Start-ups and small and medium enterprises (SMEs) in low- and middle-income countries (LMICs) often struggle to access the right type of financing to achieve impact at scale. This is particularly true for asset-heavy models – such as e-mobility, energy, or productive use equipment – or ventures targeting low-income customers such as clean cooking, WASH, or off-grid solar.

Our recent report, Digitalising Innovative Finance: Emerging instruments for early-stage innovators in low- and middle-income countries, examined how digital technologies are opening the door to new financing models, and improving the effectiveness of more established models. In this blog we look at the emergence of receivables financing, which was one of five instruments profiled in that report.

Receivables financing is particularly important for climate tech ventures in sectors such as e-mobility, off-grid solar, or productive use. These companies rely on working capital to finance inventory purchases and consumer credit solutions to support their pathway to scale but can face high costs of capital particularly across many African countries.

As IEA research has demonstrated, in Africa, the cost of capital for clean energy projects is two to three times higher than in advanced economies and China. The high cost of capital largely reflects two sets of perceived risks: 1) country-specific risks and 2) sector or technology-specific risks. These include currency and macroeconomic risks, as well as other considerations such as investors’ familiarity with investing in a given market or sector or the track record and reputation of a given company/project.

Receivables financing can be a useful tool for climate tech ventures in LMICs and can help them address some of these challenges by lowering the cost of capital at scale, improving cash flow access, and reducing foreign exchange risk.

Key characteristics and trends in receivables financing

Securitisation is a process in which certain assets are pooled to be repackaged into interest-bearing securities. Gaining prominence in the 1970s, securitisation was initially used to finance self-liquidating assets such as mortgages in the United States. But any asset with a stable cash flow can theoretically be structured into a portfolio that supports securitised debt. Examples include corporate and sovereign loans, consumer credit, project finance, lease/trade receivables, and individualised lending agreements.

Receivables financing is a financial method where businesses use their outstanding invoices as collateral to secure immediate cash from lenders or financial institutions. These institutions, also known as ‘factors’, buy the right to collect a firm’s invoices (often through an isolated Special Purpose Vehicle (SPV) or a factoring company) from its customers by paying the firm the face value of these invoices, minus a discount (see Figure 1). By securitising future flows of receivables, private companies in LMICs can access international capital markets and get immediate access to working capital. However, to enter such arrangements, companies will need to operate at a certain scale to the extent that they have a large enough book of receivables to be pooled into a portfolio.

Figure 1: A hypothetical receivables financing arrangement

The global growth in receivables financing has been driven by momentum in trade and supply chain finance. Though best suited for asset or goods-focused operations, receivables financing has also been a financing instrument for infrastructure projects across LMICs. The total value of factoring in Africa is projected to reach $100 billion by 2030. In Asia, demand for receivables financing is growing at an average of 7% annually, but is concentrated in a few key markets and dominated by formal banks and large corporations.

Receivables financing arrangements in PAYG solar

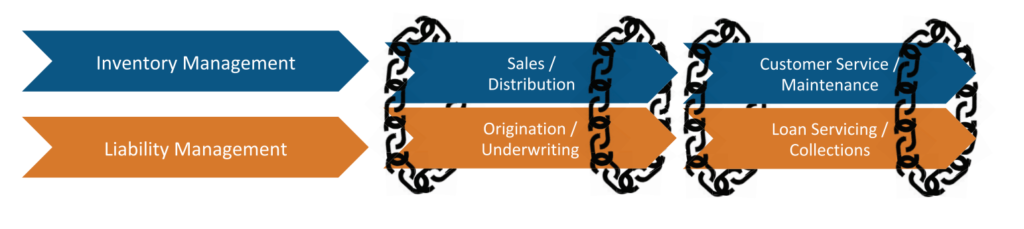

Receivables financing in the context of pay-as-you-go (PAYG) financing models in LMICs has been a topic of discussion for over a decade. Though only in the last few years have we begun to see major deals. Key to understanding the value of off-balance sheet receivables financing to PAYG companies is the nature in which inventory and liability management are linked across the PAYG sector (see Figure 2). The quality of servicing has huge implications for the likelihood of non-payment by a customer. Conversely, repayment rates across a company’s portfolio have implications for a company’s ability to access the capital needed to effectively service customers and scale.

