Last week Bill and Melinda Gates released their annual letter summarising their foundation’s progress and laying out their priorities for the coming years. Titled “Our Big Bet for the Future,” the letter sets a series of ambitious goals for the next 15 years that include spreading the adoption of digital financial services to help eradicate extreme poverty.

Innovation plays a critical role in pursuing digital financial inclusion…

“Traditional banks cannot afford to serve the poor because of their costs… [However] by making small commissions on millions and millions of transactions, mobile money providers can make a profit serving poor customers, just as brick-and-mortar banks do serving the wealthy.”

…and regulation is cited as one of the major barriers to implement this vision:

“There is a lot of work ahead to get regulators in developing countries to update their financial regulations. If the regulations limit digital banking, as is still the case in most countries, innovators can’t enter.”

This is not a new approach for the Bill & Melinda Gates Foundation, which has been implementing its digital strategy for financial inclusion since 2012. In a paper that addresses some of the key drivers of this strategy, the Foundation’s Dan Radcliffe and Rodger Voorhies have pointed out that mobile payments and transfers are the building blocks of digital financial inclusion. Mobile money services, they argue, have great potential to give millions of people access to payment and transfer services, to store their money safely, and “to build low-cost ‘on-ramps’” for accessing a broader range of financial services. Once mobile money becomes ubiquitous in a country, other services such as savings, credit and insurance can be provided. Ecosystem growth is occurring through various partnerships between operators and financial institutions (banks, insurance companies, and microfinance institutions) and other third parties (e.g. governments, employers, retailers, etc.). Enabling digital payments and transfers is the first step to creating universal access to a broad range of financial services and improving the stability and integrity of the financial system, thus fostering socio-economic empowerment of individuals and communities.

State of play: mobile operators are driving digital financial inclusion

Mobile money services are available in 89 countries through 256 live deployments,[i] 60% of which are operationally driven by mobile operators. Operators, seeing the benefits of economies of scale, have invested heavily in the development of innovative services that are making an important contribution to financial inclusion. When compared with banks, microfinance institutions and payment service providers, I believe that the level of commercial investment by mobile operators into inclusive financial services is unprecedented.

GSMA’s annual Global Adoption Survey of Mobile Financial Services has consistently shown that of the fastest-growing deployments, the vast majority are driven by mobile operators (figure 1).[ii]Therefore from a regulatory perspective, one basic requirement for mobile money to succeed is to create an open and level playing field that allows non-bank mobile money providers, including mobile operators, into the market.

FIGURE 1. GROWTH OF INDIVIDUAL MOBILE MONEY SERVICES SINCE LAUNCH (JUNE 2013)

An enabling regulatory approach: required basic elements

Where allowed to sustainably provide mobile money services, mobile operators are playing a critical role in the development of more efficient and inclusive financial sectors. Regulators that have created a “window” for non-banks to enter the mobile money market under their guidance have taken a critical first step.

Allowing for competition in the provision of mobile money services is necessary, but not sufficient on its own. Our analysis of service providers based on data from the GSMA’s Global Adoption Survey has identified additional elements are necessary to unleash the potential of non-banks and enable the mobile money market to grow.

By an ‘enabling regulatory approach’ we mean that by implementing the recommendations of global standard setters – such as the Bank for International Settlements (BIS) and the Financial Action Task Force (FATF) – the regulator has taken a functional and proportional regulatory approach that allows banks and non-bank providers to compete as well as to establish different types of partnerships for the provision of mobile money services. More specifically, the rules established by the regulator:[iii]

- Permit non-banks to issue electronic money (or equivalent)[iv] by allowing them to:

- be licensed directly, OR

- set up a subsidiary for this business, OR

- apply for a payments bank (or equivalent) license, OR

- provide the mobile money service under a letter of no-objection to the non-bank or its partner bank, pending the approval of a specific regulation.

- AND impose initial and ongoing capital requirements that are proportional to the risks of the e-money business

- AND permit them to use agents for cash-in and cash-out operations

- AND do not prescribe the implementation of specific interoperability models without allowing for a market-led approach.

