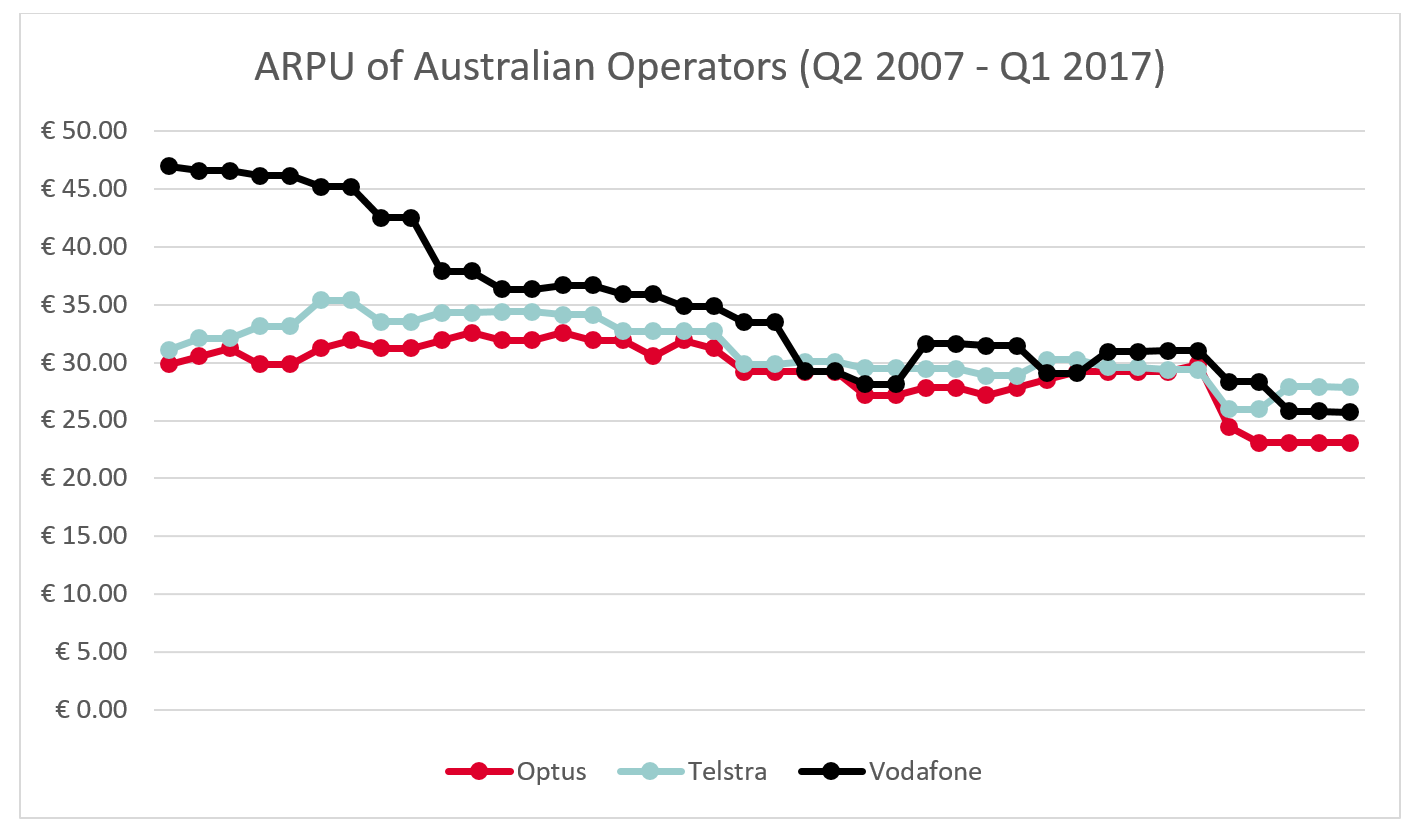

Telstra is largest mobile operator in Australia. They provides comprehensive services to customers ranging from fixed telephony and internet and mobile communications to television and content services. The Australian mobile market is quite advanced with a smartphone penetration of 80.69% and LTE penetration of 67.01% (Source: GSMA Intelligence). However, ARPU for Telstra and other operators in the Australian market have been in decline (See Figure 1).

Figure 2 ARPU of Australian Operators from Q2 2007 to Q1 2017 (Source: GSMA Intelligence)

Given the market context above, it seems logical why Telstra closed its 2G (GSM) network in December 2016.

2.2 Why 2G closure?

The primary reason Telstra closed its 2G (GSM) network was because of changes in their customers’ behaviour. Many customers moved from primarily using voice/SMS to predominantly using data. This was in stark contrast to 2006 where 99% of network capacity usage was for voice and only 1% was for data. The pattern had now completely reversed with 98% of usage for data and only 2% for voice. Clearly, in a data-centric world, it would be more suitable to utilise technologies designed for mobile broadband/data access (3G or 4G) than maintaining a 2G network primarily designed for voice calling.

There were also very few 2G subscribers left when the decision was made to rationalise this network. Rather than utilising spectrum and infrastructure assets for legacy technology catering to a minority, it would therefore be more rational to utilise these assets for more efficient next-generation technologies.

