What do we mean by Interoperability?

There are many different types of interoperability. In addition to transaction interoperability (the ability to transfer money between accounts from one service provider to another), it may also include retail point of sale compatibility (so that a customer can use a POS regardless of his payment provider) and encompass agents as well (so that a customer can cash-in & cash-out at any agent, which is already functionally possible and largely common because of agent sharing).

This blog post focuses primarily on A2A interoperability in Pakistan i.e. the ability to transfer money from one branchless banking [1] (BB) account to another in a different scheme, or between a BB account and a regular (i.e. commercial) bank account [2].

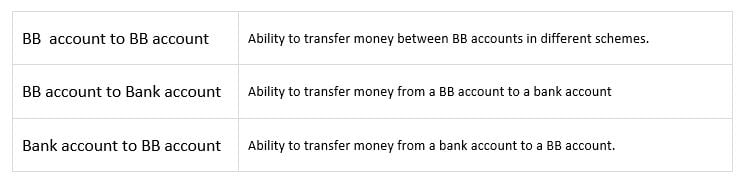

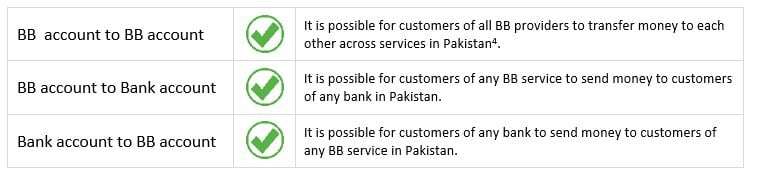

Various ‘layers’ of interoperability are possible under A2A interoperability, as shown below:

Layers of A2A Interoperability Live in Pakistan today

In Pakistan, A2A interoperability has been live since March 2014 and is enabled through a commercial inter-bank switch, called 1Link [3].

Specific layers of A2A interoperability that are currently available in Pakistan are:

As such, 13.2m BB customers [4] in Pakistan today can transact with each other across different networks. Moreover, they can also transact with all other banks in Pakistan.

The impact of A2A interoperability in Pakistan

Since early 2014, BB services and customers have enjoyed full A2A interoperability in Pakistan – but what has been the impact of this on transactions?

The graph below illustrates the increase in off-network transactions in Pakistan since the launch of A2A interoperability in the market until September 2015 (the latest data available from the State Bank of Pakistan’s Quarterly Branchless Banking Newsletter).

Source: State Bank of Pakistan Quarterly Branchless Banking Newsletter

According to the State Bank of Pakistan, the value of Inter Bank Funds Transfer (IBFT) more than tripled from PKR 2.4b to PKR 7.8b [5] between October 2014 and September 2015 [6]. Moreover, based on transaction data received from Easypaisa, UPaisa and Mobicash, we can estimate that of the total value of off-network transactions recorded by them, up to 2% is accounted for by off-network transactions between these players alone [7]. While this percentage may appear small, it is significant in that it shows that customers of BB services such as Easypaisa, UPaisa and Mobicash are increasingly using A2A interoperability to transact with each other, and not just with commercial banks.

It is worth pointing out that these numbers on interoperability have been achieved so far without any strong BTL or ATL marketing support to highlight interoperability to customers.

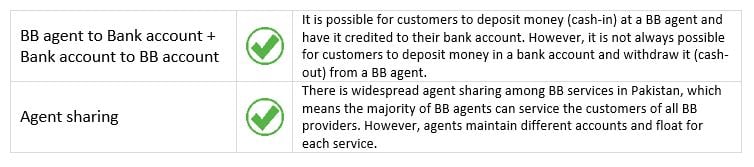

Agent Interoperability also prevalent

In addition to full A2A interoperability, it is also interesting to note that there exists a very high level of agent interoperability as well in Pakistan. This is captured in the table below:

Of the total number of BB agents in Pakistan today [8], the majority are shared and are able to perform cash-in / cash-out transactions for customers of all BB services. In addition, bank account holders across the country can take advantage of this vast network of agents to deposit funds into their accounts without having to visit a physical bank branch.

One of the most interoperable markets in the world

Based on these facts, Pakistan is definitely one of the most interoperable mobile money markets in the world today. A fully A2A interoperable market, and a good level of agent interoperability at the customer level, allows both customers and service providers to benefit.

Building upon this strong collaborative start, mobile operators are now beginning to turn their attention towards merchant payments, and the wider mobile financial ecosystem, and are looking at how they can adopt a collaborative approach there too. We will continue to watch this market and share updates as progress is made.

Notes

[1] Mobile money is referred to as branchless banking in Pakistan’s bank-led model context.

[2] See more details on A2A interoperability here: https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/mobile-money/

[3] See our case study explaining details of interoperability in Pakistan here: https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/wp-content/uploads/2016/01/2015_GSMA_Choosing-a-technical-model-for-A2A-interoperability_Lessons-from-Tanzania-and-Pakistan.pdf

[4] SBP Quarterly Branchless Banking Newsletter, July-Sep 2015

[5] These figures (taken from the SBP Quarterly BB newsletter) include the following off-us A2A transactions: BB account to BB account; BB account to Bank account; and Bank account to BB account. They do not include IBFT transactions between commercial banks.

[6] See more details on IBFT in our previous blog here: https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/a2a-interoperability-what-is-happening-between-banks-and-mobile-money-providers

[7] Based on data received from mobile operators spanning April 2014 until January 2016. Percentage arrived by dividing total value of off-us (sending) transactions registered by mobile operators, by the value of off-us (sending) transactions between just the BB services provided by the mobile operators i.e. Easypaisa, UPaisa and Mobicash.

[8] The SBP Quarterly Branchless Banking Newsletter, July-Sep 2015 lists the number of BB agents in Pakistan as approximately 268,000.