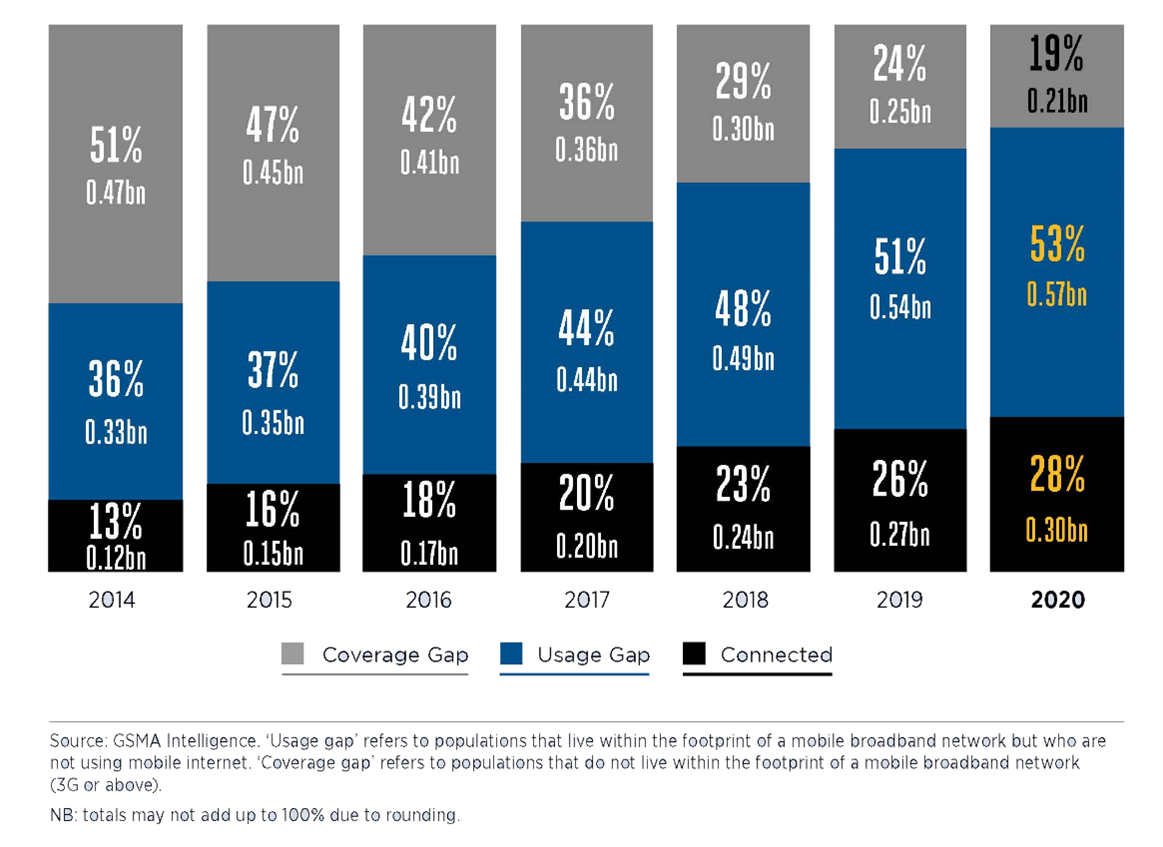

The COVID-19 pandemic has accelerated the digitisation of economies and societies around the world. Mobile internet adoption continued to increase in 2020, despite the economic recession. By the end of 2020, 28% of the Sub-Saharan African population was connected the internet, continuing the positive trend seen since 2014. Mobile broadband coverage has also increased substantially in Sub-Saharan Africa, but it is still the region with the largest coverage gap; one in five people live in an area without mobile broadband coverage – an estimated 210 million people. More concerning though, is the usage gap, which is widening year after year and now stands at 53%. In other words, across the region, more than half of the population is still not using mobile internet, despite living in an area with mobile broadband coverage.

Evolution of mobile connectivity in Sub-Saharan Africa

Why is this so? Even though mobile internet adoption continues to increase, it does so at a much slower pace than coverage expansion. In many countries we observe this lag between creating an enabling environment for mobile internet and seeing a significant increase in adoption.

