In low- and middle-income countries (LMICs), mobile money has unlocked access to financial services for hundreds of millions of people. According to the latest Global Findex 2025 data, 18% of adults in LMICs held a mobile money account in 2024, up from only 3% a decade earlier. For those without a bank account, mobile money can offer a more accessible, convenient and cost-effective path to financial services. This is especially true for women, whose access to formal financial services is often blocked by restrictive social norms, unpaid care responsibilities and lower earnings or education levels.

However, not everyone is benefitting equally from the rise in mobile money account ownership. GSMA analysis of the latest Findex data found that the gender gap in mobile money account ownership has actually widened since 2021.[1] In 2024, women in LMICs were 36% less likely than men to own a mobile money account, compared to 30% in 2021. This is mainly due to men opening mobile money accounts at a faster rate than women.

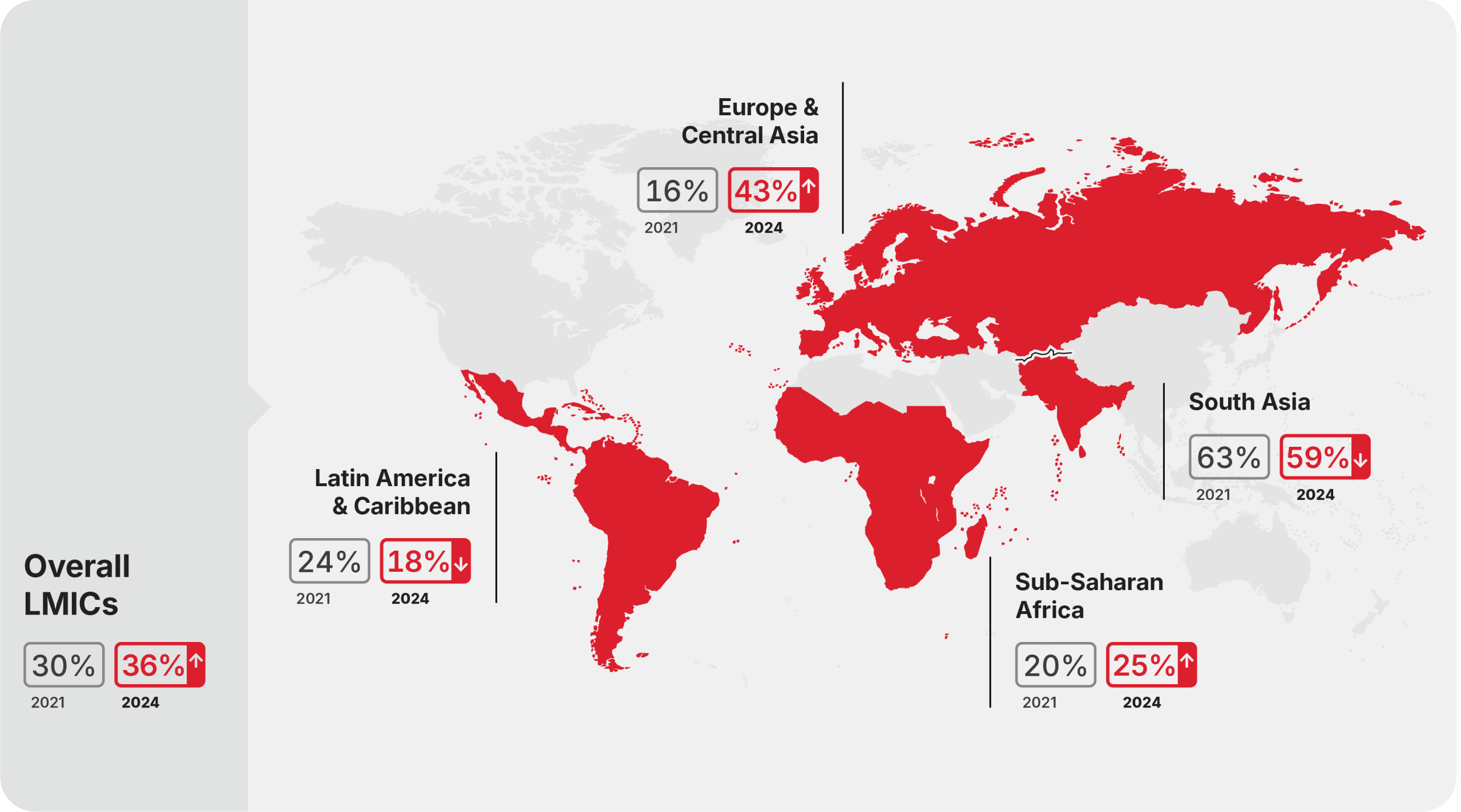

Although the overall gender gap in mobile money account ownership has increased, there is significant variation between regions and countries. Just two regions saw the gender gap narrow – South Asia and Latin America – while it widened in Sub-Saharan Africa, Europe and Central Asia (Figure 1). In South Asia, the gender gap has steadily narrowed, from 75% in 2017 to 63% in 2021 and now 59% – a notable trend in the region with the largest gender gap.

