What is blockchain?

Blockchain is a digital technology that enables the secure recording and exchange of information between participants on a network. It is a form of distributed ledger technology that can be used to record transactions, manage data, and automate processes “on the chain.”

Figure 1: Blockchain in action

Source: UN Innovation Network

Blockchain technology has the following core features: security, immutability, and transparency of data and transaction records, which can solve numerous pain points for smallholder farmers and the agribusinesses that work with them, by digitalising various parts of agricultural value chains.

The GSMA Mobile for Development’s report on “Blockchain in Agriculture: Global Lessons and the Kenyan Experience”, highlights the potential of blockchain technology to support smallholder farmers and other actors in the agricultural ecosystem to address these challenges.

Smallholder farmers’ pain points across the agricultural value chain

Agricultural value chains are comprised of all actors and activities that bring an agricultural product from the field to final consumption. The main stages of the value chain are: preparation (sowing phase), cultivation (harvesting phase), storage (crop sale), and delivery (crop distribution). Smallholder farmers across LMICs contribute significantly to total global agricultural output and food security, but they face a range of challenges across the agricultural value chain that undermine their productivity. Some of their core pain points include:

- Limited access to credit, making it difficult to cover production costs and invest in growth

- Difficulty enrolling in insurance schemes, increasing vulnerability to risks such as crop failure or market shocks

- Climate variability, negatively affecting crop yields and increasing risks

- Use of poor-quality inputs, leading to reduced productivity and lower-quality produce

- Lack of sufficient and reliable market pricing, weather, and farm-level data, hindering informed decision-making across the value chain

- Absence of verified identity documents, restricting access to financial products, government support, and formal markets

Blockchain-powered solutions can play a transformative role in addressing these challenges at various stages of the value chain by improving transparency, efficiency, and trust.

Key use cases of blockchain in agriculture

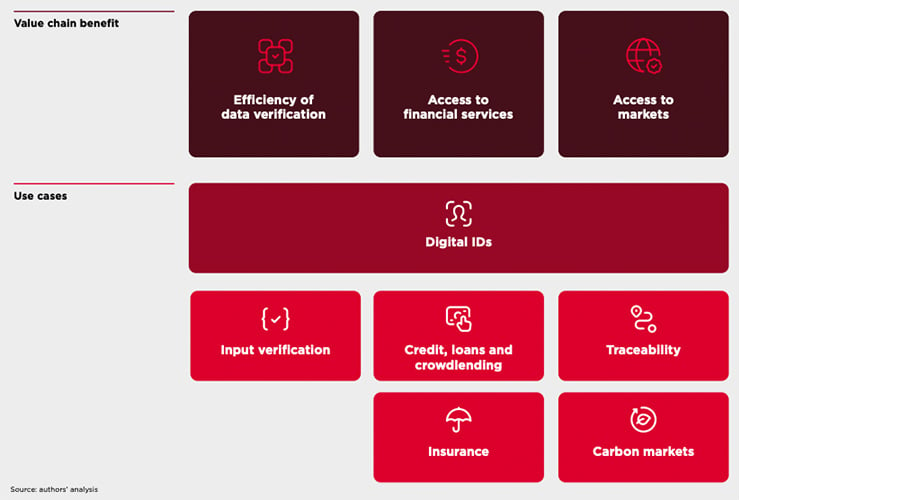

Our research identifies six key use cases of blockchain in agriculture (Figure 2), targeting different aspects of the agricultural value chain to enhance the efficiency of data verification, improve access to financial services, and expand market opportunities for smallholder farmers.

Figure 2: Key use cases for blockchain in agriculture

Source: Author’s Analysis

- 1. Digital IDs

Without access to official identification, smallholder farmers can face challenges in accessing government and financial services and formally participating in commercial agriculture supply chains. Digital IDs create a more transparent and secure way of managing farmers’ data, allowing stakeholders to confirm an individual’s identity to disburse benefits, reduce fraud, and comply with regulations. More than 850 million people around the world do not have an official ID, and at least 3.3 billion people do not have access to a government-recognised ID to securely transact online, many of whom are living in LMICs. To provide vulnerable populations with access to critical services, digital IDs offer a promising solution.