Regulatory barriers are slowing down financial inclusion

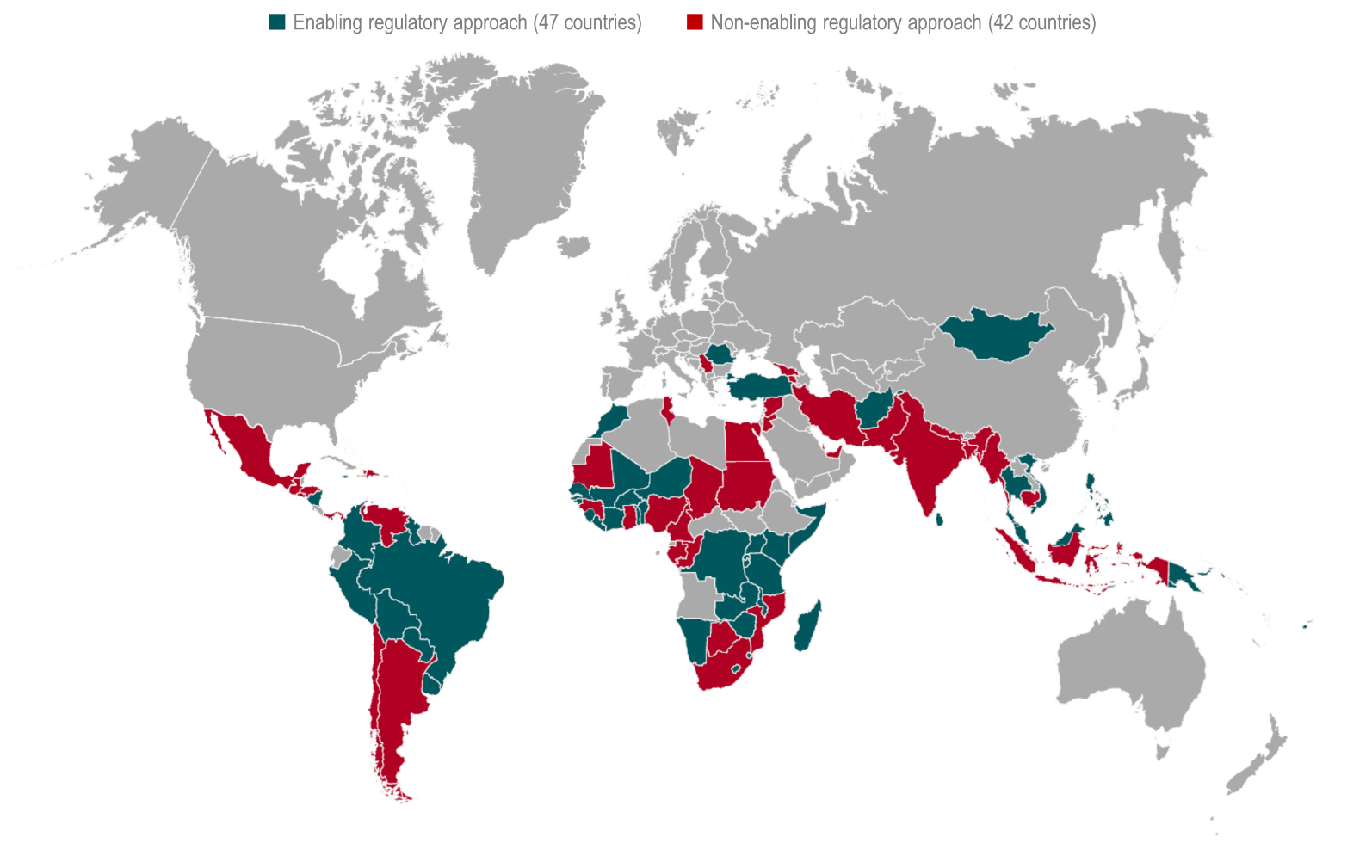

Of the 89 markets where mobile money is live, only 47 markets have an enabling regulatory approach,[v] while in the other 42 markets regulatory barriers still exist.[vi]

FIGURE 2. MOBILE MONEY MARKETS BY REGULATORY APPROACH (DECEMBER 2014)

