This blog post was co-written by Francesco Pasti and Nicolas Vonthron.

Banks and mobile money providers are now working closer together than ever before, and the connectivity between them is key for the industry to continue to grow. Over a two-part blog series, we will review the existing landscape of and trends in transactions between bank accounts and mobile money accounts.

Last year, the GSMA Mobile Money Programme began to focus on Account-to-Account (A2A) interoperability, meaning interoperability between mobile money accounts from different providers and between mobile money accounts and bank accounts. Indeed, when mobile money providers embrace A2A interoperability, it is not only about P2P transfers, but also about offering Bank Account to Mobile Money Account (B2M) and Mobile Money Account to Bank Account capabilities (M2B) to their customers.

Mobile money interoperability is live in five markets in the world: Indonesia, Pakistan, Tanzania, Sri-Lanka and Thailand.[1] Globally today, we estimate that at least 45% of mobile money deployments are connected to banks and are offering B2M and M2B capabilities. [2] The number of banks connected to mobile money schemes increased by 66% between 2013 and 2015, growing to more than 520 banks in 2015 (for 120 deployments).[3] However, this doesn’t mean that these providers are connected to every bank in their market.

So, in this scope, how are these B2M and M2B transactions impacting the mobile money ecosystem? Why is mobile money and bank interoperability relevant, and actually strategic, for mobile money providers? How can it be achieved, and what long-term questions are raised?

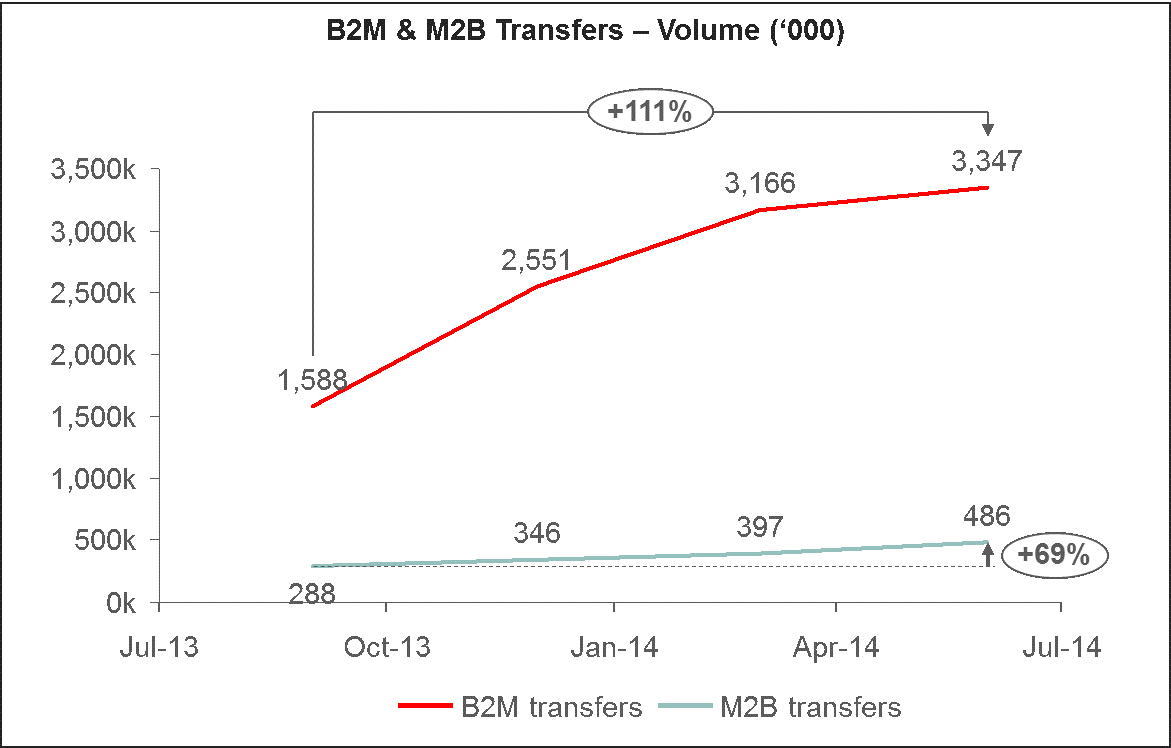

Although money is flowing both ways, to and from the banking system, the mobile money system is a net receiver

Between September 2013 and June 2014, the total number of B2M transactions increased by 111% (going from 1.6 million to over 3.3 million transactions per month), while the total of M2B transactions increased by 69%.[4]

In 2014, the volume flows to and from bank accounts saw some of the strongest growth of all products in the mobile money ecosystem (+175%), and was the second-fastest growing product after international remittances.

