Seven years after stepping into the ‘Warm Heart of Africa’ (as Malawi is aptly promoted), I had the opportunity to conduct several weeks’ field-research to investigate whether the proliferation of mobile handsets and network coverage had led to demand and opportunity for digitised agricultural value chain payments. Having spent almost two years working with smallholder tea farmers in the Southern Highlands, I was excited to compare their needs against smallholders from other value chains.

Our mAgri team has been working to support the development of mobile-based agricultural content services for smallholder farmers, aimed at enhancing their farming practices and improving their yields. In parallel, our programme has conducted extensive research into the potential for the digitisation of agricultural value chain payments (please see this report for the global opportunity).

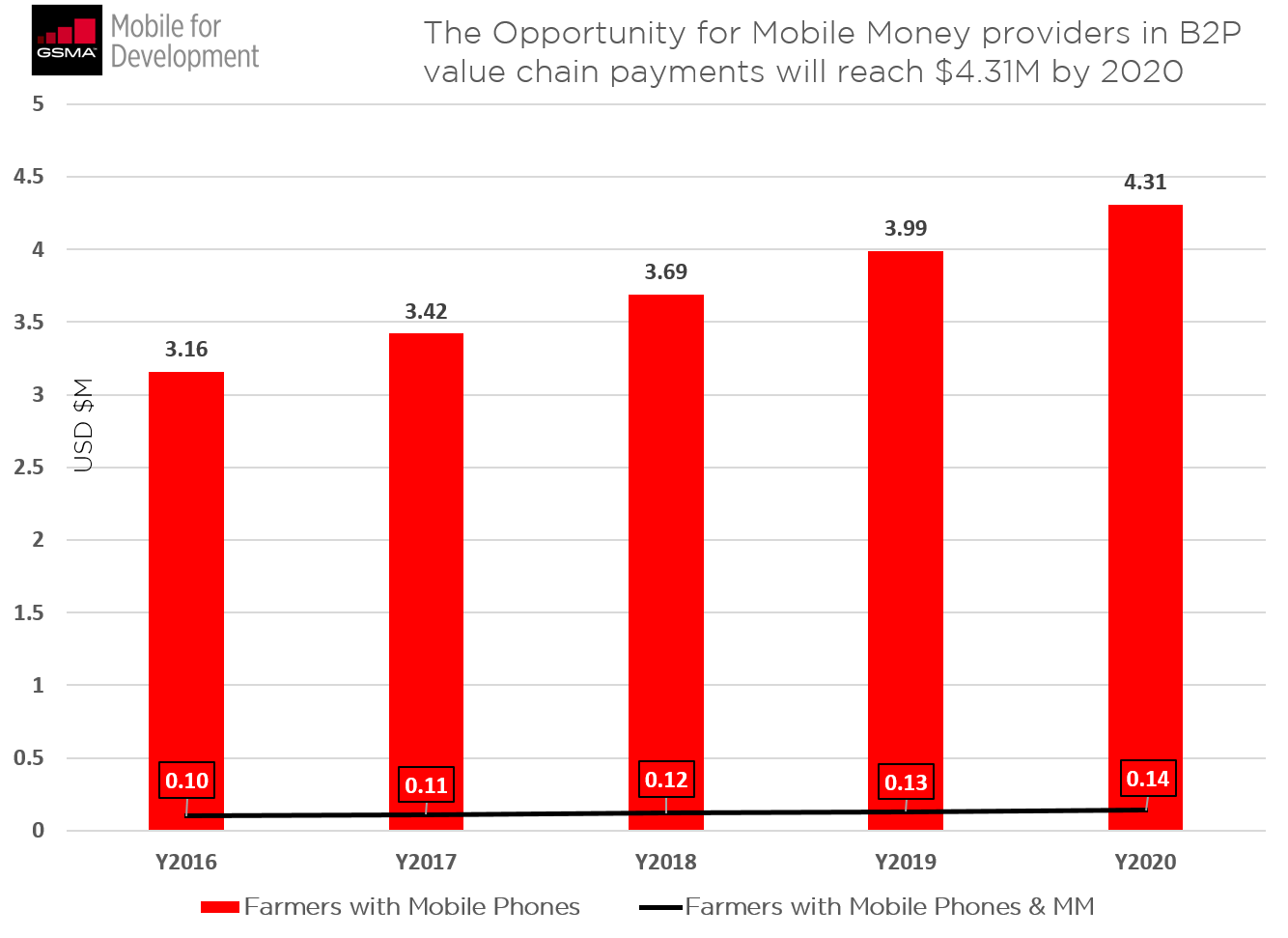

Figure 1 – Business to Person value chain payment estimate for Malawi. *MM = mobile money