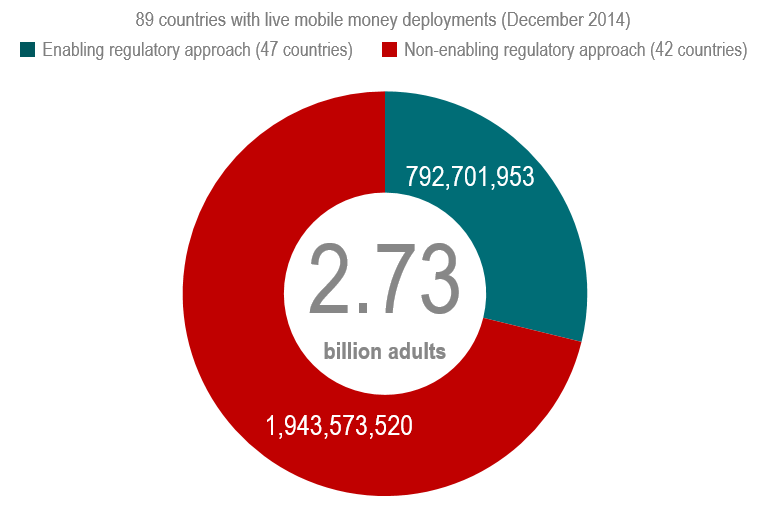

The aggregated adult population of the 89 countries where mobile money services have deployed is 2.7 billion adults. Unfortunately, the vast majority of this population lives in countries with non-enabling regulation (see Figure 3).

FIGURE 3. ADULTS LIVING IN COUNTRY WITH LIVE MOBILE MONEY SERVICES, BY REGULATORY APPROACH (DECEMBER 2014)

The existence or absence of an enabling regulatory approach has a dramatic impact on the development of the mobile money market and on financial inclusion. Enabling regulation is critical to unleashing market potential because it affects:

- the provider’s ability to build a functional distribution network to increase financial access; and

