The post is part of a series looking at key findings from the 2014 State of the Industry Report on Mobile Financial Services.

In last week’s blog post in series, we reported that there were 255 live mobile money services as of December 2014. This week, I’ll explore how customers are accessing mobile money services and try to answer the following question: How is the mobile money industry helping to increase access to financial services?

To access and use mobile money services, customers rely on two distinct channels. The first is the network of physical access points where they can typically deposit cash into, or take cash out of, their mobile money account – these access points are primarily agent outlets. The second is the technical access channel – the interface that customers use to initiate transfers and payments directly on their mobile handsets.

Agent networks grow in 2014

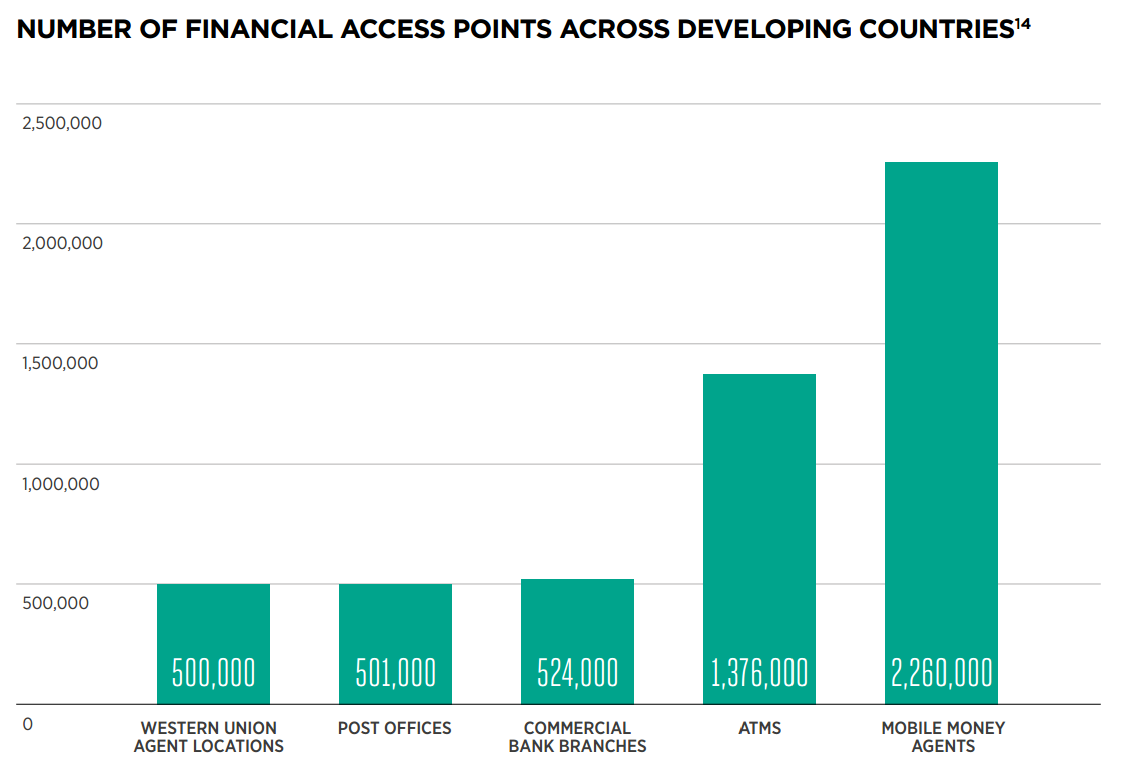

The number of mobile money agent outlets grew by 45.8% in 2014, reaching a total of 2.3 million globally in December.[1] This is particularly impressive if we consider the size of traditional financial institutions’ and remittance services’ networks. In 75% of the markets where mobile money is available today, agent outlets outnumber bank branches [2]. In more than 20 Sub-Saharan Africa markets, as well as Bangladesh and Pakistan, there are more than 10 times as many registered mobile money agent outlets than commercial bank branches.

While the bulk majority of mobile money physical access points remain agent outlets that each provider sets up individually, a growing number of mobile money providers are forming partnerships to leverage alternative existing distribution networks and thus increase the number of cash-in and cash-out points available to customers. This includes tapping into existing networks of bank branches, ATMs, MFIs, post offices, petrol stations, bus companies and pharmacies.

Despite knowing how many mobile money agent outlets there are globally, we know less about the actual reach of this network and just how far it extends access to financial services into hard-to-reach, and often underserved, locations. This year’s survey figures indicate that there is still room for the industry as a whole to better understand the reach of agent networks – less than a third of respondents were able to report what percentage of their agents were operating in rural vs. urban areas.