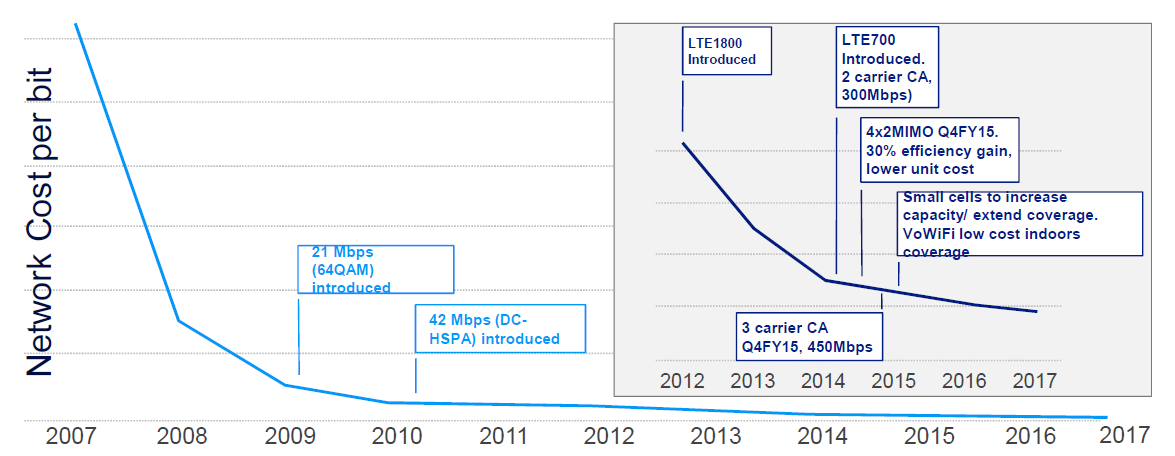

In addition, the operation of 2G involves significant costs which the revenue generated from it does not cover. There are also explicit costs such as energy and power as well as maintenance. Equally, there are implicit/opportunity costs for the operation of 2G networks. More effort is required to keep up training and knowledge of what is essentially “old” technology. Secondly, and more importantly, the greater spectrum and infrastructure efficiency provided by 3G/4G is expected as valuable spectrum and equipment space assets are tied up in the operation of 2G. This creates significant opportunity costs. Figure 2 shows the decreasing network cost per bit as technology advances.

Figure 3 Network Cost per bit (peak network speeds) (Source: Telstra)

Lastly, there are social reasons associated with the better connectivity provided by 3G or 4G. Better connectivity has been proven to be beneficial for society as social, health and banking services can be more accessible for customers and their delivery is more stable. This creates positive feedback and contributes to national economic growth (i.e. GDP growth).

2.3 Challenges in 2G closure

Although closing 2G networks has numerous benefits, closing down a live network is a very challenging task even when the network has few subscribers. The most challenging aspect is in the engagement and persuasion of 2G customers. Persuading enterprise customers to migrate from 2G to next-generation technologies can be difficult as the enterprise customers do not perceive immediate dissatisfaction with current services while migration may risk operational stability. For consumers, getting the message to them could be more challenging as they are often less engaged to outbound communications from their operator.

Devices are also a critical challenge in closing 2G. Replacing 2G only devices has to proceed before the 2G network is closed because the subscriber will not be able to connect to Telstra’s mobile network otherwise. In addition, there are complexities and benefits that arise from replacing devices such as upgrading SIM cards to the latest versions with the latest security algorithms, transferring information from one SIM card to another, changes in settings and user frustration in adapting to new UI/UX.

Lastly, M2M devices require more consideration. This is because a large proportion of services on Telstra M2M were life critical devices used in alarms, safety situations and health monitoring and replacing these devices while not disrupting their function was very challenging. Devices used in smart and remote metering are also often located in difficult or remote locations. Furthermore, most M2M devices were not purchased directly from Telstra and it is difficult to identify end users of services that are affected by these devices without the use of comprehensive analytics and early engagement with the customers.

2.4 Lessons learned and potential enablers

To address the challenges of consumer engagement, Telstra announced its 2G network closure in 2014 via an extensive marketing campaign. They issued over a million letters, SMS messages and over 850,000 outbound phone calls and was involved in over 200 media stories. Telstra also provided support over their website, advertised the announcement through external media and raised internal staff awareness to ensure all possible channels were utilised to reach their subscribers and potential customers. Telstra also actively managed enterprise customer migration. It allocated a dedicated team to manage VPN solutions and actively migrated customers to resolve any issues that arising from the enterprise customers’ solutions/devices.

Telstra tackled the serious challenge of devices with three measures. Firstly, they provided in-store lessons on using smartphones as approximately 75% of 2G consumer customers were baby-boomers and user frustration on switching to completely new type of devices had to be managed. Secondly, Telstra conducted a free handheld device campaign, where over 80,000 devices were provided. Although an operator cannot provide devices to all its 2G subscribers, this is a good way to accelerate adoption of 3G/4G. Lastly, Telstra carefully planned device procurement and initially provided the high-end customers with devices that support 2G and 4G (along with VoLTE) to reduce the number of 2G-only devices. The other segments were later addressed with procuring lower cost devices with 3G and 4G or 4G-only capability and VoLTE support.

M2M probably required the most subtle consideration. Telstra first reached out to industry bodies to identify end users of services from re-sellers that would know exactly what devices and customers needed to be migrated.

Telstra recognises that not all networks and countries are the same and that 2G closure may present different challenges. Some of the ways to address these may include the creation of a joint venture or single MVNO on a single network for use by all operators in the market. This would free up spectrum and can provide a cost-effective solution to address M2M devices. This joint venture could be allocated a small portion of the 2G spectrum while other portions could be used by the operators for 3G/4G. Furthermore, an infrastructure sharing solution MOCN could provide seamless access to the 2G network layer whilst the 3G/4G networks operate independently.

Finally, although not as major as the lessons learned above, Telstra believes that there are two more enablers for 2G closure that operators should consider. Software-defined radio can be considered to split and migrate traffic from 2G to 4G, as it is software can be easily configured to migrate from 2G to 4G rather than having to replace the radio access.

In addition, in many countries that are heavily 2G reliant today, the move directly to 4G would be most efficient. The mass availability of low-cost VoLTE phones would facilitate such a migration directly to 4G, however, this may also lead to the potential for a material penetration of smartphones requiring regular software updates and app updates. In countries with limited fixed infrastructure and Wi-Fi access, these upgrades could be problematic so the inclusion of LTE-Broadcast would be able to address operating systems and app updated scalability issues as LTE subscriber base grows.

