As part of the analysis for our recently released report, ‘Powering Mobility: The Rise of Digital Transport in Africa‘, we took a close look at the funding landscape for African start-ups working in transport and logistics. This blog summarises the headlines from that analysis and discusses the implications.

We used data from the Africa: The Big Deal database, which tracks all tech start-up funding deals over $100,000 on the continent for originations that have their headquarters in an African country, or have their headquarters elsewhere with an African founder. As such, this data will exclude investments in companies not based on the continent or with African founders, non-tech investments in transport start-ups, and only publicly announced deals are included. Despite the caveats, these data provides insight into the innovation funding landscape on the continent and indicate where the market is headed.

2019 – 2022: The headlines

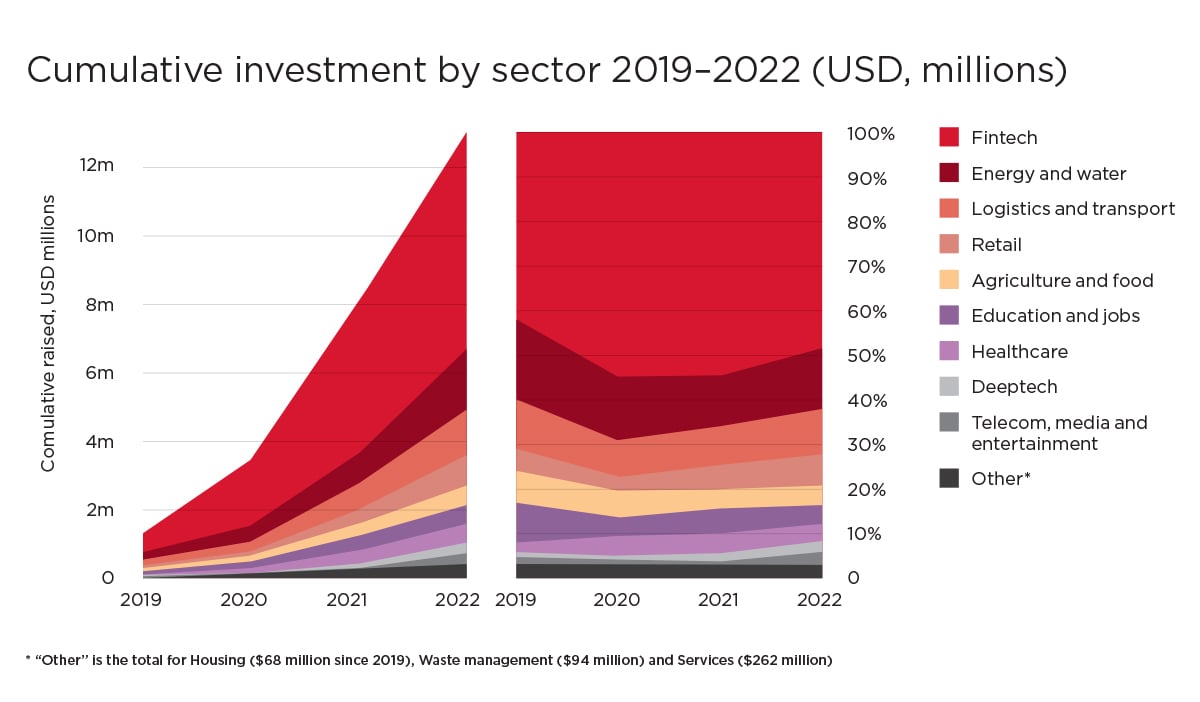

Our analysis included the four complete years of data for January, 2019 to December, 2022. In that time, there were just under $13 billion in deals across 12 key sectors. Fintech attracted the lion’s share (just over $6.2 billion). Transport & Logistics is the third largest sector by funding, with $1.4 billion in deals tracked. The figure below shows the sector funding trends for all deals tracked. Transport & Logistics compound annual growth rate (CAGR) was 78%, and 2022 saw a 38% YoY increase on the 2021 deal value.

