During a cash-in transaction, mobile money agents typically receive cash from the customer and deposit the amount into the latter’s mobile money account. To transfer money to someone else, the customer would then have to carry out a peer-to-peer (P2P) transfer from their mobile money account. However, across several markets in Sub-Saharan Africa, some customers have been using remote cash-ins to change this particular flow of money.

What is a remote cash-in?

Remote cash-ins refer to cash-in transactions at an agent where the customer receiving the funds in their mobile money account is not present during the transaction. This typically happens when customers are looking to bypass the need to cash in first before sending money to someone as a peer-to-peer (P2P) transfer. By opting for a remote cash-in, mobile money customers would need only one transaction to be performed and avoid fees that some providers charge on P2P transfers.

There are several reasons why customers opt for remote cash-ins: reducing two transactions to one offers ease and convenience. Sometimes, this may be because customers may genuinely not have a mobile money account. In other cases, if they have an account, some customers may not yet be comfortable using it. Yet, they still need to transfer money. In some markets, the behaviour is customer-led; in others, agents may encourage this to earn additional revenue.

Typically, remote cash-ins can occur when both customers and agents are looking for lower costs. For example, when there is a big difference in fees for P2P transfers and cash-in transactions, a remote cash-in may seem attractive to the customer. In other scenarios, agents may charge less than the P2P fee for a remote cash-in, incentivising customer behaviour towards remote cash-ins and offering some agents an additional revenue source.

Which countries are affected by remote cash-ins?

Remote cash-ins have been an industry concern for a few years. The GSMA spoke to Airtel Money, Axian Fintech, Orange Money and Safaricom M-Pesa to understand more about remote cash-ins and whether some markets are more prone to others. These providers are affected by remote cash-ins across different markets in Sub-Saharan Africa. Within many of these markets, remote cash-ins often occur nationwide.