3 Case Study: Bharti Airtel

3.1 Market overview

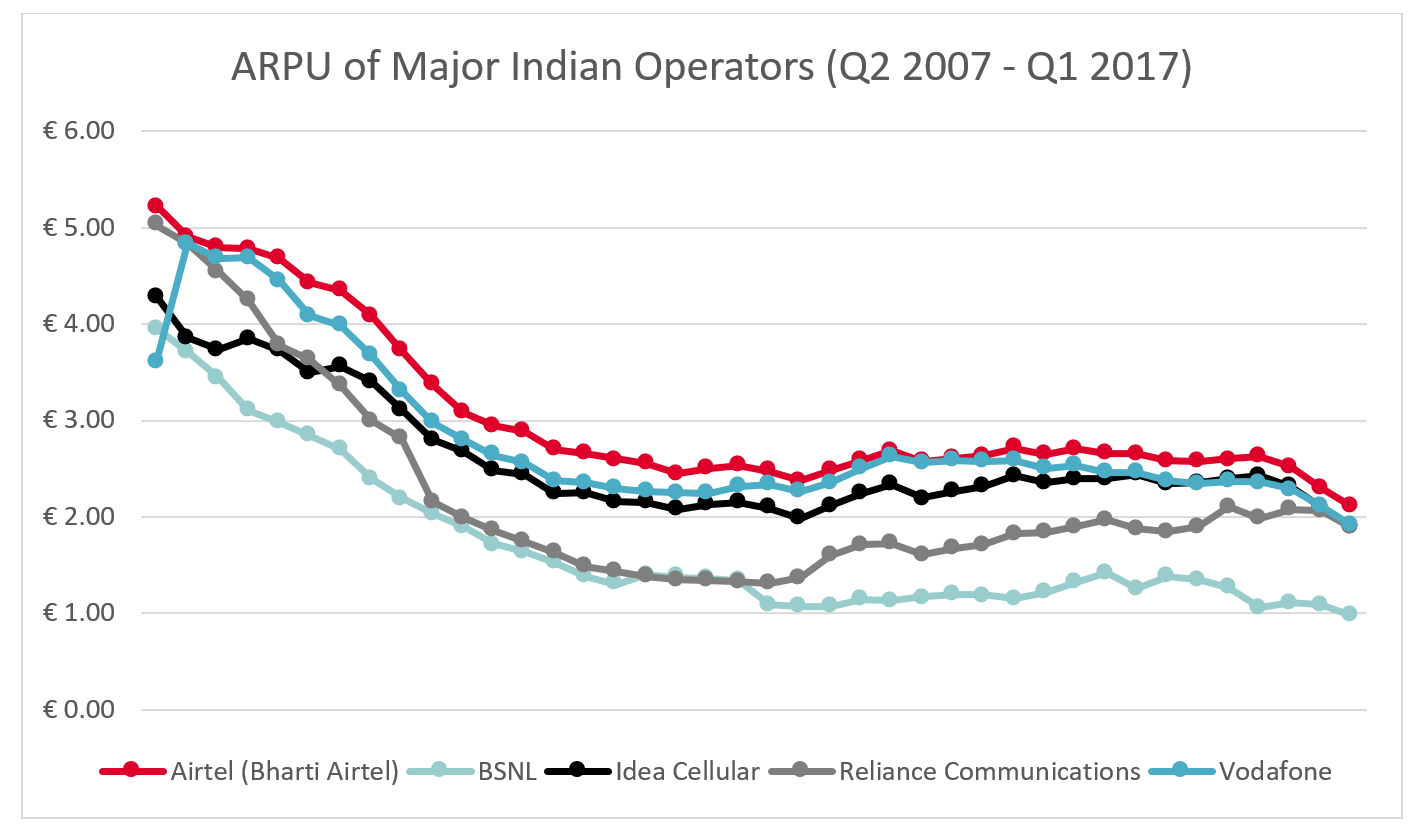

Airtel is the market leader in the Indian mobile market (consisting of more than 10 operators) with a market share of 33%. Airtel provides comprehensive offerings to customers ranging from fixed telephony and internet to mobile communications to television and contents services. The Indian mobile market is still developing with smartphone penetration of 35% and 2G penetration of 65% (LTE device penetration is 50% of total smartphones). The ARPU per connection for major Indian operators (Airtel, BSNL, Idea Cellular, Reliance Communications and Vodafone) have been in declining trends and Airtel is no exception although it has the highest ARPU.

Figure 4 ARPU of Major Indian Operators from Q2 2007 to Q1 2017 (Source: GSMA Intelligence)

In the light of these market contexts, Airtel is looking to reduce their costs and allocate more share of their spectrum to broadband to expand business opportunities, which requires rationalisation (minimising capacity and spectrum) of 2G networks. This case study will provide rationales, challenges and lessons learned from Airtel’s experience in the rationalisation of legacy networks.

3.2 Why legacy network rationalisation?

Rationalisation of 2G is a natural choice as Airtel are exploring ways to expand their business opportunities. In terms of spectrum, 24% of spectrum owned by Airtel is allocated to 2G and 76% on higher-order networks (3G (18%), FD-LTE (20%) and TD-LTE (38%)) currently. This means that only 24% of spectrum is used to carry 80% of total voice traffic within Airtel. Smartphones account for more than 40% of the total devices in Airtel’s network, which can be served by 3G and 4G networks.

As mobile broadband is the next step of evolution in mobile communications, it is in the best interest of Airtel to minimise spectrum used for voice traffic while maximising spectrum for data traffic. Indeed, Airtel has already succeeded in re-farming 900MHz spectrum band on a live network from 2G to 2G and 3G using Lean UMTS (using 4.2MHz bandwidth).

In October 2017 Airtel announced their intention to start shutting down their 3G network from 2020 onwards. Airtel has already ceased investing in 3G network equipment, and there is a high possibility that Airtel’s 3G network would shut down faster than the 2G network.