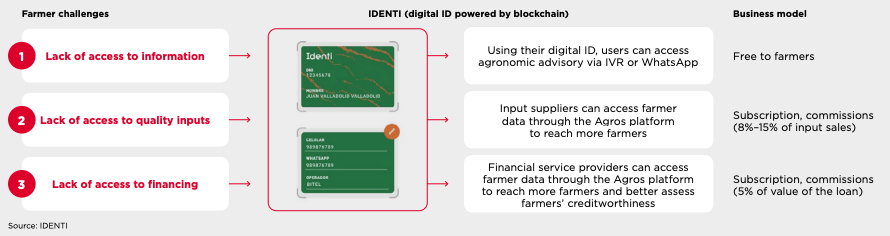

For example, Identi is a Peruvian agritech founded in 2019, and provides blockchain-based digital IDs for smallholder farmers in Peru (Figure 3). Identi supports smallholder farmers in accessing digital agri-advisory, financial services, and quality inputs by providing a reliable record of their identity and production history for service providers. At the end of 2024, there were nearly 10,000 farmers on the Identi platform, with many reporting up to a 30% increase in earnings through access to the aforementioned services, while financial service providers have reported lower origination costs and streamlined farmer vetting.

Figure 3: Identi -Blockchain powered digital identity

2. Agricultural input verification

Blockchain can facilitate verification of the quality and legitimacy of agricultural inputs from supplier to farmer. By addressing the challenge of inconsistent access to high quality inputs (such as seeds and fertiliser), it simultaneously reduces food safety risks and prevents distribution fraud. Across many LMICs, a growing number of agritech startups are beginning to develop and pilot blockchain-based input verification to bring greater transparency and traceability for agricultural input supply chains.

For example, GeoKrishi is a Nepal-based startup and a GSMA Innovation Fund alumnus; the GSMA Innovation Fund sources innovative solutions leveraging digital and emerging technologies and supports them to scale and create favourable outcomes for local communities. In partnership with the Nepal government’s Seed Quality Control Centre, GeoKrishi launched DESIS 2.0 in January 2025, which is a blockchain-powered seed certification system for rice, maize and wheat seeds. DESIS 2.0 uses blockchain to allow seed producers, government bodies, and other stakeholders to upload and verify data across all three stages of the seed certification process (Figure 4). Each seed batch is assigned a unique ID and QR code, enabling transparent tracking and allowing farmers to make informed decisions based on verifiable data on the quality and type of seed. While data regarding the impact of this solution is limited as it is recent, there has been positive feedback from stakeholders involved in the certification system.

Figure 4: DESIS 2.0 Traceability Process

Source: GeoKrishi

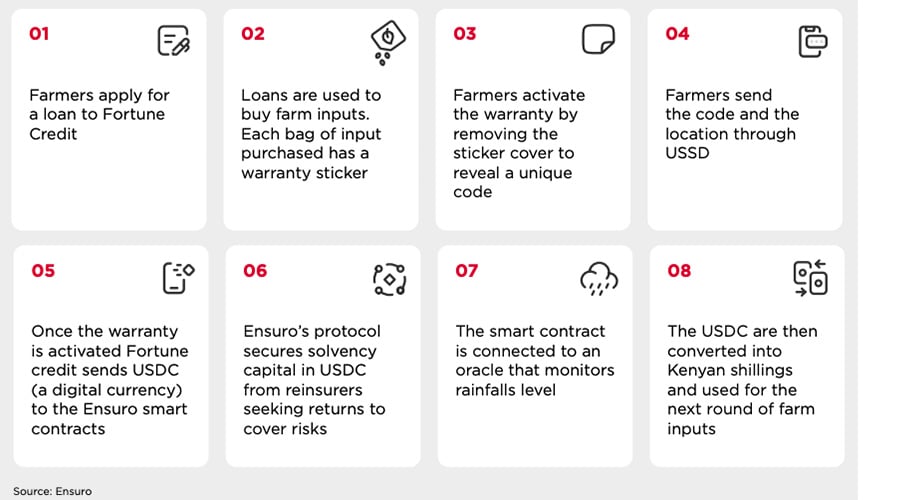

3. Credit, loans and crowdlending

With a $170 billion funding gap for smallholder farmers, access to finance remains one of their biggest challenges. Blockchain innovation can be instrumental in storing and verifying farmer records such as farmer and household data, mobile money transactions, and procurement records. This data can then be used to inform credit-scoring by financial service providers, improving farmers’ access to credit. Numerous blockchain-based financial platforms have emerged to address smallholder farmers’ access to finance in LMICs. In Kenya, startups like hiveonline and agriKOPA are providing credit and credit-scoring solutions, while groups like One Million Avocados and Project Mocha are providing smallholder farmers with access to credit through asset tokenisation, converting farmers’ physical assets into digital tokens declaring ownership.

