Last week at Mobile World Congress, MMU released its 2014 State of the Industry Report on Mobile Financial Services. In the coming weeks, the team will present some key findings and insights from this report in a series of blog posts. In this post, I’ll explore the availability of mobile money services globally and try to answer the following question: What does the global mobile money industry landscape look like in 2014?

How many mobile money services are there globally?

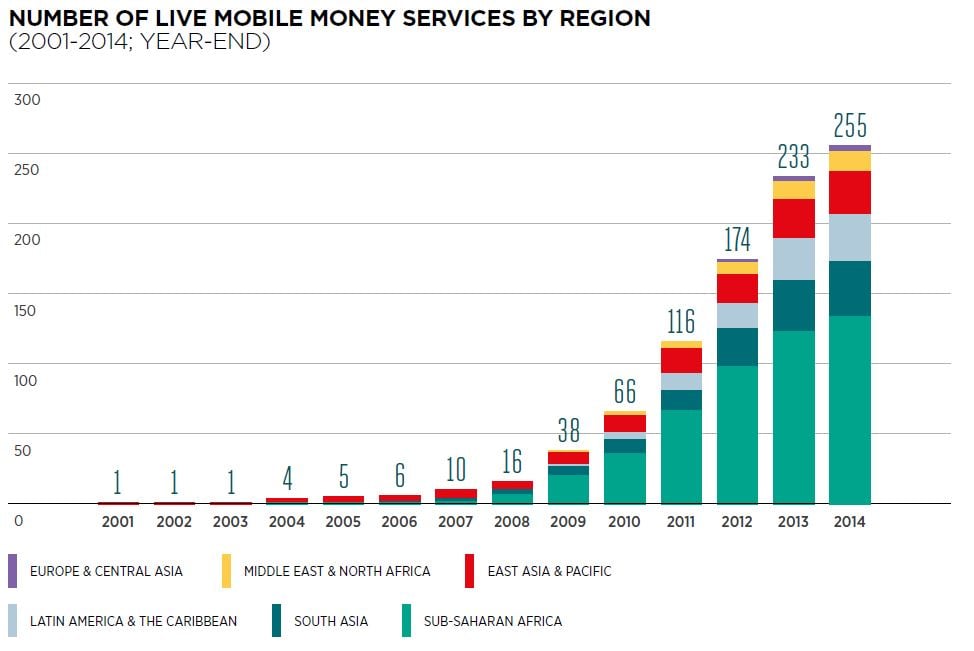

With 255 services in 89 countries as of December 2014, mobile money is now available in 61% of developing markets worldwide [i]. With mobile money now maturing across many developing regions, the number of new launches each year is decreasing steadily. Twenty-two new services were launched in 2014, compared with 60 launches in 2013 and 58 launches in 2012.

Whilst Sub-Saharan Africa still accounts for the majority of live services globally (53%), in 2014 half of all launches occurred outside the region – with each of the following regions seeing three launches respectively; South Asia, Latin America & Caribbean and East Asia & Pacific. This year, mobile money was launched for the first time in six new markets: Dominican Republic, Myanmar, Panama, Romania, Sudan, and Timor-Leste.