- customer adoption and use of the service

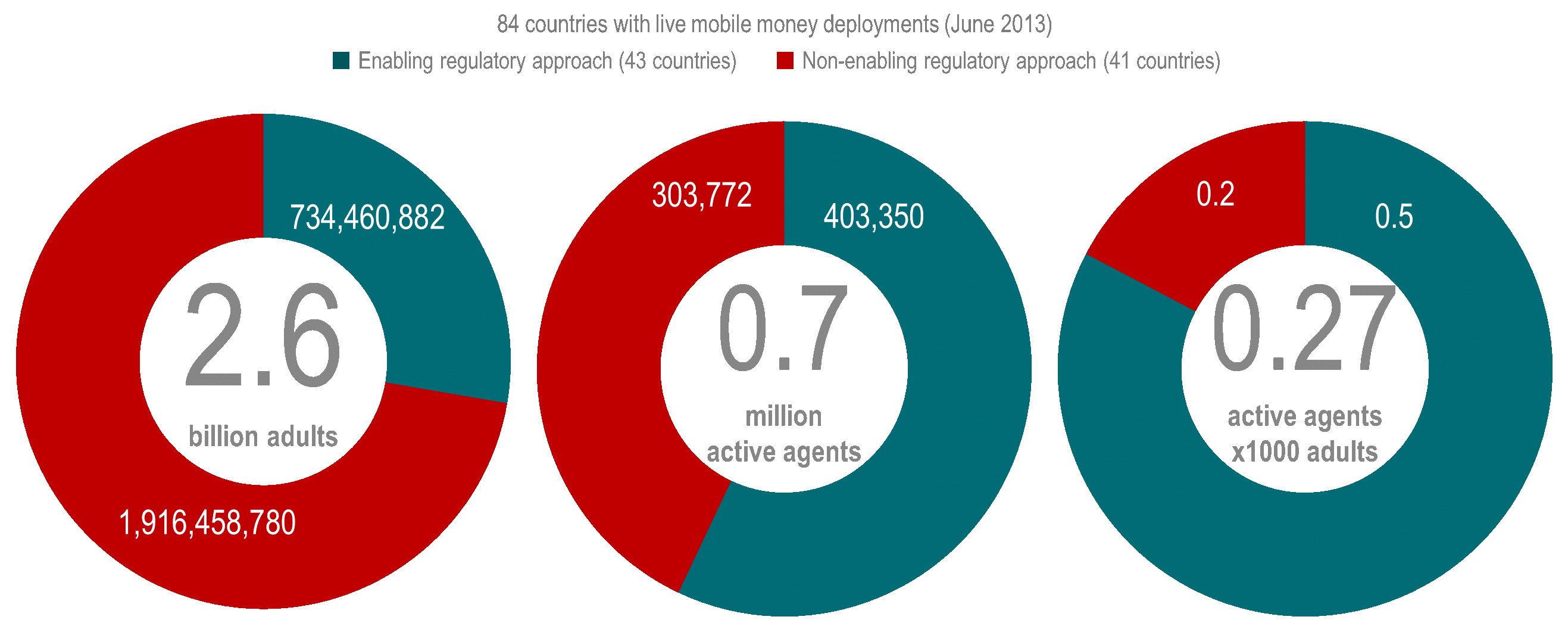

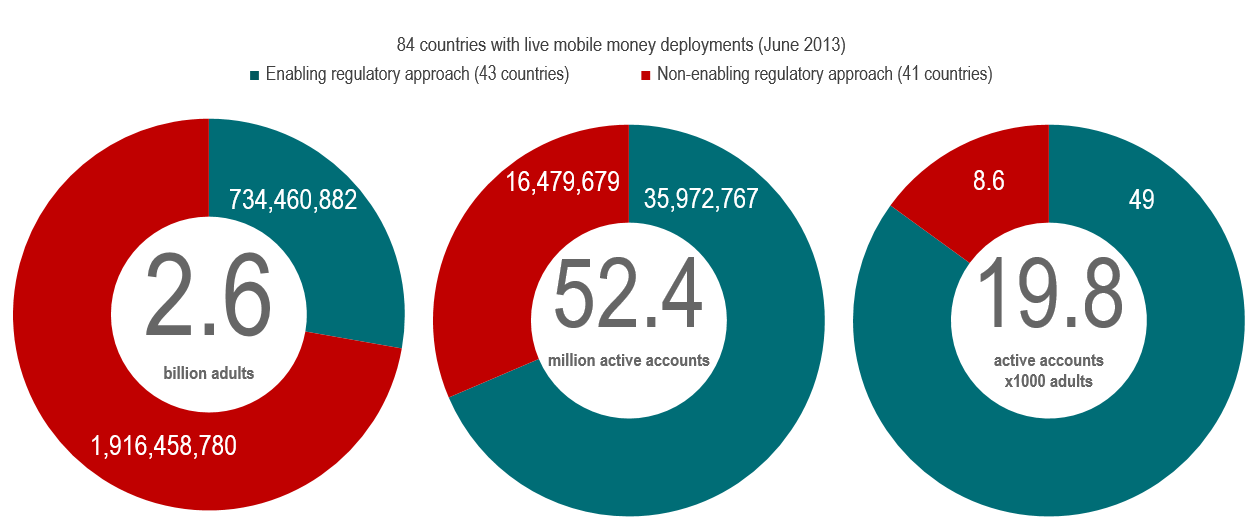

As shown below, even though most adults live in countries with non-enabling regulation, the number of active agents (Figure 4) and active customers (Figure 5) is significantly higher in those with enabling regulation.

FIGURE 4. FINANCIAL ACCESS: ACTIVE MOBILE MONEY AGENTS (JUNE 2013)

FIGURE 5. FINANCIAL INCLUSION: ACTIVE MOBILE MONEY CUSTOMERS (JUNE 2013)

Regulation: A priority to achieve financial inclusion

Bill and Melinda Gates are absolutely right in identifying regulatory barriers as one of the main priorities to address in order to achieve financial inclusion. We need to open all markets to competition among all players (banks, MNOs, and other third parties), fostering ongoing innovation in terms of services and partnerships that will reduce the cost of the services and further increase outreach.