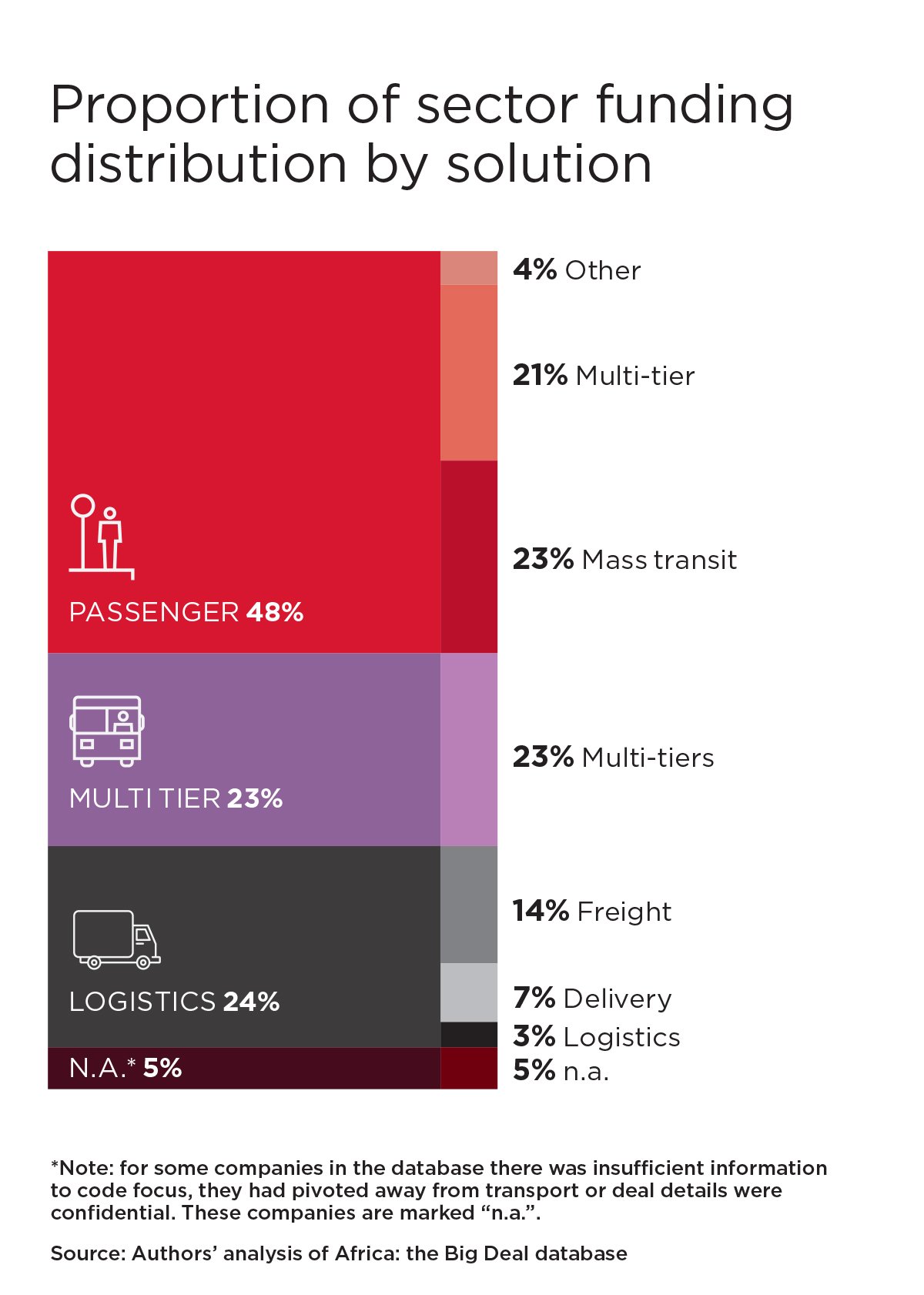

The $1.4 billion that has gone into Transport & Logistics has been channeled into 161 companies across 255 deals/funding rounds. To understand where this funding was flowing, we reviewed all companies and coded them according to their main sub-sector, the solution’s main value proposition, and if their solution includes a manufacturing or financing offer. 48% of funding has gone to companies focusing on passenger transport, while multi-tier solutions (those cutting across both transport and logistics) account for 23% of deal value, and 24% for logistics-focused solutions. Most of the funding is going to companies for which digital platforms are the main solution type. We discuss more about this trend in the report, and digital platforms in the utilities sectors in another blog.

Trends in logistics

Logistics has historically been a major break on economic development on the continent- the cost of logistics, as a percentage of GDP, is about double that in North America. This ultimately raises the costs of basic goods for the whole population, and acts as a hinderance on intra-regional trade. Only 18% of African exports are to other African countries, a figure significantly lower than other regions (it’s 58% in Asia and 68% in Europe). Established in 2018, the African Continental Free Trade Area (AfCFTA) became the world’s largest free trade area. Implementation of this entails the gradual removal of trade barriers between signatories, currently 54 of the 55 members of the African Union. The World Bank estimate that, with the removal of non-tariff barriers and trade facilitation policies, this could lift national income by an average of 7% by 2035. Many see digital as central to enabling this intra-regional trade, and the logistics sector is both an enabler and beneficiary of the AfCFTA.

“Large logistics companies have historically been too expensive for African companies to use, but we are now seeing the rise of new digital logistics companies that reduce costs and can improve the quality of services while also promoting sustainability.”