Increased competition and growing interest in interoperability

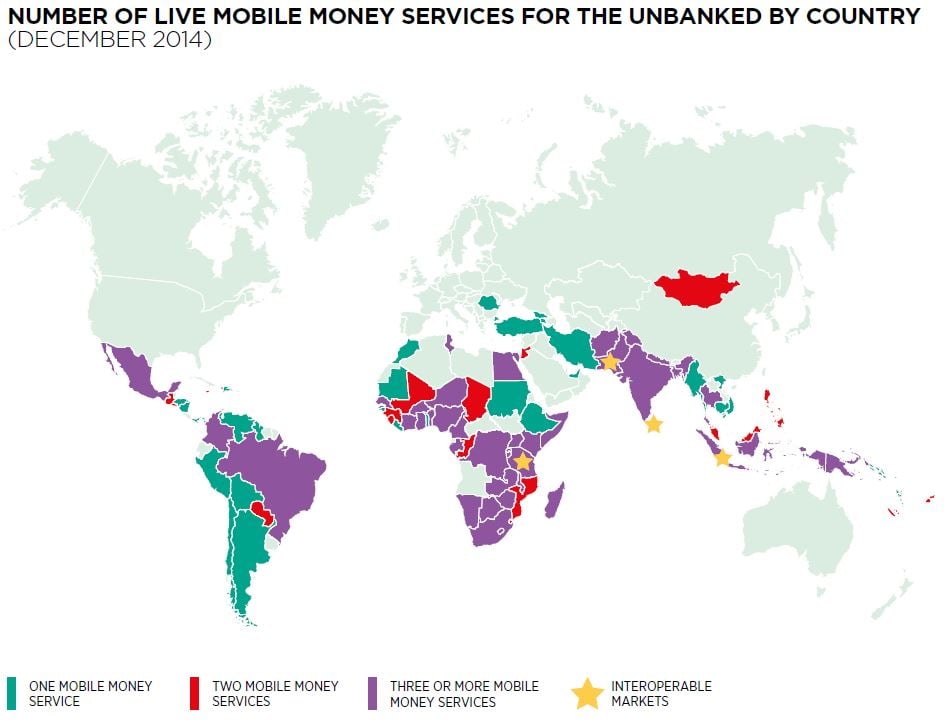

Globally, 56 markets now have at least two live mobile money services, and 38 of these markets have three or more live services. As markets become increasingly competitive, MNOs are showing a growing interest in the development of interoperable solutions. They are beginning to consider the benefits of A2A (account-to-account) interoperability, both in terms of increasing transaction volumes and revenues, and in terms of improving the customer experience by making it easier for consumers and businesses to send money domestically across networks. In 2014, interoperable mobile money services were launched in three markets – Tanzania, Sri Lanka, and Pakistan – following Indonesia, where interoperability was implemented in 2013.

A barrier to deploying mobile money in new countries

There are currently 54 developing countries that do not have a live mobile money service. Seventy percent of these countries have a total population of less than 10 million. A small addressable market size (one less than 10 million) makes it harder to build a business case for investment in mobile money, since it is more difficult for a mobile money service provider to achieve scale, lower costs and reach profitability. In addition, many of these markets are geographically small territories (including many Pacific and Caribbean islands), where it can be harder to build a P2P use case since people are less likely to be widely dispersed.

Just 13 of the 54 developing markets where mobile money services are not yet available have a total population of more than 10 million, including Algeria, Ecuador, South Sudan, Ukraine, and Yemen, among others. Within these 13 markets, 14 mobile money launches are planned, indicating a high level of interest from mobile money providers. However, in most of these countries, a non-enabling regulatory approach appears to be slowing down the launch of these services.

Enabling regulatory developments in 2014

An increasing number of regulators are recognising the major role mobile money services can play in fostering financial inclusion and economic growth, and are establishing enabling regulatory frameworks for mobile money. In 2014, new regulation was passed in Colombia, Kenya, India and Liberia. Today, in 47 out of 89 markets where mobile money is available, an enabling regulatory approach allows both banks and non-bank mobile money providers to deliver services in a sustainable way. It is critical that regulators create an open and level playing field for mobile money services, where non-bank providers can enter the market, as evidence shows that regulatory barriers can slow down both market uptake and customer adoption. Globally, MNOs are playing a key role in the delivery of mobile money services—over 60% of all mobile money services are operationally run by MNOs [ii] and, in Sub-Saharan Africa, over half of all MNOs have already launched a mobile money service (75 out of 144).

In the next post in our series, we’ll discuss the accessibility of mobile money services, focusing on the two distinct channels that customers use to access mobile money services: agent outlets and the technical interface for mobile money accounts.

Notes:

[i] Based on the World Bank list of developing countries. There are four markets where MMU tracks mobile money services for the unbanked, which do not feature on the World Bank’s list of ‘developing markets’. These are: Chile, Qatar, Singapore and UAE. Full list available at: http://data.worldbank.org/about/country-and-lending-groups

[ii] By our definition, a mobile money service is operationally run by an MNO when the MNO is ultimately responsible for the design and implementation of the majority of the operational strategy, including distribution, marketing and customer care.