Interoperability refers to different systems, devices, applications or products connecting and communicating effectively and seamlessly. This concept is critical in various fields including information technology, healthcare, and telecommunications, where diverse systems need to exchange data and talk to each other without barriers.

What is mobile money interoperability?

Interoperability in the mobile money ecosystem comes in various dimensions (Figure 1).

Figure 1: Dimensions of mobile money interoperability

| Dimension | Horizontal or vertical | Description |

| Network interoperability | Vertical | Any mobile money service can be provided on any mobile operator’s network. This is not currently implemented in mobile money markets. |

| Platform interoperability (account-to-account (A2A) interoperability) | Horizontal | Users of one mobile money service can transfer or make payments to another mobile money provider. This is the most common type of mobile money interoperability. It applies domestically or across borders and between mobile money services or to other financial service providers like banks. |

| Agent interoperability | Horizontal | Agents can serve users of multiple mobile money providers with a single shared float. This differs from agent non-exclusivity, where a single agent holds accounts, and separate floats, with multiple mobile money providers. |

| Merchant interoperability | Vertical | Users can pay a merchant regardless of the mobile money provider account they hold, without needing further KYC processes. This is rare in mobile money markets. |

| Data interoperability | Can be both | Where data and information generated by one service provider are transferred and used by other service providers. Consumer data protection is an important consideration here. This is not currently widespread in mobile money markets. |

Source: GSMA 2024, The impact of mobile money interoperability on financial inclusion

Horizontal platform interoperability (A2A) is the most prevalent type of interoperability in the mobile money industry.

It comprises five core components:

- Connection refers to the mechanism through which digital financial service providers (DFSPs) interconnect and exchange information.

- Settlement allows “real” money to flow between participating organisations.

- Governance refers to the way participants of an interoperability solution make decisions.

- The pricing and business model determine the profitability and sustainability of an interoperability solution.

- Finally, dispute resolution mechanisms enable DFSPs to reach a consensus on a transaction’s status and financial liabilities in the case of a disagreement.

These core components can lead to different technical models for interoperability. In the bilateral model, participants form one-to-one connections. This can be extended to more than two participants to create a multilateral agreement. In the aggregator model, a third party already integrated with multiple ecosystem players establishes payment interoperability between participants. The mobile money hub model requires mobile operators to set up a central entity that connects them and other DFSPs. In the global payments hub model, a non-mobile operator sets up the central hub. This includes cases where governments require providers to connect to a national switch.

Mobile money interoperability is more prevalent than ever

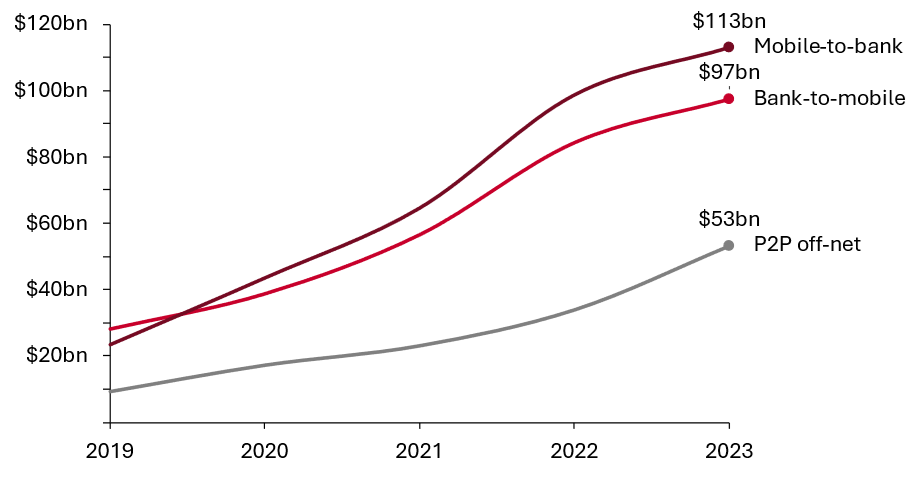

The growth of mobile money interoperability is clear given the evolution of specific use cases. Between 2019 and 2023, mobile-to-bank transaction values grew fivefold, bank-to-mobile transaction values grew threefold, and person-to-person (P2P) off-net transaction values (between wallets of different mobile money providers or domestic transfers to unregistered users) grew sixfold (Figure 2). In 2023, mobile money providers participating in the Global Adoption Survey were connected to 27 banks on average – almost 50% more than the previous year.

Figure 2: Global mobile-to-bank, bank-to-mobile and P2P off-net transaction values, 2019-2023

Source: GSMA Global Adoption Survey and estimates

Why does mobile money interoperability matter?

A2A interoperability is more convenient for users because it allows access to customers outside a mobile money provider’s network. Before the introduction of A2A interoperability, P2P transfers across different networks included over-the-counter (OTC) transactions and vouchers. As these alternatives are less convenient for users, they can promote the use of cash. A2A interoperability can lead to P2P transfers that are also faster, more affordable and more secure.

Interoperability supports government objectives too. It can lead to more inclusive digital economies by expanding access to financial accounts and making funds more secure. It can also enhance the effectiveness of monetary policy tools through better traceability of financial transactions.

