Over the past decade the cost of sending remittances has significantly declined. According to the latest data released by the World Bank, the average cost of sending a typical $200 remittance has declined from 9.1% in 2013 to 6.4% in Q4 2023. While these current costs are still more than twice the SDG 10.c target of 3%, a reduction of 30% in costs since 2013 is worth celebrating.

The advent of digital remittances

Most of the decline in costs over this time has come with the advent of digital services. Not only has there been an increase in the number of digital remittance services in that time, their cost has also significantly decreased to an average of 4% in 2023, contributing to the global reduction in costs. Within this classification of digital remittances lies mobile money.

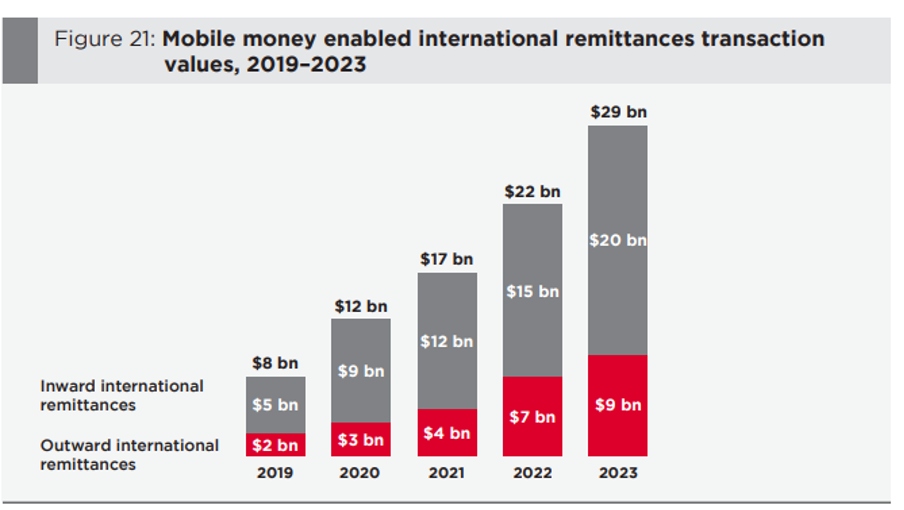

According to the most recent State Of The Industry Report, international remittances are now one of the fastest growing use cases of mobile money. Here, there are opportunities of cost, speed and convenience for remittances whether mobile money is involved on the send leg, receive leg or both. Mobile money enabled international remittances continue to show strong growth with transaction values totalling $29 billion in 2023.

Current research being conducted by IOM with Kenyan diaspora in the UK shows that overwhelmingly, they prefer to use cheaper digital remittance services that payout into a mobile wallet (M-Pesa in the majority of cases) rather than more expensive cash-based services. With many of the newer generation digital providers competing aggressively on price, migrants on the UK Kenya corridor typically pay less than the SDG 10.c target of 3% and less than the official published figure of 4.8% (which is an average across all service provides, both cash and digital).

The opportunity for mobile money IMT

The opportunity for digital and mobile remittances is not limited to developed-developing country corridors. Within Africa for instance, the majority of migration remains within the continent. We see a similar picture for remittances, with some 37% of remittances to sub-Saharan African countries being sourced from within the continent. Yet Africa remains the most expensive region in the world for sending remittances. The continental average for remittance costs is 7.9%. This is accompanied with high variance where some corridors average in excess of 30%. Expensive corridors within the region offer the biggest opportunity for mobile-enabled remittances as most already have live mobile money services offering international money transfer (IMT) today. It may well be that, similar to the experience we have witnessed on the UK-Kenya corridor, migrants are already taking advantage of these lower-cost services.

More can be done to enable these flows. To be able to take advantage of formal mobile and digital remittance channels, migrants need access to the regular pathways that permit them to migrate safely to countries of destination and to open formal accounts. At a regulatory level, permitting non-bank operators to process remittances is the best way to stimulate the competition that brings prices down. Permitting tiered-KYC and customer onboarding allows those migrants and refugees lacking formal documentation to open basic transaction accounts for making mobile payments and receiving remittances.

Countries that have already adopted these measures are already bearing the fruit, such as Kenya. Other countries in the region are poised to take similar advantage. If an enabling environment can be implemented more widely it can drive the adoption of digital and mobile remittance channels, helping to bring down costs and promoting financial inclusion throughout the continent and help to achieve the SDG 10.c target.

This year, the GSMA Mobile Money programme is conducting a survey that will determine the costs of remittances where mobile money is at both ends of the transaction (mobile money to mobile money remittances) and the challenges that are hindering sending and receiving corridors. Look out for this exciting research.