By

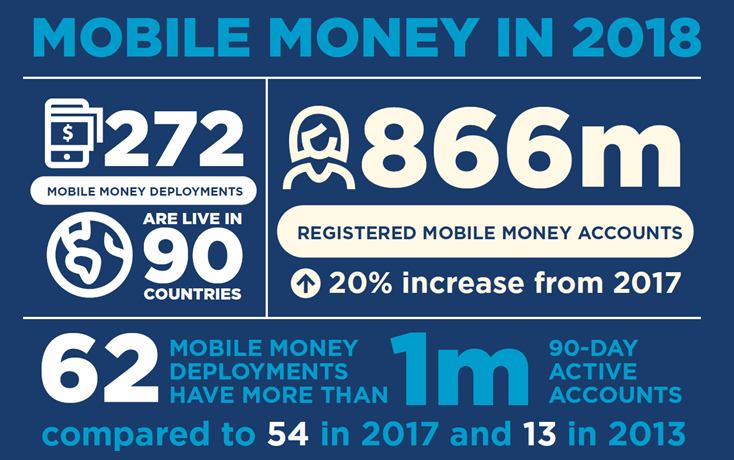

By With more than 866 million registered mobile money accounts globally and $1.3 billion processed daily, mobile money serves as a critical infrastructure for start-ups looking to increase digital payment adoption among their customers.

Inspired by this, the GSMA Ecosystem Accelerator and Mobile for Development Utilities teams hosted an online clinic diving into mobile money adoption strategies specifically for start-ups in Asia Pacific and Africa. Anant Nautiyal, Senior Manager for Inclusive Fintech, and Nika Naghavi, Data and Insights Director, who work in the GSMA Mobile Money programme gave an overview of the mobile money industry as it undergoes crucial technological and organisational transformations. Four start-ups within the GSMA Ecosystem Accelerator and Mobile for Development Utilities portfolios – eSewa and Gham Power (Nepal), MaTontine (Senegal), Safe Water Network (Ghana), presented their respective challenges to mobile money adoption and their strategies to overcome them.

Source: GSMA Mobile Money, 2019

When it comes to driving mobile money adoption, start-ups face a range of different challenges depending on the context and sector that they operate in. Here are some of the barriers identified by the four start-up grantees:

Educational and digital literacy barriers

For many start-ups, particularly those operating in rural or low-income settings, their customers are first time mobile money users. Addressing education and digital literacy barriers is therefore critical for driving mobile money adoption and providing greater access to the start-up’s product offering.

- In rural Ghana, Safe Water Network (SWN), operates mobile money-enabled prepaid household meters, and water treatment and distribution stations. Initially, their users lacked trust in the technology. To resolve this challenge, SWN partnered with MTN Ghana to tackle educational and product design barriers through interactive group work-shops and one-one sessions, as well as a promotional campaign offering prizes to the ‘super-star’ mobile money users. Though cash still represents a significant proportion of total payments, the impact of the joint-campaign is evident.

- Gham Power develops solar microgrids and solar water pumps, which heavily relied on digital payments for cash collection in rural Nepal and so partnered with mobile operator Ncell ,and eSewa, a digital wallet provider, to leverage their agent networks. Gham Power invested in training agents with video tutorials and ensured that agent incentive structures were designed to drive digital payment adoption among rural customers.

Product design barriers

These can include language restrictions, lacking suitability for basic and feature phones, and the limitations of USSD, culminating in poor customer experience and user experience (CX/UX), and therefore poorly designed products not suitable for targeted users.

- SWN realised the importance of communicating with its customers and employed the use of SMS notifications to communicate about deductions from customers’ MTN mobile wallets – fostering an environment of trust and transparency with low-income users. Here SWN noticed that slight differences in the wording of automated messages (‘somebody’ vs. ‘someone’) have profound implications for its ability to communicate with customers effectively.

- MaTontine is a mobile solution that digitises traditional savings circles (‘tontines’) to facilitate access to credit and financial services. Given the low smart phone penetration in Senegal, MaTontine had to ensure that its product offering could operate on basic and feature phones, whilst facilitating trust in their digital service for their female users.

Photo of MaTontine customers

Affordability barriers

When mobile money transaction fees account for a significant proportion of the average end-user utility bill payment, it can be a significant barrier to adoption, along with weakening the economic case for mobile money adoption for businesses that rely on small frequent transactions (such as pay-as-you-go). This is particularly true for first-time mobile money users and in nascent mobile money ecosystems, where fees are often interpreted as an insurmountable entry cost.

- Given the immense operational cost savings from high mobile money adoption, SWN decided to absorb the mobile money transaction fee charged to its customers in order to ensure widespread adoption among its customer base. (Read our blog on mobile money transaction fees and utility bill payments).