Figure 1: Gender gaps in mobile money account ownership across LMICs[2]

Source: Global Findex 2025

Sub-Saharan Africa remains the global leader in mobile money account ownership. In 2024, 40% of adults in the region owned a mobile money account – 13 percentage points higher than in 2021. Although lower than most regions, the gender gap in mobile money account ownership stands stubbornly at 25% – five percentage points higher than in 2021.

There is significant variation within the region, however. Of the 29 Sub-Saharan markets surveyed in 2024, the gender gap narrowed in roughly two-thirds and widened in 10. In Togo, the gender gap almost doubled from 23% in 2021 to 43% in 2024, as more men opened mobile money accounts than women. Conversely, in Senegal, it shrunk from 27% to 12% over the same period, and in Côte d’Ivoire it declined by 26 percentage points. Progress in these two countries is driven by rising adoption of mobile money among women, which has also contributed to a reduction in the overall financial account ownership gender gaps, demonstrating mobile money’s role as a strong equaliser.

It is encouraging that, despite a widening gender gap in mobile money account ownership in LMICs since 2011, this gap is instead narrowing in some countries and regions. However, the underlying penetration of mobile money also needs to be considered, as it may reflect limited financial inclusion overall. In Mozambique, for example, the gender gap in mobile money account ownership has fallen by 12 percentage points since 2021. Yet, with overall mobile money account ownership at just 46%, a large share of both women and men still lack access to mobile money services.

Several barriers prevent women from owning a mobile money account

To close the gender gap in mobile money account ownership, it is vital to understand the barriers preventing women from owning and frequently using a mobile money account. The GSMA State of the Industry Report on Mobile Money 2025 identifies several of these barriers, including a lack of perceived relevance or awareness of mobile money services, limited knowledge and digital skills, safety and security concerns, lack of access to a mobile phone and restrictive social norms, such as family disapproval. While both men and women can experience these barriers, more women than men remain financially excluded and would benefit disproportionately from efforts to tackle these barriers. from efforts to tackle these barriers.

Owning a mobile phone is a prerequisite for owning a mobile money account. Without a phone, women cannot register, verify their identity, receive payments or build a transaction history. Across LMICs, women are 8% less likely than men to own a mobile phone. This translates into 400 million women who do not yet own a mobile phone, many of whom are from rural and lower-income households (GSMA, 2025). For women to reap the full benefits of mobile money, reducing the gender gap in mobile phone ownership, is an important step.[3]

Progress has stalled – what now?

The latest Global Findex data shows that progress in closing the mobile money gender gap has stalled. Urgent, targeted action is needed to better understand and address this stubborn gender gap. This includes increasing awareness of the relevance and benefits of mobile money for women and among any gatekeepers, as well as designing services to meet women’s needs, as well as men’s. Improving digital skills and tackling the gender gap in mobile ownership is also essential – for instance through incentivising agents to upskill women customers and expanding access to affordable devices. Bridging the gap also has considerable social and commercial benefits and is vital to achieving the United Nations Sustainable Development Goals (SDGs)[4], especially those related to gender equality and financial inclusion.

[1] 2021 global and regional averages differ slightly from figures originally published in our 2021 blog. This is because the Global Findex 2025 dataset includes data from 22 new countries in 2022, which could not be surveyed in time for the release of the Global Findex 2021 due to COVID-19 mobility restrictions.

[2] Data from East Asia and the Pacific and Middle East and North Africa is excluded from Figure 1 in line with Global Findex 2025, where data on demographic groups is only available for regions and countries where overall mobile money ownership is below 10%.

[3] A list of recommendations for stakeholders to close the mobile phone ownership gender gap in LMICs can be found in The Mobile Gender Gap Report 2025.

[4] GSMA. (2023). Making progress on the SDGs with mobile money.

The Connected Women programme is funded by the UK Foreign, Commonwealth & Development Office (FCDO), the Swedish International Development Cooperation Agency (SIDA), and supported by the GSMA and its members.