Figure 2: Servicing linkages between PAYG value chains

By collateralising receivables and isolating operator risk through off-balance sheet financing structures, PAYG companies have been able to meet working capital needs on favourable terms, access liquidity without increasing insolvency risks, and focus on operations and sustainable growth. At the same time, they have introduced many lenders to a new asset class with a strong ESG profile, and isolated them from some of the operational and market risks associated with selling products based on credit to a low-income customer base with seasonal or irregular incomes.

One of the earliest receivables financing arrangements in the PAYG solar sector occurred in 2015 when Bboxx and Oikocredit set up a $500,000 off-balance-sheet SPV to buy tranches of Bboxx’s receivables denominated in Kenyan shilling; with Okiocredit buying the USD notes issued by the SPV. While this facility did not scale, it set an important precedent. Large PAYG scale-ups like d.light, Sun King, M-Kopa, and Zola Electric, have all engaged in sizeable receivables financing arrangements over the past five years. In 2023, off-balance sheet financing accounted for 75% of the value of total debt commitments made to scale-ups across the sector. Some of the larger recent deals by d.light and Sun King and their significance to the wider sector are profiled below:

| Spotlight 1: d.lights Brighter Life Kenya (BLK) deals and Sun King’s securitisation deal d.light’s BLK1 and BLK2 receivables finance structures combined were worth over $250 million. Initially established in 2020 by African Frontier Capital (AFC), BLK1 is an off-balance sheet financing vehicle, which received debt commitments from the U.S. International Development Finance Corporation (DFC), and Norfund. BLK2 provides d.light with multi-currency financing over a two-year commitment period, and finances products including solar-home-systems, productive use appliances and smartphones. AFC and d.light just announced that BLK1 has successfully repaid its senior debt in full, and that BLK2 received the first ever worldwide formal credit rating for a securitisation structure in the PAYG solar sector. In 2023, Sun King secured a first-of-its-kind, bank-led and entirely Kenyan-Shilling-denominated $130 million sustainable securitisation transaction arranged by Citi and supported by several commercial banks and development finance institutions (DFIs) including ABSA Kenya, British International Investment (BII), FMO, Norfund, Standard Bank Kenya and the Trade and Development Bank. The commitment allows Sun King to access the capital needed to provide consumer financing to another 1 million customers. These deals represent major milestones for the off-grid solar industry, as they underline that PAYG portfolios with a consistent repayment record can be financed at scale through off-balance sheet securitisation, while providing investors with stable, and predictable returns. DFIs have played a major role in mainstreaming these financing arrangements and providing other funders with confidence to provide funding to this new asset class. |

The role of digital technology in enabling receivables financing

The principal contribution of digital technologies in receivables financing is the data they produce. PAYG systems rely on machine-to-machine communication, where devices remotely relay consumption data to a central server, predominantly via GSM. The wealth of repayment data from these business models has allowed for the creation of portfolio-level credit scores, facilitating the ease of sales to factors and subsequently liberating working capital.

For example, climate fintech Nithio run a risk analytics engine, which calculates the real value vs. the face value (contracted) of a ring-fenced receivables portfolio on a discounted basis by directly accessing the customer relationship management (CRM) systems of distributors. AI helps process this raw, anonymised customer repayment data, which is then combined with a rich database of geospatial, socioeconomic and climate data.

Asset tracking through IoT and app-based rider-driver matching platforms are emerging as other important technological enablers for receivables models tailored to mobility solutions.