Photo of a SWN employee explaining mobile payments to a customer

Photo of a SWN employee explaining mobile payments to a customer

“The importance of customer education cannot be overemphasised” – Charles Yeboah (Head of Innovation, Safe Water Network)

To overcome the challenges outlined above, there are other imperatives for start-ups to consider when aiming to collaborate with a mobile money provider.

- Mobile operators and start-ups are working together to adopt the right mix of “tech and touch” along with driving financial literacy. Digital solutions can reduce operational expenses but regular touch points with customers remain important – especially when on-boarding new customers.

- Given their human resource and organisational constraints, MNOs will be more responsive to the needs of start-ups when they clearly demonstrate value through their ability to scale and drive mobile money transaction frequency and value.

- Starts-ups can leverage the MNO’s agent network and brand recognition as mobile money agents are becoming increasingly skilled at on-boarding new customers – particularly in rural areas.

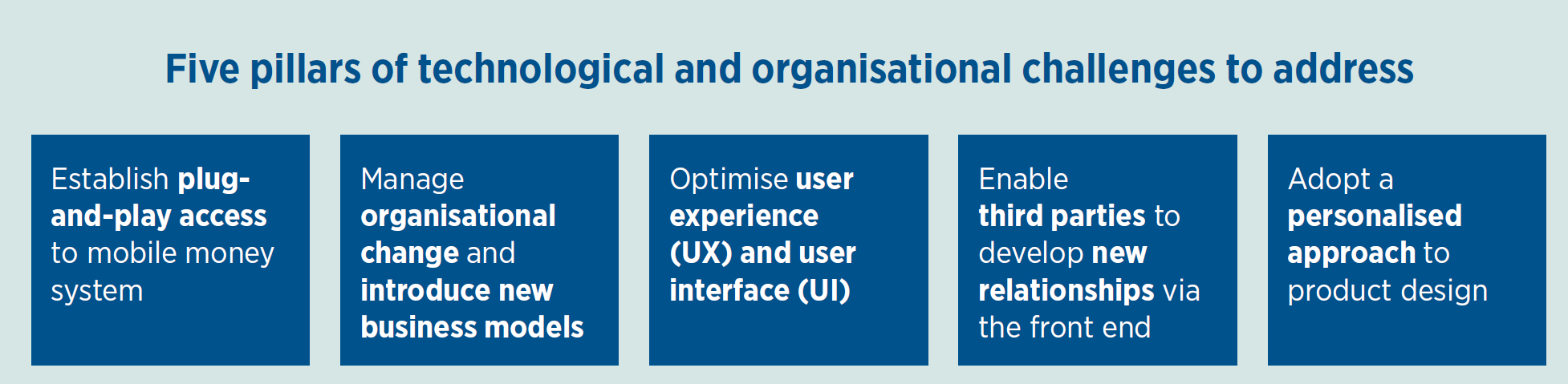

Meanwhile, Nika Naghavi and Anant Nautiyal identified five technological and organisational challenges that mobile money providers must address to become more responsive to the needs of start-ups, in order to evolve to true platforms for start-ups and SMEs. Read the Embracing payments as a platform for the future of mobile money report for details.

Source:GSMA Mobile Money, 2019

Given the evolution of the digital payments ecosystem in the developing world, which now includes a plethora of actors such as aggregators, tech platforms, bank-led digital finance offerings, and fin-tech disruptors, the mobile money industry is increasingly moving towards a platform-based approach. As emphasised by the GSMA Mobile Money team, “the key question is how the mobile money business model can evolve to increase the relevance of accounts and to meet the changing needs of individuals and small businesses.” This transition towards a “payments as a platform” approach, which involves connecting consumers with third-party services across a range of industries is at the heart of this evolution, and will provide new and exciting opportunities for start-up MNO collaboration. To take advantage of this and to reduce dependence on cash, start-ups and MNOs have to continue to collaborate to drive mobile money adoption and to establish mobile money as the driver of innovative business models in emerging markets.

We would like to end this blog by thanking our grantees for participating, and most importantly our speakers Anant Nautiyal, Nika Naghavi, Bernie Akporiaye, Charles Yeboah, Roshan Lamichhane and Anjal Niraula for sharing their valuable insights.

The Ecosystem Accelerator programme is supported by the UK Department for International Development (DFID), the Australian Government, the GSMA and its members.

The GSMA Mobile for Development (M4D) Utilities programme is funded by the UK Department for International Development (DFID), USAID as part of its commitment to Scaling Off-Grid Energy Grand Challenge for Development and supported by the GSMA and its members.