3.3 Challenges in 2G rationalisation

For Airtel, the challenges in rationalising 2G lie in the 2G network, which handles 80% of voice traffic, contributes to 60% of their revenue (out of Airtel’s India mobility revenues of approx. USD 8bn, 2G revenues are USD 5bn and USD 3bn are from 3G and LTE respectively). This means that hasty rationalisation of 2G networks may jeopardise the stability of 2G voice services and have a serious impact on Airtel’s reputation and voice revenue.

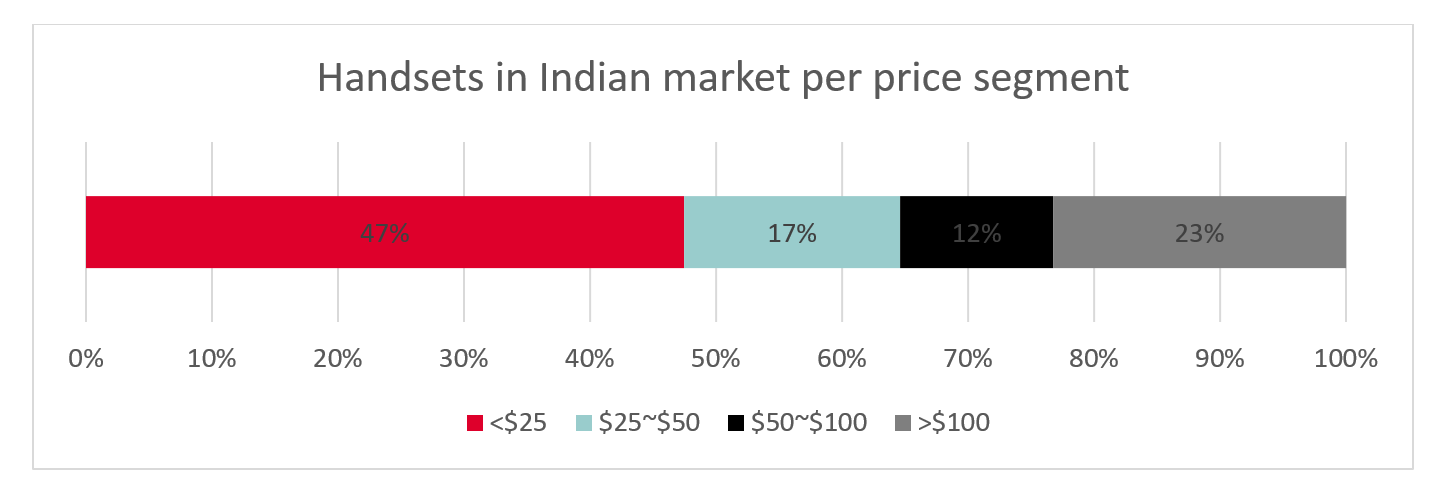

Furthermore, as declining ARPU trends and low ARPU (in the range of EUR2.00~3.00 in 2017) indicate, India is a cost-sensitive market. Figure 5 below shows that 47% of the handsets in the market are in the price segment of below USD 25, and only 23% of handsets are over USD 100.

Figure 5 Classification of handsets in Indian market per price segment

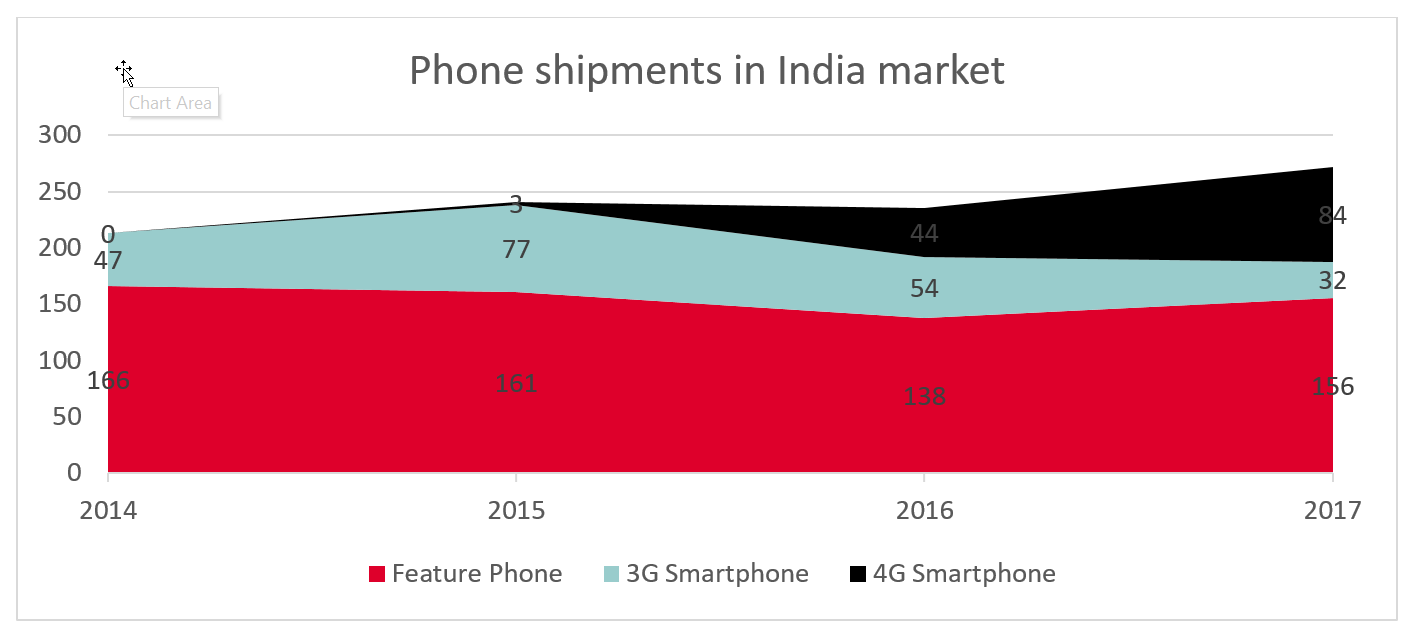

Finally, although smartphone penetration is rising, there are still over 750 million 2G-only handsets that are still active in the Indian market. In fact, over half of the devices that are shipped today in India only support 2G. This is a challenge that must be addressed because subscribers with 2G-only devices can only be served by 2G networks and this leaves less room for 2G rationalisation

In addition, 90% of the smartphones in India support 4G+2G mode, which means the operator’s SIM placed in a secondary slot can only be used for 2G technology irrespective of the network provided by the operator.