In Latin America and Mexico, EthicHub, a crowdlending platform founded in 2017, provides financing to smallholder farmers across the coffee and cocoa value chains. Through EthicHub, people from across the globe lend small amounts of money directly to farmers, and farmers borrow from many individual lenders rather than from a traditional bank. EthicHub has created a crowd collateral system using digital tokens, acting as an insurance pool for lenders, which keeps default rates low (around 3%) and increases investor confidence. Everything is recorded on a public blockchain using smart contracts. So far, it has disbursed over $5 million in loans to over 10,000 farmers in six countries, with data showing that farmers are able to earn around 15% more for their coffee than before.

4. Traceability

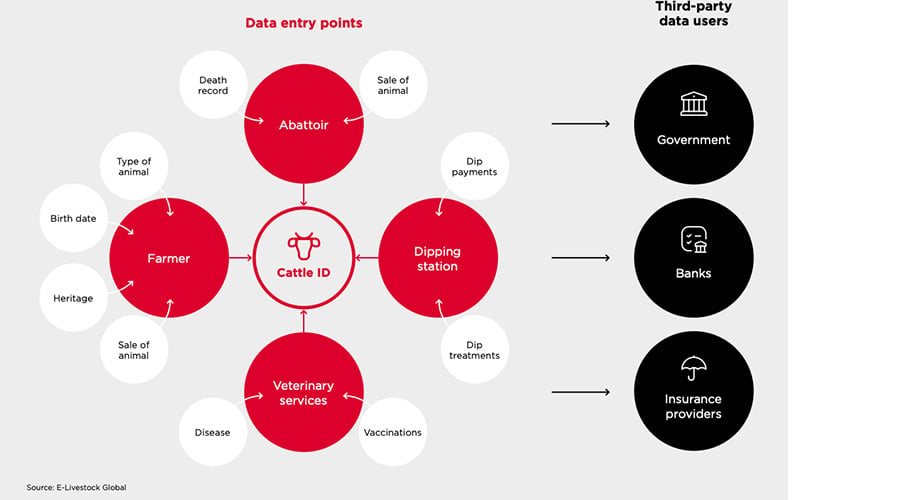

Blockchain is well-suited to support the traceability requirements of “farm-to-fork” initiatives that aim to provide transparency across the value chain due to the immutability of records on the chain, from the growth of crops to the sale of the final product. Over the past year, the need for demand-side traceability solutions has increased due to companies and suppliers wanting to establish themselves as ethical providers of premium products, as well as the introduction of regulations such as the EUDR, that require strict compliance for agricultural goods. Blockchain platform Provenance, in the US, tracks seafood and crops from farm-to-fork, ensuring, for example, that fish are caught ethically and fishers are paid fair wages. E-livestock Global, an agritech startup in Zimbabwe, uses blockchain to digitally manage livestock-related data. The platform connects farmers, governments, banks, and insurance providers (Figure 5), shares data with multiple stakeholders simultaneously and ensures regulation adherence for livestock. Because blockchain records are immutable, fraudulent activities are minimised.

Figure 5: E-Livestock Global data ecosystem

Source: E-Livestock Global

5. Insurance

Parametric insurance policies have emerged in recent years, lowering costs for insurance providers while making premiums affordable for smallholder farmers. Blockchain can make parametric insurance more efficient by automating processes and using smart contracts, significantly reducing the costs associated with verifying claims and enabling faster compensation for affected farmers. Data suggests that only four out of 54 countries in Africa offer affordable agricultural insurance products, and only 3% of farmers in Africa are insured. One example of such a product is Ensuro’s ResilientGrowth, a blockchain-powered parametric insurance product that provides smallholder farmers in Kenya with coverage against drought. Insured farmers receive automated payouts based on different drought levels which are automatically verified by weather stations and enabled through smart contracts. The platform aims to reach 20,000 farmers in the Rift Valley region of Kenya, and registration on the platform continues to grow and expand across other regions in the country.