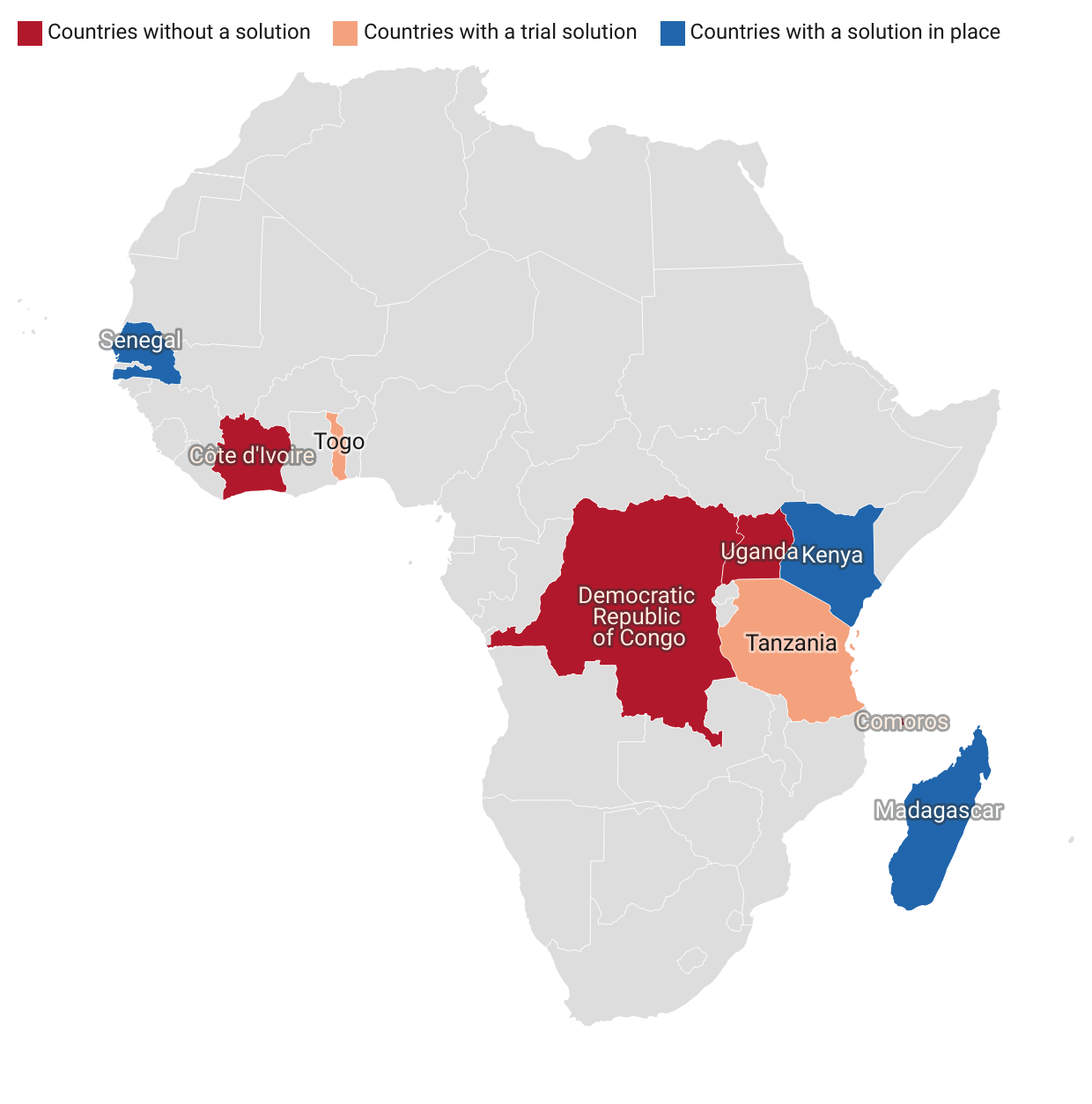

Mobile money providers in some of these countries have either implemented a successful solution to overcome remote cash-ins or have trialled a solution (Figure 1). For instance, in Kenya, M-Pesa identified remote cash-ins as a significant concern early on. In 2017, M-Pesa launched a vicinity-check solution where a customer cashing in needs to be in the same cell as the agent. The transaction fails if the customer cashing is located elsewhere.

Figure 1: Selected countries in Sub-Saharan Africa affected by remote cash-ins

Axian Fintech has launched an alternative solution where agents are deterred from proceeding with a remote cash-in. This involves agents receiving a warning message that they may be charged the P2P fee when attempting to cash in for an absent customer. Agents having to bear this fee is designed to encourage customers to open an account and actively use mobile money. This solution is currently live in Madagascar and Senegal.

One possible downside is that the customer may be willing to cover this cost, especially if the agent is being charged the same fee as a customer P2P transfer. An alternative approach recently trialled in Madagascar aimed to overcome this issue by prompting customers to use their mobile money accounts. The remote cash-in fee was raised to the same rate as the cash-out fee, making it higher than the P2P transfer fee. A few months later, the volume and value of P2P transfers had suddenly risen significantly.

What impact have remote cash-ins had on the industry?

For mobile money providers, remote cash-ins can restrict mobile money adoption and use. Agents are important in digitalising customer funds. However, their role in enabling remote cash-ins has affected P2P transfers in some markets and cannibalised providers’ P2P revenue. List revenue can vary from around $200,00o per month in a market to around $20 million annually for a mobile money group with several services. While customers are likely to appreciate the savings made by using this alternative transfer service, remote cash-ins can affect agents and their income. In some cases, providers – such as Airtel – have sought to claw back agent commissions on remote cash-ins to discourage their use. By not verifying the depositing customer’s ID, agents may also create a major regulatory compliance issue regarding know-your-customer (or KYC) for providers.

How should the mobile money industry approach remote cash-ins?

Many mobile money providers agree that resolving remote cash-ins is best done as an industry-wide action – rather than attempting a unilateral fix. Customer or agent behaviour can affect the entire industry as opposed to a single provider. For any industry initiative to succeed, regulatory engagement can help to raise mobile money providers’ concerns as a collective. However, most providers have sought to resolve a problem once identified as the first course of action.

To learn more about the important role that mobile money agents play, click here.