Figure 6 Phone shipments in India market (millions)

3.4 Rationalising 3G network

In January 2017, 4G devices accounted for less than 35% of all smartphone shipments in India. Fast forward to October 2017, and this number has jumped to nearly 70%. At the same time, 2G feature phones still account for about 40% of all mobile shipments. Allied to the fact that there have been no shipments of 3G-only devices in India over the past two years, the conclusions are unequivocal – India as a device market is divided sharply into two segments: 2G feature phones and 4G smartphones.

From a pricing perspective, 4G handsets are more affordable than ever before. The cheapest smartphones in India now retail at Rs 2500 (US$35). Operators provide further subsidies of up to Rs 1000 on the back of strategic partnerships with device manufacturers (Vodafone with Micromax, Reliance Jio with Lyf), and that brings the price down to an eminently affordable range of Rs 1500 (US$20).

With the LTE layer picking up voice (VoLTE) and data traffic from smartphones, 3G network traffic is decreasing rapidly as 2G networks continue to carry the bulk of voice traffic from feature phones. In such a case, it makes far more sense, given the efficiency of 4G networks to refarm 3G spectrum to 4G services. The spectrum licence conditions are technology neutral, which makes the case for migrating to 4G purely an economic argument.

3.5 Lessons learned and potential enablers

Airtel believes that affordable smartphones supporting 4G (with 4G+4G capabilities for dual-SIM devices) are necessary to reduce the share of 2G traffic in the Indian market. This is because the Indian market is very cost sensitive and customers will only switch from 2G to 4G when they can afford the devices.

In addition, phones that support 2G and other networks (3G/4G) should be configured such that they prefer the 3G/4G networks when possible. For example, “2G only” mode in smartphones should be switched to “preferred network type: LTE/3G/2G” to ensure that devices that are not 2G-only attach to 3G/4G whenever possible. In addition, dual-SIM devices with LTE and GSM SIM card should be encouraged to migrate to LTE and LTE/WCDMA SIM cards with promotions and incentives.

To ensure the stability of 2G network operations while diverting spectrum to mobile broadband use, Airtel is collaborating with technology providers to develop dynamic spectrum sharing which allows LTE and GSM to coexist in the same spectrum band. Airtel plans to implement this scheme in the top 7 metro cities by 2020 such that those cities will not require dedicated spectrum for 2G. The scheme will then be expanded to rural areas.

Airtel has articulated a clear strategy to switch from 3G to 4G. Pan-India VoLTE on the Airtel network is a top priority and will be completed by the first quarter of 2018. Since the 3G spectrum licence is technology neutral, Airtel intends to take a phased approach in migrating 3G to 4G, starting with the 2100 MHz band in select cities, with at least one carrier dedicated to 4G (in a dual carrier setup). Most newer 3G sites are also capable of powering 4G, so a software upgrade with minimal hardware changes will more than double the capacity of current 3G sites. Older sites will need equipment upgrades but Airtel has a clear business case which shows that the cost per GB of serving a 4G customer drops so significantly compared to 3G that this migration exercise becomes profitable very quickly.

3.6 Summary

2G rationalisation is critical for re-farming spectrum to 4G and delivering a better user experience. This can be achieved by reducing traffic on 2G network which would need the following interventions

- Affordable 4G smartphones

- Enabling 4G dual-SIM devices (at least with DSDV – Dual-SIM Dual VoLTE capabilities)

- Disabling “2G-only” mode in devices and enabling the network to control traffic prioritisation

- Dynamic spectrum sharing between 2G & 4G

Re-farming 3G spectrum for 4G services is also high on Airtel’s agenda. The total number of 3G handsets on the Airtel network has been steadily falling at a rate of more than 3 million a month, whilst the price of affordable 4G smartphones is also decreasing at a rapid rate. Over the next few years, Airtel intends to accelerate the shift away from 3G to 4G in a staged approach:

- Strategic tie-ups with device manufacturers to promote affordable 4G devices

- Providing pan-India VoLTE coverage by early 2018

- Converting at least one carrier from a dual-carrier setup (900/2100) to 4G

4 Case Study: StarHub

4.1 Market overview

StarHub is the first runner-up in the Singaporean mobile market with a market share of 27.57%. StarHub provides comprehensive offerings to customers ranging from fixed telephony and internet, to mobile communications, to television services. Moreover, the Singaporean mobile market is quite advanced with a smartphone penetration of 83.52% and an LTE penetration of 83%. However, ARPU for StarHub and other operators in Singapore have been in a declining trend as figure 1 indicates.