Figure 6: ResilientGrowth Payout Process

Source: Ensuro

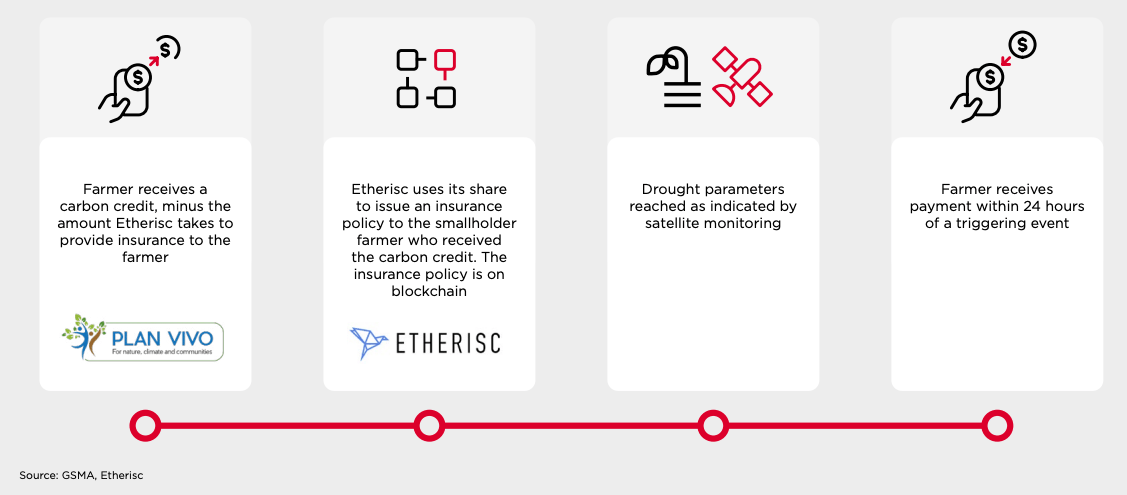

6. Carbon markets

Voluntary Carbon Markets (VCM) offer farmers the opportunity to generate additional income by participating in carbon offsetting projects and adopting more sustainable farming practices. However, VCM projects can often lack transparency due to fragmented data reporting, overestimation of CO2 impacts, limited third-party verification, and unclear arrangements on how to share benefits. Blockchain can help address these challenges by maintaining immutable records of transactions and leveraging smart contracts including carbon credits for automated execution of agreements.

Etherisc is one example that combines insurance and carbon credits. It is an open-source, decentralised insurance protocol that uses blockchain to deliver parametric crop insurance. In East Africa, Etherisc bundles insurance with carbon market participation, so that farmers adopting sustainable or climate-smart practices generate carbon credits, which are tracked and verified via blockchain. In Kenya, Etherisc integrates with M-PESA, so insurance payouts and carbon credit income are paid directly to farmers’ mobile wallets. Over 2.5 million Kenyan farmers have accessed Etherisc insurance through the platform.

Figure 7: Business model for Etherisc carbon credit programme in Uganda

Source: GSMA, Etherisc

Challenges with scaling blockchain solutions

Despite the promising use cases of blockchain in digitalising agricultural value chains, findings from this research indicate that blockchain solution providers face significant challenges in securing funding. This is partly due to the technology’s association with cryptocurrencies, which have been volatile and subject to negative media coverage and regulatory uncertainty. In addition to funding, technology-specific challenges include:

- Poor quality or inaccurate data entry

- The high cost of maintaining data and transaction records on the blockchain compared to the cloud

- The lack of on/off ramps solutions that bridge the traditional finance system with the blockchain ecosystem, which limits everyday usability and reduces the incentive to adopt blockchain-based financial products.

Recommendations for adoption and scale

Realising the opportunities blockchain offers for agriculture in LMICs requires coordination and commitment from various stakeholders involved in the agricultural ecosystem.

Governments can play a role by creating an enabling regulatory framework for products and services such as smart contracts, digital assets, and insurance. They can also help drive awareness and capacity building, and provide funding support to help advance blockchain solutions for smallholder farmers.

Blockchain innovators and startups can prioritise solutions that improve existing processes (e.g. insurance payouts, input verification and traceability). This can help improve interoperability between services, which is necessary for blockchain to remain useable and efficient for farmers. Combining blockchain with other technologies could also support blockchain innovators to better strategise their deployment of blockchain for scale.

For NGOs and donors that are actively working on blockchain-related projects, supporting shared infrastructure (weather stations and data platforms) can help reduce the costs of blockchain, thereby making it easier and more cost-efficient to scale. Lastly, by ensuring that blockchain solutions are adapted to rural smallholder farmers through local partnership models, low-data solutions and data support, and investing in building trust, digital literacy, and capacity building, donors can better drive scalability of new blockchain solutions.

As described in this blog, emerging blockchain solutions in agriculture have shown potential in improving the livelihood of smallholder farmers and actors across the agricultural value chain. To find out more about how blockchain technologies can catalyse agricultural development in LMICs, read the full report here.

The Central Insights Unit is currently funded by the UK Foreign, Commonwealth & Development Office and supported by the GSMA and its members.

{kind=link}