Drawbacks and challenges associated with receivables financing

- Accessibility and fairness within sectors: It is well-documented that seven companies attract the bulk of funding in the off-grid solar sector, while local, nascent, and women-led distributors often struggle to access financing. When it comes to receivables financing, it largely remains accessible only to established organisations with significant scale, developed digital infrastructure, and access to sophisticated CRM platforms and risk-scoring methodologies.

- The transaction costs of deals require scale: The degree of complexity and number of financing and legal stakeholders involved in receivables financing arrangements lead to significant transaction costs that make small deals less attractive, creating barriers to entry for smaller distributors.

- Risk perceptions and limited awareness: Several potential private funders such as banks are still learning about PAYG models and are reluctant to fund the sector. A key enabler for addressing these issues is the participation from DFIs. DFC and BII were both instrumental in supporting d.Light and Sun King in their record-breaking securitisation deals. Guarantee mechanisms are particularly critical to support local currency financing by incentivising the involvement of local banks.

- Lack of data standardisation: Given the complexity of PAYG businesses across their respective inventory management and liability management value-chains (see Figure 2) and varying degrees of vertical integration across the industry, data across the PAYG ecosystem is often not standardised and can be challenging to compare across ventures and markets. Initiatives such as PAYGO Perform by GOGLA aim to encourage the industry to adopt a standardised and transparent set of key performance indicators.

An overarching risk is also intrinsic to the business environment and market context many PAYG businesses are operating in. Some businesses tend to be low-margin businesses with elevated customer default rates, whose portfolio risk can be impacted by a series of exogenous factors (macroeconomics, weather, sudden income shocks) that could impact the well-being of their customer base. An encouraging signal from d.light’s BLK1 facility has been that successful repayment occurred despite the facility running concurrently to a range of unexpected shocks affecting d.light and their customer base (COVID-19, locust, and currency fluctuations).

Looking forward

Aggregation of upstream capital devoted to receivables financing, as well as downstream aggregation of eligible projects, is poised to increase its accessibility and attractiveness to a wider set of players and sectors. Solaris Offgrid, for example, is developing the Bridgin receivables aggregation platform that integrates with all major PAYG management platforms. This enables increased automation of data collection, aggregation, and transaction processing, reducing transaction costs overall. Platforms leveraging application programming interfaces (APIs) with IoT-connected devices and predictive analytics could generate first-approximation credit scores to test the application of receivables finance in sectors where it is less common (for instance by building on existing credit scoring approaches by productive use asset financing ventures such as EnerGrow). Clean cooking, productive use assets like solar water pumps, agro-processing, or e-mobility assets could be securitised in such a way.

Access to well-priced working capital financing solutions require more companies to adopt CRM solutions. Reliable data and monitoring solutions are a core feature of this new wave of receivables financing across climate tech ventures. CRM providers offering solutions for smaller, early-stage companies will allow a larger number of providers and use cases to benefit. Other not-for-profit initiatives such as the Green Genset Facility by the Access to Energy Institute provides technical assistance and digital loan portfolio management tools to smaller distributors.

The work of Nithio and others highlights the value of leveraging satellite and geo-spatial data to inform credit risk analysis in a consumer portfolio. This is especially relevant for unlocking financing among customers that are employed in agriculture, where fulfilling equipment needs along appropriate repayment cycles can result in appreciable improvements in yields and social impacts.

Lastly, deploying receivables financing alongside other financing instruments such as results-based financing or carbon credits that are leveraging similar data systems and verification technologies could generate further impact and catalyse vital collaboration between funders across the impact-to-commercial spectrum.

No single financing instrument is a silver bullet solution to address the financing challenges of climate tech ventures in LMICs. Receivables financing has emerged as an important instrument in the PAYG solar sector and will also be an important tool for other climate-tech ventures relying on hardware and consumer financing. Key challenges going forward are enabling more early-stage ventures to access receivables financing, involving more funders such as commercial banks, and supporting companies in finding the right balance between different forms of funding for their business.

Watch the video replay of our webinar hosted on 29 May 2024, which features a number of funders and start-ups actively involved in receivables financing.