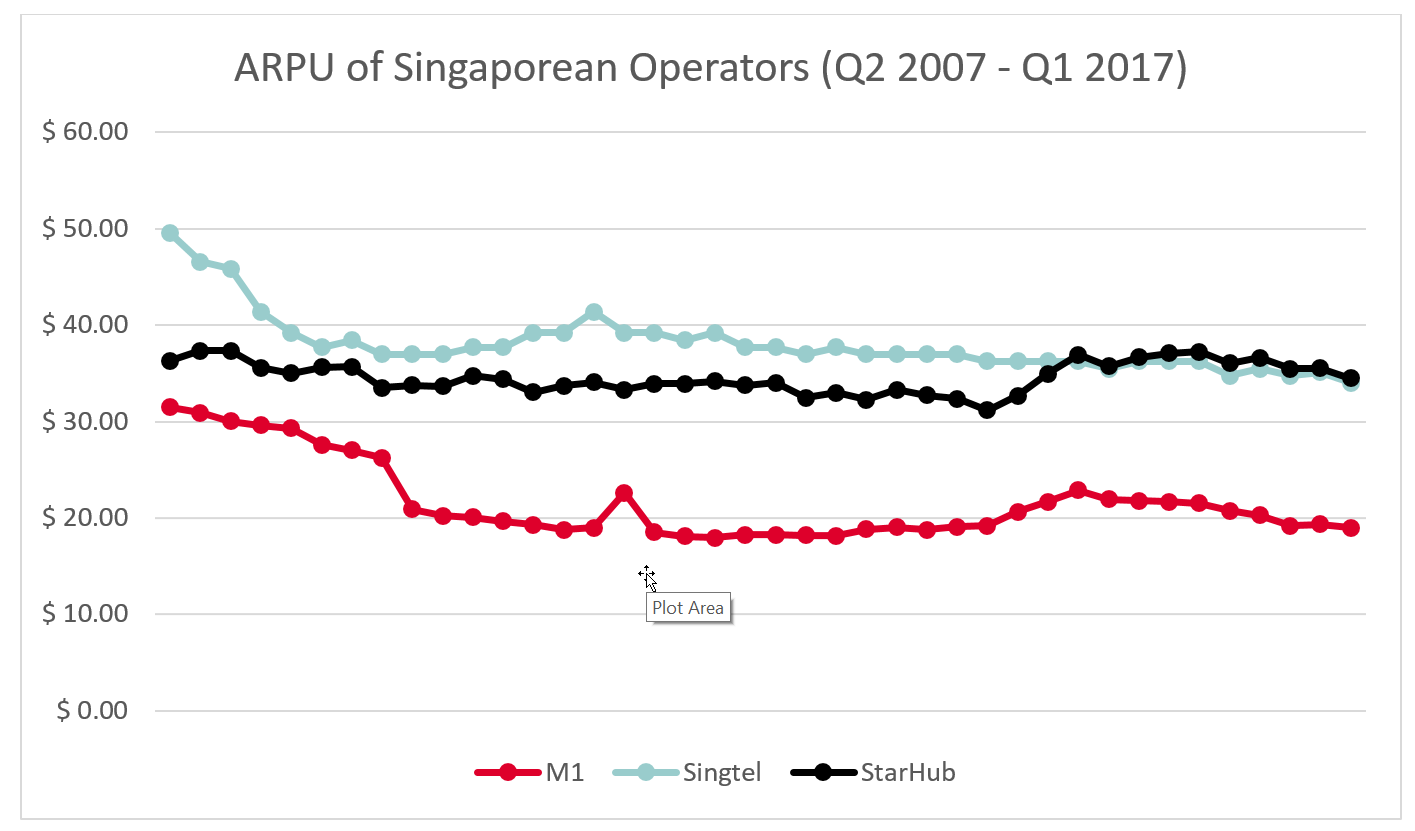

Figure 7 ARPU of Singaporean Operators from Q2 2007 to Q1 2017 (Source: GSMA Intelligence)

In light of these market contexts, it seems natural that StarHub closed its 2G (GSM) network in April 2017. This case study will provide the history, rationales, challenges and lessons learned from StarHub’s experience.

4.2 History of 2G closure in Singapore

Unlike many other cases, StarHub’s 2G closure case is unique as mobile operators in Singapore collaborated in requesting the regulator’s approval to shut down the 2G network in 2014. This was because the majority of mobile traffic was on 3G and 4G networks even at the time and Singaporean operators wanted to focus on high-speed data traffic demand.

In 2015, StarHub and other Singaporean operators’ request for 2G cessation was approved and the operators started a public announcement of their plans to close 2G in 2017 (i.e. 2 years prior to the closure). In addition, the regulator ceased to “type-approve” 2G-only handsets, 18 months before the closure, to ensure that the number of 2G-only subscribers would not increase. During this time operators continued to enhance their 3G and 4G networks to accommodate their existing 2G subscribers, this was complemented by reducing the quality of service on 2G networks in 2016 to motivate 2G subscribers to upgrade to 3G/4G services.

In 2017, approval to sell new 2G-only handsets ceased and StarHub closed their 2G network on 1 April 2017.

4.3 Why 2G closure?

The major driver behind StarHub’s 2G closure was to free up spectrum for the deployment of high-speed data networks such as LTE. The closure of 2G enabled re-farming or reallocation of 2G spectrum to move to more spectrally efficient technologies, that were more suitable for mobile broadband. This was a natural choice for StarHub as an operator residing in an advanced market with very high smartphone and LTE penetration rates. This also lead to customer benefits as they could enjoy an enhanced data and communications experience once they were upgraded to later technology such as 3G/4G.

In addition, 2G closure lowers the overall cost to maintain the mobile network. As network operation is simplified from maintaining 2~3 separate generations to 1~2 generations, operation and maintenance costs can be reduced. Furthermore, closing 2G means that 2G equipment is no longer required from the operator, which means that physical space could also be freed up at both the base station and data centre.

4.4 Challenges in 2G closure

One of the challenges faced by StarHub in their journey to close the 2G network was the availability of cheap 2G handsets in the market for customers to stay on the 2G network. Since 2G-only devices tend to be low-end, price sensitive customers often choose and stay with these devices. This means that high handset or retention subsidies were required to entice these customers to move to 3G. In addition, most 2G subscribers tend to be in an older demographic and educating these consumers to convert to 3G/4G required investment and time to persuade the consumers.

This consideration also applied to enterprise customers that used inexpensive 2G devices (for both communications and machine-type communications use). Machine-type communications using 2G devices were common among enterprise customers managing fleets and sensor applications.

Lastly, whilst the 2G network shutdown was done in phases, it required coordination among the Singaporean operators to minimise the impact it had on consumers. As it is often more difficult to collaborate with external organisations, coordination in 2G network shutdown required delicacy and a collaborative mindset.

4.5 Lessons learned and potential enablers

From StarHub’s experience, it is essential to cease supply of 2G-only handsets to prepare for 2G closure. If an operator intends to close their 2G network but still sells 2G-only handsets, the process is likely to be delayed as an influx of 2G subscribers will not cease and would require sustained communication and education efforts.

