This blog is based on research by Analysys Mason.

The innovative and effective use of mobile money provider (MMP) data is able to support operational efficiencies and customer outreach – but it is also able to drive new and enhanced products and services, both for consumers and businesses using mobile money platforms. MMPs have shown progress in areas such as access to credit, but there is scope to improve access to financial and non-financial products and services by identifying underserved consumers, personalizing services, and building trusted profiles. Some MNO-led MMPs may be well positioned to combine telecommunications data with payments data, where they have begun digital transformations, that include shifting to big data analytics platforms that enable the production of faster and real-time insights at a lower cost.

MMPs motivated to seek out these opportunities, can look to other industries to understand the diversity of potential applications. The use of data is best informed by an industry or consumer need or pain point, so we spent some time trying to uncover potential uses for mobile money data, along with some of the key considerations for MMPs thinking of adopting them. Here are three areas in which mobile money data assets may be harnessed to meet consumer and market needs:

Improving the e-commerce experience

Strong growth in mobile-based e-commerce (m-commerce) in emerging markets is driving demand for greater marketing services. In SSA, from 2017-2022 m-commerce transaction revenue is projected to increase to 13% while digital advertising revenue is expected to experience 40% CAGR (Digital Services Worldwide). While online advertising as we know it faces challenges in Africa, opportunities to for personalised marketing and promotions continue to evolve and grow. MMPs can offer consumer insights to e-commerce merchants that accept mobile money payments by developing customer profiles, and even leverage telecom data where accessible. These services can provide significant value to e-commerce merchants and decrease churn.

MMPs can learn from SK Telecom’s ‘Syrup’ which has created an integrated offering of payments and loyalty schemes, leveraging SK Telecom’s Smart Wallet data and a large network of partnering e-commerce and physical merchants to offer curated benefits and targeted information to individual consumers. MMPs will need to grow their acceptance network of e-commerce merchants and transactions to provide a suitable marketing value proposition.

Tackling payments fraud

As e-commerce and digital payments take-off, small merchants that use mobile money for online or physical transactions would benefit from protection against fraudulent transactions. Globally, card fraud has grown 14% (CAGR) since 2012 – an ominous statistic for mobile money, the new kid on the block.

MMPs can enhance their offering to e-commerce and physical retailers with payment fraud prevention services that leverage mobile money data to develop or enhance risk assessment engines. The use of transaction data to prevent fraud in other industries is established.

One sign of a growing demand are recent moves by payments providers PayPal and Stripe to couple fraud analytics with their payment offering to online merchants. MMPs can also learn from Chime, a mobile bank, as one example of how they partnered with specialized fraud analytics vendor Simility to reduce fraud by analyzing transaction data and device fingerprints in real-time. Chime reports reducing fraud by 70% and the number of chargebacks from customers. Critically, MM providers considering offering fraud prevention services will need to forge partnerships or make significant investments in systems with machine learning capabilities, to varying degrees depending on whether they intend to monitor, defend, or detect fraud.

Expanding access to consumer credit

Findex 2018 indicates that globally 22.5% of the adult population reports borrowing from a formal financial institution or using a credit card in the last year. However, across low-income countries that figure is only 7.9%, with 31.3% report borrowing from family and friends (as compared to the global figure of 22.5%). This reliance on informal borrowing is one sign that there is a gap in formal sources of credit in low-income countries. The uptake of mobile money and the subsequent creation of transaction data has spurred access to credit to individuals who, previously lacking a credit history, were excluded from borrowing from formal sources. MMPs have made significant strides in this space, often building on MNO experience leveraging customer’s usage and top-up data to extend emergency airtime loans. The growth in mobile money transaction data has further increased the size of the opportunity with pioneering services such as Safaricom M-Shwari in partnership with Commercial Bank of Africa, Airtel Tanzania’s partnership with Jumo, and GCash’s synergies with Fuse lending, amongst many others.

Building on this concept and success, MMPs can consider their ability to develop consumer insights or scores that can help identify good, credit worthy or reliable customers for partners looking to provide new services – both financial and non-financial – to mobile money users. This has been the strategy for Alibaba’s Sesame Credit, has allowed consumers to opt-in and create a score based on their Alipay transaction data which provides access to services such as bikes share deposit waivers for shared bikes and powerbanks and access to online travel agencies. As the sharing economy grows and access to new services depends on trust – mobile money data can support building this bridge. MMPs will need to prove the robustness of their score by carefully considering the needs of the end user and business that would benefit from the score.

How will mobile money providers shape these opportunities?

In order to unlock these opportunities for consumers and businesses, mobile money providers will need to carefully consider their unique strengths and context to determine the business model and role they are able to play in the delivery of these products and services.

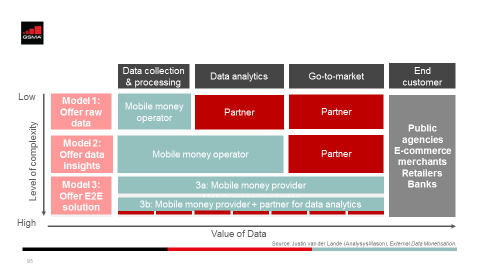

Providers can consider 3-4 key business models. In the first, providers that are willing to harness data may not have the direct channels to the end customer and may prefer to partner with established channels to deliver the service. In the second, MMPs have the opportunity to add greater value when data scientists are employed to gather business insights that are tailored to an industry or sector. The third model is where MMPs are able to create or leverage their direct customer engagement capabilities to market their data-based products and services, without relying on a partner to ‘go-to-market’. Providers will need to make the critical decision about which variation of the business model they choose based on the application at hand and their business context and capabilities.

However, what remains critical for all mobile money providers across these business models, is a primary role in data collection and thus a critical commitment to maintaining safeguards to uphold consumer trust when analyzing, using, and sharing consumer data. The mobile money industry has begun to address this through the GSMA Mobile Money Certification, but will continue to raise the bar and balance innovation with consumer trust as new applications evolve.