World Economic Forum

Significant funding is going to B2B logistics platforms for matching shippers to truck drivers, with tracking and reliability a key part of the value proposition. Companies like Kobo360, Trella and Lori Systems are the leaders in the field, and are those that many are hoping will support the expansion in intra-regional trade. A second major group are solutions that support e-commerce and allow for delivery tracking and warehousing solutions. There are several companies that combine physical infrastructure with digital platforms for managing the movement of goods. E-commerce penetration on the continent is at about 32% presently, so there is plenty of room to grow, and sound logistics and delivery – alongside effective payment solutions – are a key part of supporting the emergence of a sector which is likely to contribute to economic growth. You can read a summary of a GSMA roundtable at MWC Barcelona 2023 on e-commerce in Africa here.

| Solution type | Example companies | Total raised |

| B2B platforms for matching shippers to truck drivers with asset tracking and other services | Kobo360 Trella Lori Systems Naqla | $78m $54m $34m $11m |

| All-in-one warehousing and delivery | Sendy | $22m |

| B2B parcel delivery for e-commerce | Mylerz Bosta | $10m $13m |

| Platform for small shops to source FMCG | Jabu | $18m |

| Platform for food order and delivery | Elmenus | $18m |

Trends in passenger transport

The story of passenger transport is told, at least in part, by the three leading companies. Together, Moove, Swvl, and Yassir have raised close to $700 million in the last four years, close to half of the total deal value in Transport & Logistics for the period.

Ride hailing is, of course, part of the picture in mobility start-ups, and Yassir have successfully managed to expand across North Africa and into Europe and North America. Not in this analysis due to a pivot to fintech, it is also notable the MNT-Halan recently became the continent’s ninth unicorn and began life as a ride-hailing platform.

Moove’s success tells a different part of the story in ride hailing filling the need for access to vehicle financing. Moove offer this on a revenue-share basis as drivers are approved for finance only if they use the vehicle to drive on a partner ride-hailing platform. In addition, there are other digital marketplaces for second-hand and new cars that offer more traditional financing like Sylndr and Autochek.

Swvl’s success tells the story of the transport systems in many African cities. Their platform allows the booking of privately owned mass transit operating along fixed routes, as well as other B2B and B2G offerings. Their success speaks to the need for coordination in a fragmented mass-transit market, where the line between public services and private ownership is often blurry. One facet that is not captured by looking just at start-up funding is the investments in digitalising public transportation systems. Our report contains a deep dive on digitalising payments in public transport, digital solutions supporting Bus Rapid Transit (BRT) systems, and how data can be used to inform planning (see companies like Go Metro). Finally, it is encouraging to see early-stage investment in mobility start-ups looking to the manufacture of e-vehicles to the continent. It’s a fast-moving space and is seeing rapid innovation, and the recently launched Africa E-Mobility Alliance have some great resources. This sector is key to a green energy transition in transport, and as with other offerings many of these companies offer financing or ‘pay-as-you-drive’ options.

| Solution type | Example companies | Total raised (Jan 2019-Dec 2022) |

| Revenue-based vehicle financing platform suppling ride-hailing market | Moove | $266m |

| Digital platform for accessing mass transit | Swvl | $252m |

| Ride hailing | Yassir | $180m |

| Electric mobility manufacturing and supply | Max Ampersand Basi-go JET Motor Roam* | $63m $13m $12m $9m $8m |

| Marketplace for second hand vehicles | Autochek Sylndr | $17m $13m |

Q1 2023 update: A tempering

The analysis above covered the four years to the end of 2022. Beginning in 2022 and continuing into 2023 the picture is changing. It has been a bad year for the tech VC sector: The collapse of both FTX and Silicon Valley Bank significantly undermined confidence, while others underestimated the impact the global inflation spike, and subsequent interest rate hikes, would have on liquidity. While the Q1 results from the Big Deal Data were better than many may have expected, the impacts of the global slowdown on the continent are undeniable and substantial. The Transport & Logistics sector was particularly badly hit. Q1 2023 deals were 11% of the level in Q1 2022, $25 million vs $220 million. The high Q1 2022 figure can be attributed, in part, to a substantial $115 million in raises by Moove. Nonetheless, the slowdown is undeniable. It isn’t however all doom and gloom. While the current analysis largely reflects the success of the three leading companies, 2021 and 2022 saw many Series A and B rounds closing, hinting at continued growth for the sector. While raises are no doubt more challenging in the current climate, deals are nonetheless still flowing. Earlier this month, M-KOPA secured a $250 million debt/equity injection for its asset financing platform. While a winnowing of the market is likely, those who come through this winter will likely do so on sound business models and in a better position to scale.

Where and what next

The need for clean mobility solutions is clear, and the successful companies are bringing tailored offerings that speak to some of the most pressing needs in the sector: Access to finance, coordination in a fragmented sector and the need to accelerate electric mobility adoption. In logistics the focus of companies heralds the expansion/growth of e-commerce, while at the same time speaking to some of the long-standing challenges associated with facilitating regional and global trade, and accurately tracking goods to their point of delivery. The availability and adoption of the core enabling technologies underpinning these business models – IoT, digital payment, GIS services and access to connectivity – are continuing to grow despite the slowdown in investment. The emergence of tailored and digital-first models is exciting where it intersects with continent-wide transformations, such as the AfCFTA and improved cross-border road and logistics infrastructure, and where it enhances the capabilities, and generates greater freedoms, within populations. We’re not alone in this excitement, and despite the recent investment headwinds, we remain optimistic on the sector’s long-term trajectory.

The Digital Utilities programme is funded by the UK Foreign, Commonwealth & Development Office (FCDO), and supported by the GSMA and its members.