The launch of South Sudan’s first mobile money transfer services in 2019 – m-Gurush and Nilepay, both in partnership with Zain – was a key milestone in the country’s journey to financial inclusion. South Sudan gained independence in 2011 but has continued to suffer from instability, economic stagnation, conflict, and poverty. A revitalised peace agreement signed in 2018 paved the way for some social and economic progress.

The introduction of mobile money in South Sudan has allowed development organisations to distribute cash assistance through mobile channels. Humanitarian organisations have gradually substituted in-kind donations for cash disbursements, as preferred by beneficiaries. However, providing cash assistance through mobile money requires access to mobile phones, connectivity, and digital literacy among affected communities. Additional care and consideration are necessary for marginalised groups, such as women and those with disabilities, who are less likely to be digitally included. Using mobile money to distribute cash transfers has also been more effective and cost-efficient: moving large amounts of cash through high-risk areas in South Sudan often required security services, costing up to 30% of the transfer value. Mobile money has improved payment confidentiality too, ensuring the safety of beneficiaries.

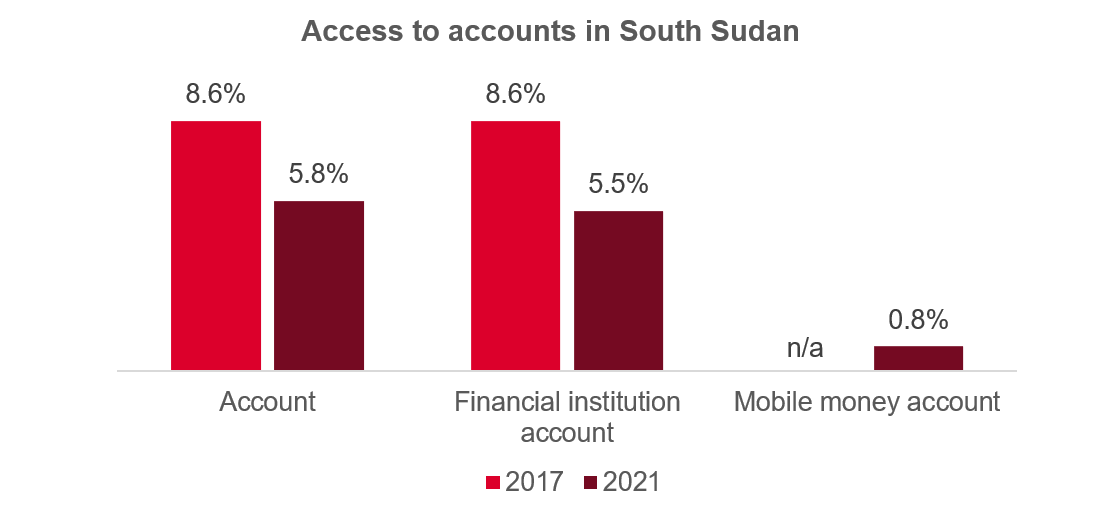

Financial inclusion in South Sudan is low. In 2017, less than 10% of the adult population held an account (at a bank, financial institution, or through mobile money – Figure 1). Mobile money adoption can help drive financial inclusion, enabling easier and faster financial transactions, reducing the risk of theft, and providing access to savings. This in turn contributes to resilience in a country where external shocks, such as conflict or natural disasters, are common.

Figure 1: Financial Inclusion Profile for South Sudan

Source: The Global Findex database

Note: Account is defined as – The percentage of respondents aged 15 and over who report having an account (by themselves or together with someone else) at a bank or another type of financial institution or report personally using a mobile money service in the past year.

The Bank of South Sudan first introduced regulations governing and supporting mobile money in 2017. However, in 2021, two years after the introduction of mobile money, less than 6% of the adult population held an account. While this trend was mostly driven by lower financial institution account access, mobile money account penetration in South Sudan was less than one per cent in 2021. Conversely, mobile account usage in sub-Saharan Africa had risen to 33% at the same time.