GSMA’s research has also found that owing a smartphone is one important enabler for becoming a regular mobile internet user. In Sub-Saharan Africa, while smartphone penetration continues, they still account for less than half of total connections. The mix of mobile connections in the region is quite unique: it has the highest percentage of basic or feature phone connections, and most smartphones only support 3G, despite increases in 4G coverage. However, it is worth noting that in 2020 only half the population in Sub-Saharan Africa had access to a 4G network.

The State of Mobile Internet Connectivity 2021 highlights that a lack of user demand limits operator’s investments in mobile broadband coverage. Shifting the focus from infrastructure only to a more people-centered approach to connectivity could help close the coverage gap and drive-up demand. This includes having a better understanding of the barriers that prevent people from using mobile internet. In Sub-Saharan Africa, as in other regions, affordability of handsets and data, and a lack of literacy and digital skills are the most cited barriers to mobile internet adoption and use.[1]

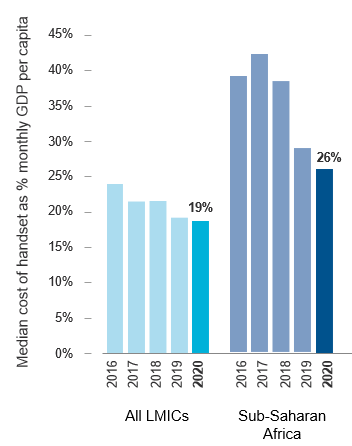

Affordability of an internet-enabled handset has improved in Sub-Saharan Africa, driven mainly by wider availability of cheaper smartphones and smart-feature phones. While the latter do not share the full capabilities of a smartphone, they do allow for installation of a range of applications and provide a faster and better browsing experience than traditional feature phones.[2] Smart-feature phones were introduced in many markets in 2020, reducing the price of the cheapest entry-level internet-enabled handset from $36 USD in 2019 to $28 USD in 2020. However, Sub-Saharan Africa still has the least affordable handsets of any region. Across low- and middle-income countries, the median cost of the cheapest internet-enabled handset as a percentage of monthly GDP is 19% compared to 26.5% in Sub-Saharan Africa.

Literacy and digital skills remains a key barrier to mobile internet adoption and use. In Kenya, Mozambique and Nigeria, more than half of those who are not using mobile internet, despite being aware of it, report barriers related to literacy and digital skills. This barrier disproportionately affects people living in rural areas and women. Difficulties with reading and writing were most commonly reported as a sub-barrier, particularly in Nigeria.

To close the usage gap, it is important to address the barriers to digital inclusion in a more holistic way. Yes, handsets need to be more affordable for consumers in Sub-Saharan Africa and to be available for purchase in rural areas, but unless data also becomes more affordable, people may not be able to take advantage of all that mobile internet has to offer. In Sub-Saharan Africa, the median cost of 1 GB of data is 15.3% of monthly GDP per capita for the poorest income quintile, well above the Broadband Commission target of 2%.[3] In addition, the internet needs to be relevant for users to be able to easily navigate, consume and create content to meet their needs. Furthermore, users need to feel safe going online, with the knowledge and skills to recognise and mitigate any threats or scams.

Click here to download The State of Mobile Internet Connectivity 2021 and related resources, including a Sub-Saharan Africa Key Trends factsheet.

[1] Based on the results of the GSMA Consumer Survey 2020. This question is asked to mobile users those who are aware of mobile internet but haven’t used it in the last 3 months.

[2] For further details, see spotlight in GSMA, State of Mobile Internet Connectivity Report 2020

[3] The UN Broadband Commission has set a target to make entry-level data services less than 2% of monthly income per capita by 2025. See 2025 Targets: Connecting the Other Half, Broadband Commission, 2018.

This initiative is funded by UK aid from the UK government and by aid from the Swedish International Development Cooperation Agency (SIDA), and is supported by the GSMA and its members. The views expressed do not necessarily reflect the UK or Swedish governments’ official policies.