The widespread nature and affordability of mobile makes it the perfect vehicle to bridge the infrastructure gap that people in low- and middle-income countries often face. Mobile is also the gateway to life-enhancing services such as mobile money, which is undoubtedly contributing to increasing financial inclusion in emerging markets.

However, women tend to be consistently left out of the picture. Data from the Global Findex 2014 shows that women in low- and middle-income countries are 36 per cent less likely than men to access and use mobile money, which translates to 1.9 billion women worldwide. But this number masks greater imbalances at both the regional and country level. For instance, while in Sub-Saharan Africa the gender gap in mobile money ownership stands at 19.5 per cent, in Niger it is 60 per cent. In South Asia women are 67 per cent less likely than men to have a mobile money account.

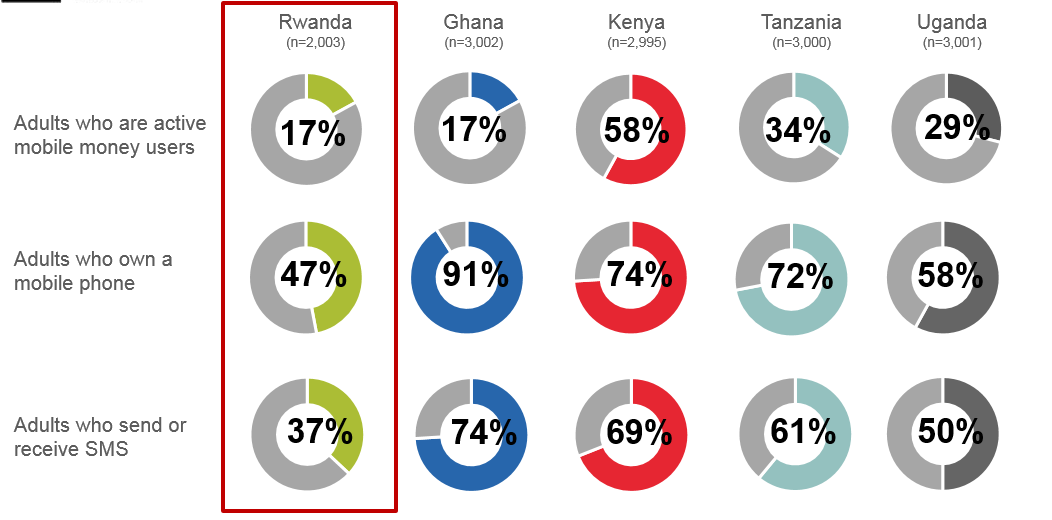

How mobile money is contributing to financial inclusion in Rwanda

Rwanda is a dynamic mobile money market and the existence of a formal national ID system has contributed to financial inclusion via mobile money. To date, 37 per cent of Rwandan adults are considered financially included . 23 per cent of Rwandan adults or nearly two thirds of those who are financially included, have a mobile money account . 17 per cent of Rwandan adults are 90-day active mobile money users, at the same level of Ghana and not too far behind Uganda. In Rwanda, mobile money is catching up rapidly in spite of low literacy levels and handset ownership . This is impressive, especially if we consider that the first mobile money service in Rwanda was launched in 2010, while in Kenya and Ghana mobile money has been live since 2007 and 2008, respectively.

Source: FII data

In Rwanda, women are 20 per cent less likely than men to have a mobile money account . To better understand the origins of this gender gap, we decided to focus on the barriers that prevent women from accessing and using mobile money at the same rate as men. Also, in order to understand how the barriers affect different female mobile money users, we decided to assess what separates a regular female mobile money user (here defined as a user who has carried out at least one P2P/month on average over the last three months) from a power mobile money user (here defined as a user who has carried out at least one P2P/week on average over the last three months).

These insights allowed us to come up with some concrete suggestions on how to better reach women with mobile money in Rwanda. In order to do this, we conducted 40 semi-structured interviews and five focus group discussions, with women and men that are regular and power users of mobile money. Men and women were kept in separate groups to ensure that the opinions shared during the discussion were unbiased. All the interviewees lived in Kigali and were between 25-34 years of age, so the results may look different in rural areas.

Some barriers prevent women from accessing and using mobile money at the same rate as men

Price sensitivity

Our research showed that the women in the study tended to be more price sensitive than men to the fees associated with making a mobile money transaction. This can be partly explained by the fact that women often have a lower disposable income than men – as they were much more likely than men to do unpaid housework, they had lower income levels. Also, when women worked outside of the house, they were more likely to be employed in jobs that earn lower wages.

While men were more likely to value the convenience offered by the service over the fees, the opposite was true for women. Women therefore tended to find ways to avoid what they felt were unnecessary charges. Also, women were more likely to send mobile money more frequently and in lower amounts than men, leaving them more exposed to transaction fees. This pattern may be explained by women’s lower levels of disposable income compared to men, as mentioned earlier on.

Lower confidence and understanding

Women in the study were much less confident than their male counterparts in their ability to make a mobile money transaction. There was a widespread perception, both among men and women that finance and technology are not traditionally female domains leading to the perception that women are less knowledgeable and less confident in these areas. Also, women were less mobile than men, meaning that they were less likely to be exposed to people who transact regularly and to opportunities to learn how to use the service, which fuelled the perceived sense, of both men and women, of lower understanding.

Low levels of trust

Lower levels of understanding of how the mobile money service works, make women less likely to trust the service with their money. Also, women who reported having low trust in the service were likely to complain about negative customer service experiences, or of the negative customer service experienced by others. Finally, more so than men, women preferred to use the bank for larger amounts of money, as banks were perceived to be safer than mobile money. As such, women seemed to be more likely than men to store money on their mobile money account up to a certain amount, at which point they would withdraw the money and deposit it into a bank, deemed more trustworthy with larger sums than mobile money.

In the next blog, I’ll explore the reasons why women like using mobile money, and I will compare regular and power users of mobile money, to understand how the barriers impact them differently.