The rise of A2A interoperability has led to more funds entering and leaving the mobile money ecosystem digitally rather than through cash conversions. While cash-in remains the dominant source of funds entering the mobile money ecosystem, bank-to-mobile transfers are catching up (Figure 3). In 2023, these were equivalent to almost a third of the value cashed in. More funds are exiting the ecosystem through mobile-to-bank transactions, equal to almost half the value of cash-outs in 2023. Digital flows accounted for 60% of total mobile money transaction values in 2023, up from 55% in 2019.

Figure 3: Global bank-to-mobile and mobile-to-bank transaction values as proportions of cash-in and cash-out, 2019 – 2023

Source: GSMA Global Adoption Survey and estimates

Mixed evidence for mobile money interoperability’s impact on financial inclusion

In 2024, the GSMA published a report that explored the effect of mobile money interoperability on financial inclusion in Ghana, Kenya, Malawi, Rwanda and Tanzania. The report assessed how mobile money adoption and usage evolved under different models of interoperability. In Kenya, market-led interoperability took effect in 2018. In the other four markets, interoperability is now a regulatory requirement via the national switch.

In four markets, mobile money adoption was already high before interoperability was implemented. This is because incentives to become interoperable often occur after mobile money has reached scale. In these cases, financial inclusion preceded interoperability – not the other way around.

In Kenya, Rwanda and Tanzania, interoperability solutions designed and led by mobile money providers were accompanied by increased mobile money adoption and usage (higher average transaction values).

The impact of national switch-led interoperability on financial inclusion remains unclear. More time is needed to assess whether national switches in Rwanda (eKash) and Tanzania (TIPS) have affected mobile money adoption and usage. Evidence from Ghana and Malawi on the role of national switches is inconclusive.

Organisations that opt in to interoperability do so to expand their customer base, increase returns from new and existing products and add value through a more convenient and efficient platform. In Kenya and Tanzania, this happened once mobile money had achieved sufficient scale.

Governments often push for interoperability to drive competition, but there are trade-offs involved. Interoperability can increase participants’ costs, discourage innovation and reduce product differentiation in dynamic, fast-moving markets.

Policymakers should consider specific market dynamics before intervening, particularly implementation timing. Imposing mandatory interoperability too early can lead to regulatory failure and slow market and technological development.

Is mobile money interoperability sustainable for providers?

Another GSMA study in 2024 looked at how commercially sustainable interoperability initiatives are for providers. It highlighted the benefits and challenges in three countries (Figure 4).

Figure 4: Commercial benefits and challenges of mobile money interoperability

| Country | Interoperability commercial benefits | Interoperability commercial challenges |

| Ghana | Interoperability has driven transaction growth. Common price structure and range: The ‘receiver pays’ model was selected because interoperable payments mainly flow from small sending providers to larger ones. | Transaction failures affect the reliability and trust in the system. Due to a lack of consensus, mobile money providers prefer bilateral connections (e.g. for merchant payments). |

| Jordan | To promote the hub, the central bank introduced a two-year grace period for new provider onboarding. Interoperability allows mobile money providers to reach a wider customer base and is a foundation for alternative revenue. Interoperability has stimulated transactions. Mobile money providers contributed to discussions about business rules and fees. Mobile money providers have expanded use cases to include credit and international remittances, creating new revenue streams. | Reaching consensus and rule setting among interoperability participants is time-consuming. Newly introduced switching fees put pressure on provider revenue. Mobile money providers faced technical issues at the inception of interoperability, but clear service level agreements (SLAs) have helped. Mobile money providers might incur costs related to technical upgrades and compliance with standards. |

| Tanzania | Interoperability, especially via TIPS, has helped mobile money providers reach more customers, and facilitates various transaction types including cross-border transactions. For one mobile money provider, on-net P2P transactions increased seven-fold within the first year of becoming interoperable. | There are profitability concerns under TIPS where pricing might be set by regulators. The P2P interchange agreement took one year, while the merchant payment interchange was not settled by the end of 2023. |

Source: GSMA 2024, The commercial sustainability of mobile money providers in interoperability initiatives

In mature markets, interoperability is a strategic tool for expansion and partnership rather than a direct source of revenue.

Mobile money A2A interoperability combines core components that can generate a range of models. It has grown significantly and supported the digitalisation of cash transactions. Mobile money interoperability offers convenience to users and supports key government objectives. However, there is mixed evidence for its impact on financial inclusion, and governments should consider trade-offs and specific market dynamics before imposing mandatory interoperability.

Overall, mobile money interoperability can offer many advantages to stakeholders. For long-term success, it needs to work for all service providers. Technical solutions should include multiple points of redundancy to avoid total system outages during operational disruptions. Implementing redundancies, such as maintaining bilateral interoperability while deploying national switches, can enhance system resilience and ensure continuous service delivery. Where possible, interoperability should use existing infrastructure to minimise costs. It must be priced sustainably, and mobile money providers should be part of the decision-making process when interoperability solutions are centralised.

Learn more about the GSMA Mobile Money Programme’s work on interoperability here. The annual State of the Industry on Mobile Money includes data and analysis on interoperable transactions here.