Countries that have most recently approved enabling regulations include Brazil, Liberia, Colombia and Kenya. Ghana is close to approving new regulations that will be a radical departure from the conservative approach taken in 2008. Madagascar and Tanzania are codifying their successful approaches, while Mozambique is working to improve theirs. And in 2014, the Tanzanian regulator made two decisions that have benefited mobile money customers and the growth of the market: they allowed operators to begin implementing interoperability (based on a model and timeline that was determined among the operators themselves); and they allowed providers to distribute the interest accrued in the mobile money escrow account.

India has also recently made great progress in terms of regulatory reforms, although there are still elements in the 2014 Payments Banks Regulations (such as high capital requirements and limitations on foreign ownership) that may limit their (positive) impact. Unfortunately, other potentially big mobile money markets such as Indonesia, Nigeria, Mexico, Egypt and Francophone Central Africa are lagging behind in terms of market development and require regulatory reform to facilitate participation by non-bank providers.

Out of the 52 developing countries where mobile money is not yet available, there are 12 with populations of more than 10 million where the regulatory approach appears to be slowing down the launch of services.[vii] The total adult population of these 12 markets is 204,376,494.

We at the GSMA are convinced that a structured and efficient dialogue between the public and private sectors is necessary to establish an informed and transparent policy making process whose outcome will foster financial inclusion. We are actively working to support this dialogue and hope that all countries will soon have open markets that encourage competition, proportional requirements that ensure the safety and soundness of mobile money services without burdening providers with unnecessary compliance costs, and the ability to offer desirable features such as the distribution of interest earned on the float. With these elements in place, mobile network operators will be able to expand the availability of payment services and other financial services and foster the development of more efficient and inclusive financial sectors.

Notes

[i] GSMA, Mobile Money for the Unbanked Deployment Tracker, https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/tracker/.

[ii] Early analysis from the GSMA 2014 Mobile Financial Services Adoption Survey confirms evidence already provided by the previous year’s Survey. Every year the GSMA publishes an overview of the quantitative and qualitative information gathered through its annual survey in the GSMA Mobile Financial Services State of the Industry Report. The 2013 Report is available here https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/wp-content/uploads/2014/02/sotir/_2013.pdf. The next report will be presented at Mobile World Congress in March.

[iii] These rules may be codified or may be outlined in individual “Letters of no- objection.

[iv] In some cases, regulators authorise providers to offer such services under a different name, such as “mobile money”, “mobile payment”, or “electronic deposit”.

[v] These markets are Afghanistan, Benin, Bolivia, Brazil, Burkina Faso, Burundi, Colombia, Cote d’Ivoire, Democratic Republic of Congo, Fiji, Guinea-Bissau, Guyana, Jamaica, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mongolia, Morocco, Namibia, Nicaragua, Niger, Papua New Guinea, Paraguay, Peru, Philippines, Romania, Rwanda, Samoa, Senegal, Sierra Leone, Singapore, Somalia / Somaliland, Sri Lanka, Swaziland, Tanzania, Thailand, Togo, Tonga, Turkey, Uganda, Uruguay, Vanuatu, Vietnam, Zambia and Zimbabwe.

[vi] These markets are: Argentina, Armenia, Bangladesh, Botswana, Cambodia, Cameroon, Chad, Chile, Congo Brazzaville, Dominican Republic, Egypt, El Salvador, Gabon, Georgia, Ghana, Guatemala, Guinea, Haiti, Honduras, India, Indonesia, Iran, Jordan, Mauritania, Mauritius, Mexico, Mozambique, Myanmar, Nepal, Nigeria, Pakistan, Panama, Qatar, Serbia, Solomon Islands, South Africa, Sudan, Syria, Tunisia, UAE and Venezuela.

[vii] These markets are Algeria, Angola, Cuba, Ecuador, Iraq, Kazakhstan, North Korea, South Sudan, Syria, Ukraine, Uzbekistan and Yemen. China is not included in this list because we are currently researching this market to understand the nature of the services offered and the underpinning regulation. More information on China will be presented in the 2014 Mobile Financial Services State of the Industry Report.