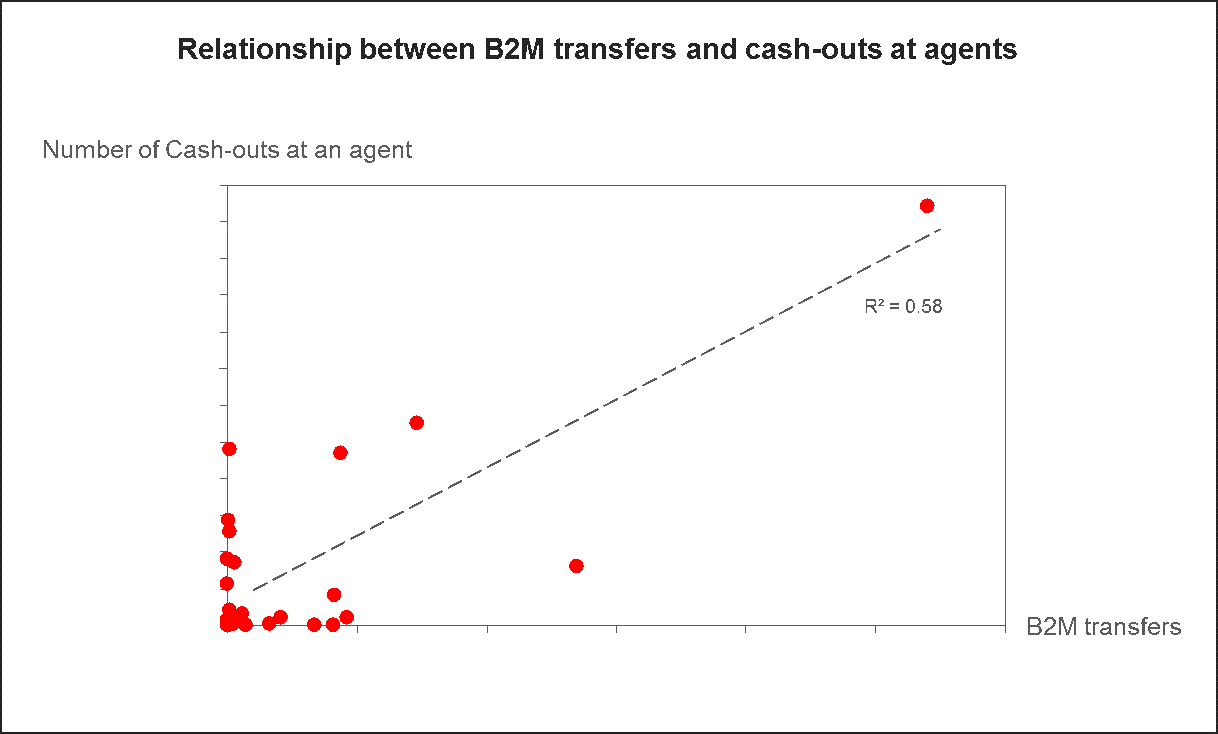

Mobile money is not only for the unbanked – banked customers are also using agents to cash-out

When analysing the correlations (R²)[5] between downstream ecosystem transactions (such as bill payments, merchant payments, etc.) and B2M volumes, it appears that banked customers transferring money from bank accounts to mobile money accounts are using it mostly for cashing-out at agents (R²=0.58), as well as for P2P transfers (R²=0.27).[6]

This indicates that customers are actually transferring money from bank accounts to mobile money accounts in order to proceed to a cash-out, and thus we can assume:

- That mobile money is performing an important and valued role in allowing banked mobile money customers access to their funds, and;

- That banked mobile money customers are also sending money via P2P transfers to mobile money customers, previously unbanked, closing the gap between these two worlds.

These findings raise questions around how commercial agreements between banks and mobile money providers should reflect the additional patronage on agent networks, particularly with potential liquidity pressure (perhaps similar to the ATM interoperability mechanisms, where usually a “sending party” pays).

This is the first of two blog posts analysing bank to mobile money integrations. The next post will review the flows of money and technical solutions that are supporting these increased number of integrations.

Notes:

[1] These markets are offering interoperability between mobile money accounts from different providers. Thailand live as of 1 December: http://www.bangkokpost.com/print/768428/

[2] 2014 GSMA Global Adoption Survey

[3] 2015 GSMA Global Adoption Survey

[4] 2014 GSMA Global Adoption Survey

[5] The coefficient of determination R² is a measure of dependence among random variables that indicates how close these are to a regression line. The coefficient goes from 0 to 1, with 1 indicating that the regression line perfectly fits the data and 0 meaning that all variables are random

[6] For a reference, the R² between P2P transfers and cash-outs is 0.85.