Over-indebtedness is a concern for many people, but the rise of digital credit may have amplified the issue. While there is no global consensus on its definition, it refers to holding a relatively large and unsustainable amount of debt. This blog highlights key findings and recommendations from a 2024 GSMA report that investigates the relationship between digital microcredit and consumers’ financial health.

Microcredit use trends in emerging markets

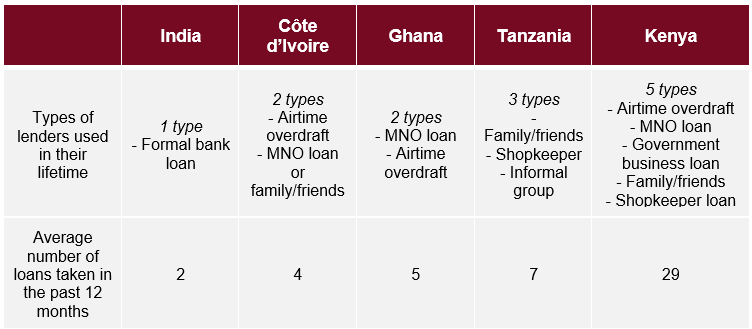

Through phone surveys, the report studied borrowing behaviours in five markets: Côte d’Ivoire, Ghana, India, Kenya and Tanzania. Borrowing varies significantly across the five countries (Figure 1), from infrequent and focussed in India (borrowing twice a year from one provider) to frequent and diverse in Kenya (borrowing more than two times a month from multiple providers).

Borrowers in India primarily use banks due to the prevalence of the Unified Payment Interface (UPI) – a real-time, bank-to-bank transfer system. In Kenya, digital loan providers dominate the market. In all five countries, personal networks (e.g., friends and family) are among the top five sources of credit.

Despite these differences, all users prefer easy applications, fast disbursements and low interest rates when choosing a credit provider. The two most common reasons for borrowing in East and West Africa are to cover day-to-day expenses and invest in a business. In India, borrowers often use loans for one-off social or emergency expenses.

Figure 1: Behavioural profile of an average borrower, by country

Source: GeoPoll. Note: MNO refers to mobile network operator.

More than half of borrowers in Africa and 38% of borrowers in India struggle with loan repayments. The main causes include increased costs of living and loss of income. Loan repayments can consume large portions of a household’s monthly income – ranging from 15% in India to 34% in Kenya and Ghana. Borrowers with outstanding loans are more likely to report mental health issues, such as anxiety or stress, compared to borrowers who repay on time.

Over-indebtedness and digital credit products

Ghana and Kenya have the largest proportions of borrowers who have taken a digital loan (through a mobile app or MNO), at 80% and 54%, respectively. Tanzania is third with 32%, followed by Côte d’Ivoire (30%) and India (2%).

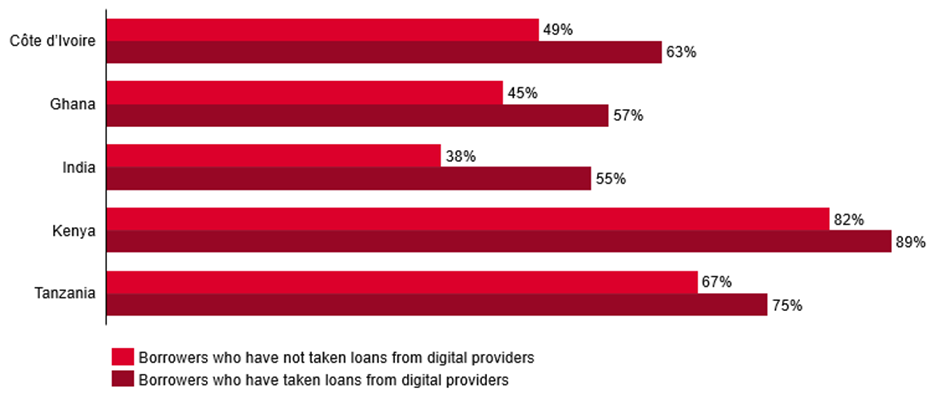

The survey found links between access to digital credit and financial delinquency. In all five markets, borrowers with digital loans are more likely than those without digital loans to report credit arrears (Figure 2). Abusive lending practices associated with digital credit may contribute to chronic over-indebtedness. These often target vulnerable communities and include excessive pricing, price shrouding, debt stress, abusive enforcement and “push marketing”. These practices are particularly common in East Africa.