During three weeks of field research in February 2017, our mAgri team spoke to a number of agribusinesses and smallholder farmers across the country to understand their Business to Person (B2P) interactions and payment needs. It was important that the research illustrated the following aspects:

- The current demand for digital payments;

- How they would compare to complimentary propositions; and

- Whether digitisation of agribusiness payments to farmers provides a meaningful value proposition.

The research uncovered opportunities for MNOs to design a service that meets the needs of multiple agricultural value chains.

Highlights and key findings from the field:

Dairy:

In the vast majority of cases, dairy farmers are organised around milk bulking groups (MBGs) which aggregate and store farmers’ milk ready for collection by commercial buyers. The MBGs themselves are not operating or behaving as an agribusiness and do not handle some of the business processes or administrative tasks that payment digitisation can most directly benefit. Two additional barriers included a lack of direct payments from the MBG to farmers or a sufficiently large number of progressive farmers who were adequately mobile/technology literate to try mobile money services.

Multi-crop:

An agribusiness purchasing multiple crops was focusing on developing relationships with existing farmers to achieve growth targets, rather than onboarding new farmers. They see that there is scope for sufficient yield increase through proper extension support and contract-farming agreements.

With trucks sent to the field to buy crop from smallholders in remote areas, digital payments offer the agribusiness (and farmers) significant security benefits. In addition, this also means that more purchases could occur per trip, as the buyer was not limited to the amount of physical cash at hand. The business was also interested in digitising other elements of their supply chain in order to improve efficiencies, which could leverage the mobile network to relay information (such as volume of crop bought), back to the processing centre.

Tea:

Tea is a well-established value chain in Malawi and second largest export crop, employing tens of thousands of Malawians. The estates have well organised farm management systems with regular productivity and commercial targets to on which to deliver. They have established strong relationships with smallholders who are organised into associations and benefit from extension support. These factors, combined with a sizable number of progressive farmers (early adopters) makes tea one of the more attractive value chains for digitisation.

Groundnuts:

Initial research highlighted groundnuts as an attractive value chain for digitisation based on frequency of payments and volume of crop production. However, the fragmentation of export buyers, agents and dealers means that agribusiness-farmer relationships are relatively weak. With no formal contracts between the agribusinesses and farmers, the cost of the necessary education to on-board farmers to accept crop payments through mobile money, with no guaranteed return, reduces the crops’ attractiveness. Farmer records are not yet sufficiently digitised to realise the benefits of regular digital B2P payments.

Condensing these findings, we’ve identified the following key factors for agribusinesses to consider digitising agricultural payments:

- Progressiveness (agribusiness commercial ambitions);

- Relationship with farmers (1:1 relationships, contracted faming, extension support – seen as trusted/needed); and

- Pain of existing payments procedures (inefficiency of manual process, risk).

Barriers to digitisation:

Farmers receiving payments via mobile money will need to be educated on how the service works. Further, they will initially expect to cash out immediately from a mobile money agent, although this should become less prevalent with time. Agent density and liquidity will have to be significantly scaled up and carefully managed to accommodate fortnightly or monthly peaks in transaction frequency. Agents and Super Agents incentives will need to be customised to encourage improved rural liquidity management and cash availability.

Key recommendations and next steps:

From this research, we are working with an operator to develop a new digital payments pilot with a priority on establishing processes for overcoming the highlighted barriers via the following approach:

1. Gain commitment and buy in from key stakeholders (agribusiness, farmer representatives and MNO)

2. Strengthen and prepare area agent networking

- On boarding agents or retraining them for the rural context

- Prepare logistics of rural liquidity

3. Prepare agribusiness accounting and payroll systems for mobile payments

4. Segment progressive farmers (potential early adopters) for initial product training

5. Start with small numbers of farmers and aim to carefully scale once processes have been validated, in line with the agent’s capacity to maintain sufficient liquidity.

Call for mAgri B2P Engagement Partners:

Our mAgri programme has just launched our latest initiative where we are offering a variety of support packages to MNOs with a keen interest in digitising agri value chains across Asia, Africa and Latin America. For more information, please email us at [email protected].