Activating registered agents

To successfully serve customers, mobile money providers need to do more than simply register agents; they need to ensure their agents are active, which is significantly more challenging, particularly for service providers that have not yet reached a critical mass of mobile money users in the market.[3] The total number of active mobile money agent outlets that facilitated at least one transaction during a month grew by 44%, rising from 946,000 in December 2013 to 1.4 million in December 2014. This year, the global average active rate[4] remained stable at 60% – though this global figure masks stark variances across regions.

In West Africa for example, a region which has really seen mobile money services grow in the past year and a half[5], the agent active rate rose faster than anywhere else to reach 43% (up by 11 percentage points from last year). By contrast, in both Middle East & North Africa and Latin America & Caribbean, where mobile money is yet to really take off, agent activity rates decreased, by 9 percentage points and 13 percentage points respectively, as mobile money providers have focused on quickly registering large numbers of agents to increase the number of access points for customers.

Accessing a mobile money account from a mobile handset

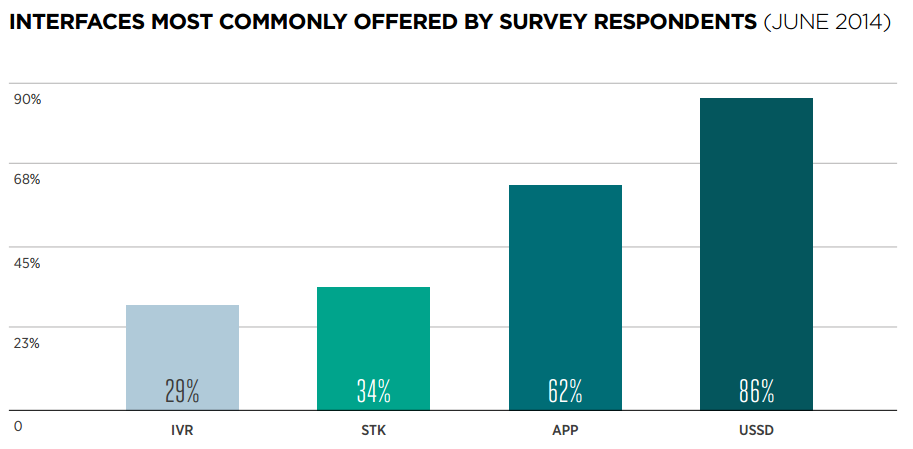

The technical interface that a mobile money account holder uses to initiate transactions from a mobile handset can have a significant impact on customer experience. Today, the majority of mobile money services are available through two or more interfaces – usually USSD[6] and one or more other interface(s) – STK[7], IVR[8] and Apps[9].

By diversifying the types of interfaces available to access a mobile money account, providers can target different customer segments within their markets. For example, the IVR interface, which can be adapted to numerous local languages and dialects, can help providers target illiterate communities, as well as people who aren’t comfortable interacting with data services, typically through USSD, on a mobile handset. Additionally, well-designed apps can dramatically improve user experience by providing rich user interfaces and enhanced functionality[10]. Apps are also helping operators to target the growing segment of smartphones users in developing markets. As low-cost smartphones and data packages become more widely available, the number of operators offering mobile money apps is likely to increase.

In the next post in our series, we’ll explore how many registered and active mobile money customers there were globally in 2014.

Notes:

[1] At the end of 2014, there were 2.3 million mobile money agent outlets. However, this is not the number of unique mobile money outlets but rather the sum of the outlets providing cash-in and cash-out services for each of the 255 mobile money services that are available globally. Indeed, in many markets, individual outlets may serve several mobile money service providers. This practice is more pronounced in mature mobile money markets, particularly where competition amongst service providers is high. For that reason, the number of mobile money agent outlets published in this report must be interpreted with care as it does not reflect the number of unique mobile money cash-in and cash-out locations.

[2] Data on bank branches available from the IMF Financial Access Survey (FAS) Database.

[3] For more information on incentivising a network of mobile money agents and boosting activity, see Neil Davidson & Paul Leishman. “Incentivising a Network of Mobile Money Agents.”

[4] The ratio of active agent outlets over registered agent outlets.

[5] Claire Pénicaud Scharwatt (2014), “Mobile Money in Côte d’Ivoire: A Turnaround Story.”

[6] USSD (Unstructured Supplementary Service Data) is the protocol for sending text across GSM networks.

[7] STK (SIM Application Toolkit) enables the SIM to initiate actions for various value-added services.

[8] IVR (Interactive Voice Response) technology allows a computer to interact with humans through the use of voice and DTMF (dual-tone multi-frequency signalling) tones input via keypad.

[9] A mobile app is a computer program designed to run on smartphones, tablet computers and other mobile devices.

[10] For more on smartphones and mobile money, see: Almazan & Sitbon (2014) “Smartphones and mobile money: the next generation of digital financial inclusion.”