StarHub’s experience suggests that collaboration among mobile operators may be more effective in obtaining approval for closing 2G networks. Singaporean operators requested regulator’s approval to close 2G networks together in 2014 and they were able to obtain permission in 2015. As this became a topic on the national agenda, regulators were also more proactive in communicating closure of 2G services with the operators.

Lastly, the most important lesson learned is communication of 2G closure to 2G subscribers. In addition to letting customers know that the 2G network will be closed, attractive offers for new 3G/4G handsets also had to be provided to entice these same customers. The following table shows StarHub’s approach to different types of customers in communicating 2G closure.

| Customer Type | Channel | Actions |

| Post-paid | SMS, Mail | (In-contract) Regular SMS encouraging handset upgrade (Out-of-contract) Mail with attractive offers for new 3G/4G handsets |

| Enterprise post-paid | Account Manager | Letters with attractive handset offer Webpage to educate customers on 2G closure and way forward |

| Prepaid | SMS, Retail, Webpage | Campaigns at prepaid hotspots SMS notifying 2G closure Posters at retail channels Webpage to educate customers on 2G closure and way forward |

Table 2 Communicating 2G Closure to Customers (StarHub experience)

5 Case Study: China Unicom

5.1 Market overview

China Unicom is the first runner-up in the Chinese mobile market with a market share of approximately 19% and subscriber base of 269.6 2 million as of Q2 2017. Their ARPU per connection is not as great as their competitors, but China Unicom has been successfully closing the gap with their competitors by tackling the decreasing trend of ARPU.

Figure 8 ARPU of Chinese Operators from Q2 2007 to Q1 2017 (Source: GSMA Intelligence)

5.2 Why 2G closure?

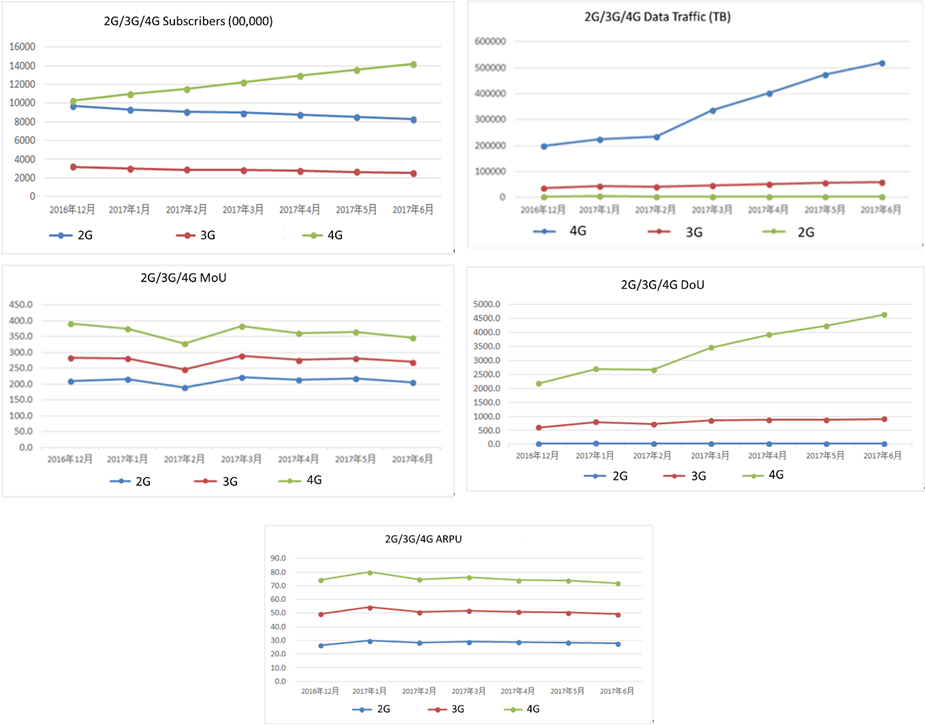

The commercial driver for 2G closure is mainly from the analysis of 2G / 3G / 4G users’ key indices analysis, including the analysis of subscriber numbers, analysis of data traffic, analysis of MoU(monthly Minutes of Usage), DoU(monthly Data of Usage) and ARPU(Average Revenue Per Unit) trends.

Firstly, with the rapid development of 4G data services, the indicators show that 4G is significantly more promising than 2G. The following subscriber charts show that 2G users are decreasing monthly, whereas the 4G user base is increasing. For data services, 4G traffic is increasing rapidly whilst 2G is more suitable for voice services than for data services. 4G MoU remained stable, but 4G users’ MoU is 1.3 – 1.7 times more than that of 2G users. 4G DoU is rapidly growing, while 2G DoU remains flat. For the APPU, 4G and 2G users both exhibit a constant trend, but 4G ARPU value can be up to 1.8 to 2.8 times that of 2G users’ value.

Figure 9 Various indices indicating change from 2G to 3G/4G is necessary

Secondly, the 2G network occupies the 900Mhz and 1800Mhz spectrum bands which are attractive for wide coverage. Operators hope that through network structure optimisation and spectrum re-farming, these bands can be released and reused for 4G. In addition, 2G network equipment is reaching the end of its lifecycle, which means it will have higher energy consumption and maintenance costs.

5.3 Challenges in 2G closure

In terms of business revenue, 2G voice traffic was slowly declining, but the total amount of 2G voice and 3G voice traffic was essentially the same. If the 2G network was shut down suddenly and 2G voice wasn’t diverted to 3G/4G, then it could lead to a loss of voice revenue.

China Unicom’s 2G devices accounted for 28.4% of the current network as of June 2017. This was reduced by about 1.2% every month. The main type of 2G devices are 2G industry terminals (IoT terminals), function terminals (for the elderly and children) and other domestic operators’ customised devices with China Unicom’s SIM card. As the cost of a 2G-only terminal is low, other domestic operators will not close their 2G network within 3-5 years. This means that the number of 2G-only terminals will not be easily reduced and will delay China Unicom’s 2G closure progress significantly.