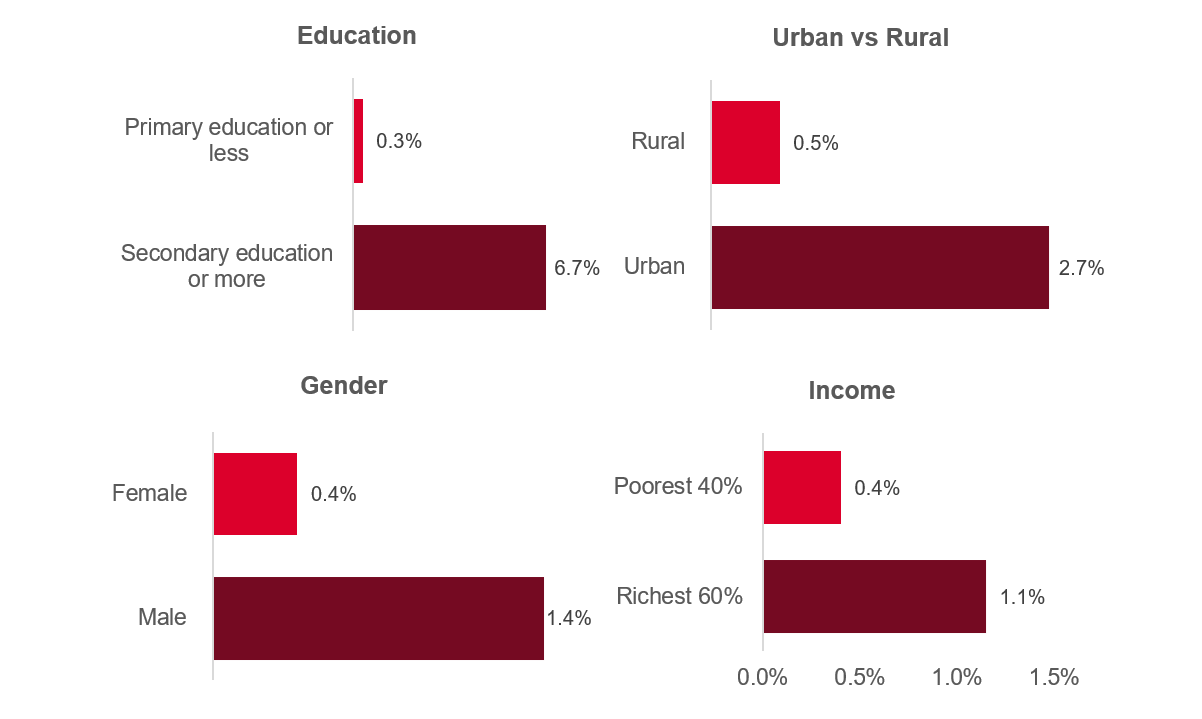

In South Sudan, people are more likely to have a mobile money account if they are better educated, live in the city, are male, and are wealthy (Figure 2). Financial inclusion policy should aim to narrow these gaps to improve the impact of mobile money on socio-economic outcomes.

Figure 2: Mobile Money Account Usage by Group (2021)

Source: The Global Findex Database

Note: Figure 2 refers to the percentage of the population aged 15 and over

Mobile money adoption and financial inclusion have faced significant structural challenges in South Sudan. Inadequate telecommunication infrastructure contributing to patchy network coverage has restricted mobile money use, especially in rural areas. Limited access to electricity and low mobile phone penetration also affected mobile money uptake. The long distances between residents and mobile money agents have proved challenging too. In 2019, around 83% of rural inhabitants had to walk at least 30 minutes to reach an agent; this was the case for only 40% of urban dwellers. To overcome this, the country’s first local telecom operator, Digitel, launched in 2021, is working to improve mobile network infrastructure in remote areas.

Socioeconomic barriers have limited mobile money uptake. Persistent underdevelopment and low purchasing power are a constraint, as is a lack of identification documents (ID). In 2019, only 41% of the population had the required ID to access mobile money subscriptions.

There are more than two million internally displaced people in South Sudan due to ongoing inter-communal conflicts, insecurity and flooding. Displacement-affected populations in South Sudan use mobile wallets to send and receive money from friends and family or to buy airtime. However, mobile phone penetration among displaced communities is hindered by high costs, limited access to charging, low literacy, and low digital literacy.

Economic and health risks presented by COVID-19 have exacerbated the situation. South Sudan’s currency depreciated by 97% between September 2019 and October 2022. To overcome this volatility, m-Gurush offers USD-only mobile money accounts. The company supports P2P transfers, mobile-to-bank transactions, outward international remittances, bill payments, as well as cash-ins and cash-outs at agents in both South Sudanese pounds and US dollars.

M-Gurush also halved transaction costs in 2022 to 4% relative to their inception, supporting affordable access to their services. Such adaptation is necessary to support mobile money’s growth while the economy stabilises but may not be enough on its own to achieve scale. MTN recently began providing mobile money in South Sudan, which could further improve access to financial services by offering customers additional choice. More competition in the industry should lead to better quality services and more affordable prices, driving scale.

While there remain substantial obstacles in the way to financial inclusion in South Sudan, mobile money has the potential to play a key role in the journey.

To find out more about the growth of the industry, read our milestone 10th State of the Industry Report on Mobile Money.