Figure 2: Proportion of borrowers who have loans with late, partial or missed payments or are in default, by experience with digital providers and by country

Source: GeoPoll

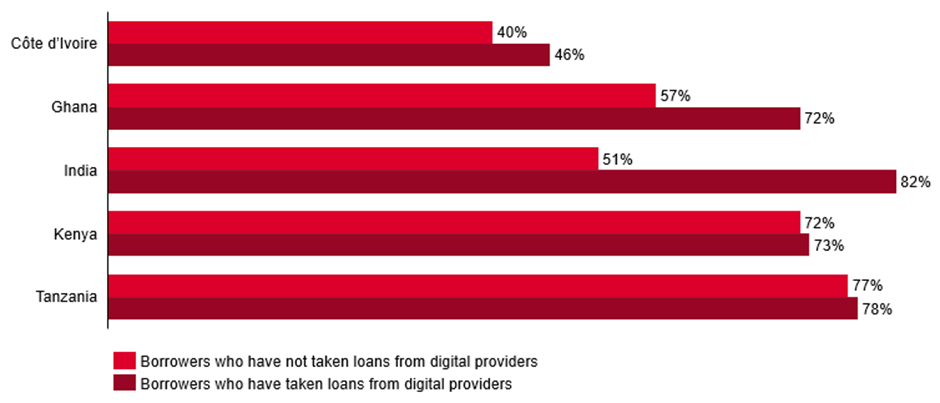

Digital borrowers exhibit positive traits too. They are more likely to self-assess as financially healthy (except for Tanzania) and report formal or informal savings (Figure 3). In Kenya and India, digital borrowers are less likely to use savings to repay a loan. At least two-thirds of digital credit holders across all markets believe that digital loans helped them meet short-term needs.

Figure 3: Proportion of borrowers who report having formal and/or informal savings, by experience with digital providers and by country

Source: GeoPoll

Provider perspectives and expert opinions on over-indebtedness

All mobile money providers (MMPs) surveyed had a separate unit or partnered with licensed digital microcredit providers. This model offers advantages but may limit MMPs from developing in-house expertise in digital markets. While MMPs report relatively low default rates, they have taken initiatives to minimise them. These include artificial intelligence (AI)-driven credit-scoring algorithms, compelling behavioural nudges and tailored instalment schemes to help delinquent customers repay loans.

The research identified three groups of consumers currently benefitting from digital credit: “pay cheque loan” borrowers who treat digital loans as a financial bridge, consumers taking buy-now-pay-later (BNPL) loans and informal microenterprises that borrow to fund their daily operations. The last two groups remain underserved and could benefit from credit products that are better tailored to them.

While the report presented several recommendations on how to improve the financial health of borrowers, two important ones concern the relationship between regulation and innovation, and digital literacy:

Recommendations to manage over-indebtedness

Regulatory gaps across the surveyed countries may be stifling innovation, supporting a potentially biased view of credit providers and stigmatising delinquent borrowers. Credit providers and policymakers should collaborate to create a regulatory environment that encourages information sharing with credit reference bureaus, consumer protection agencies and other industry stakeholders. Better digital infrastructure would support faster and more secure data transfers.

Many vulnerable consumers of microcredit suffer from low general, financial and digital literacy levels. Compulsory financial education, national IDs and cheap smartphones could reduce vulnerable households’ susceptibility to over-indebtedness. This approach has already been effective in India and Ghana.

Learn more about the relationship between digital microcredit and the financial health of consumers here.