Enterprises and verticals also bring challenges to China Unicom. In some provinces, 2G industry terminals (IoT terminals) accounted for 20% of all 2G-only terminals. As the cost of multimode terminals is still high, the deployment of new networks to suit multimode terminals is costly. In addition, even if the 2G-only terminals are all replaced by multimode terminals, the cost of replacement will be still very high also.

Roaming is another challenge. As the inbound roaming voice service is provided over 3G, the inbound roamers that have a 2G-only handset will not be able to access voice services in China Unicom’s network.

5.4 Lessons learned and next steps

For 2G industry terminals (2G IoT terminals), China Unicom is promoting 2G IoT/NB-IoT/eMTC multimode terminals. According to the development of multi-mode terminals and network deployment, China Unicom will gradually use multi-mode terminals to replace 2G IoT terminals.

For existing dual-SIM card handset, the second card slot generally only provides a 2G voice function. This will encourage users to stay on 2G and not to migrate to 3G/4G up. Therefore, the 2G and WCDMA voice services should be provided on the secondary card at the same time such that users can choose to use 2G or WCDMA voice according to the network. Consequently, users will be able to migrate to 3G/4G and operators will not be required to retain 2G service.

5.5 Conclusion

- Regulators need to discourage 2G-only handset to be deployed in the network

- Promote low cost 2G/3G/4G multimode terminals

- For dual-SIM handset, promote WCDMA voice on secondary SIM slot

- Capital intensity and cost reduction opportunities

- Definition of capital intensity

Capital intensity is defined to be the capital expenditure (CAPEX) divided by the revenue: CAPEX/Revenue. Whilst the absolute magnitude of CAPEX is also important, this concept looks into the normalised expenditure to accommodate differences in the size of the mobile operators.

The technical definition of capital intensity is total assets over revenue, where this definition can indirectly measure the effects of CAPEX and OPEX because assets are influenced by the costs. However, this definition can be influenced by many other factors and therefore is not used.

- CAPEX/OPEX reduction framework

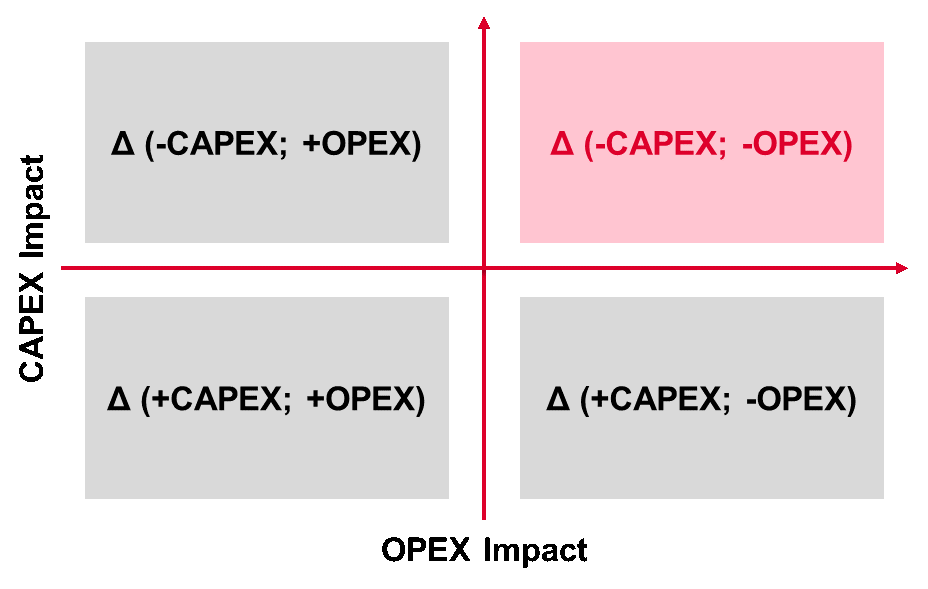

To explore the cost reduction opportunities fully, it is important to consider the reductions in the ratio of OPEX per revenue than to focus on capital intensity alone. It may be that reduction of capital intensity does not necessarily lead to the fall of the ratio of OPEX per revenue. Therefore, we also propose a framework to evaluate the CAPEX/OPEX reductions as follows.

Figure 10 CAPEX and OPEX Impact Framework

For 2G/3G closure, we expect the impact to lie on the 1st quadrant (shaded in red) as it enables reduction of both CAPEX and OPEX.

- Document Management

- Document History

| Version | Date | Brief Description of Change | Approval Authority | Editor / Company |

| 1 Nov 2017 | Section 5 China Unicom case study is validated | China Unicom | LV Guagnxu /China Unicom | |

| 20 Nov 2017 | Section 2 Telstra case study is validated | Telstra | Mike Wright /Telstra | |

| 28 Nov 2017 | Section 3 Bharti Airtel case study is validated | Bharti Airtel | Bharti Airtel | |

| 29 Nov 2017 | Section 4 StarHub case study is validated | StarHub | CHONG Siew Loong /StarHub | |

| 1.0 | 29 Nov 2017 | New White Paper | PSG | Michele Zarri / GSMA Kelvin Qin / GSMA Dongwook Kim / GSMA |

- Other Information

| Type | Description |

| Document Owner | GSMA Future Networks Programme |

| Editor / Company | Michele Zarri / GSMA Kelvin Qin / GSMA Dongwook Kim / GSMA |

| Reviewed & Approved by | Future Networks Programme Steering Group (listed in alphabetical order): · America Movil · China Mobile · China Telecom · China Unicom · Deutsche Telekom · KDDI · KT · Millicom · MTS · NTT DoCoMo · Orange · SK Telecom · Telefonica · Telenor · Turkcell · Vodafone |

It is our intention to provide a quality product for your use. If you find any errors or omissions, please contact us with your comments. You may notify us at prd@gsma.com

Your comments or suggestions & questions are always welcome.