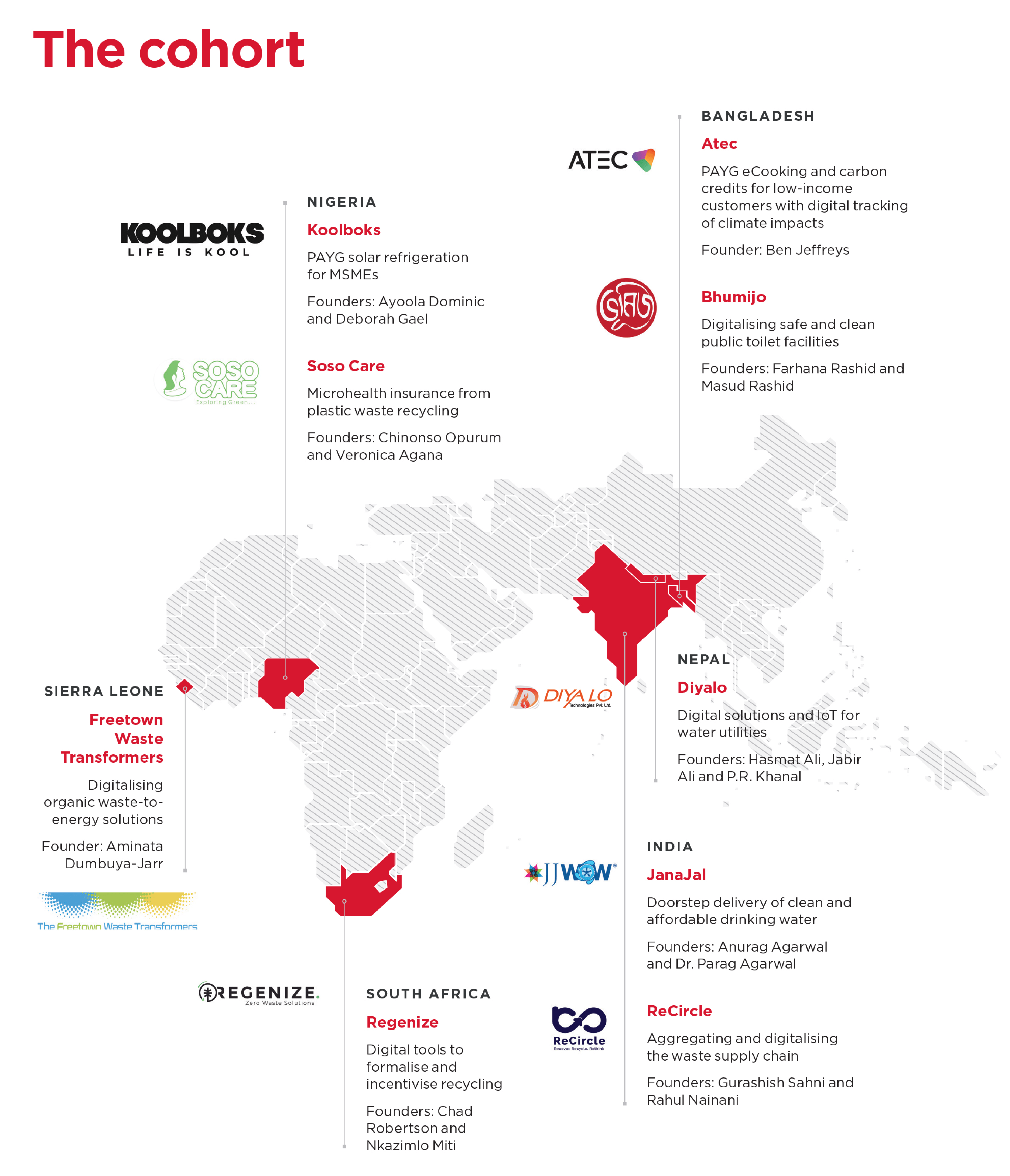

In May 2021, GSMA launched the GSMA Innovation Fund for Digital Urban Services with support from the UK Foreign, Commonwealth & Development Office (FCDO). The fund was open to start-ups and early-stage companies providing essential urban utility services who leverage digital innovations to make these services more accessible, reliable, sustainable and affordable. Successful organisations were awarded between £100,000 and £250,000 in grant funding and were provided with technical assistance. Pitches were received from 335 organisations in 43 countries across Africa, South Asia and Southeast Asia, and from these, a cohort of nine organisations were selected. This blog series summarises the key learnings from the grant period.

This blog takes stock of some of the key fundraising milestones of the nine organisations awarded grants under the GSMA Innovation Fund for Digital Urban Services, and concludes with a discussion of what this tells us about the state of climate tech finance. The figures in this blog include raises made during the grant period (Q1 2022-Q4 2023) and the nine months following, and as such only the initial stages of scaling for the cohort.

Over the grant period the nine organisations collectively raised over $11 million in follow-on funding. Comprised roughly of ~$4.5 million in debt, ~$3.5 million in debt/equity rounds, and ~$3 million in other grants and awards. Since the grant closed in Q4 2023 a further ~$13 million has been raised, bringing the follow-on funding total for the round to approximately $24 million.

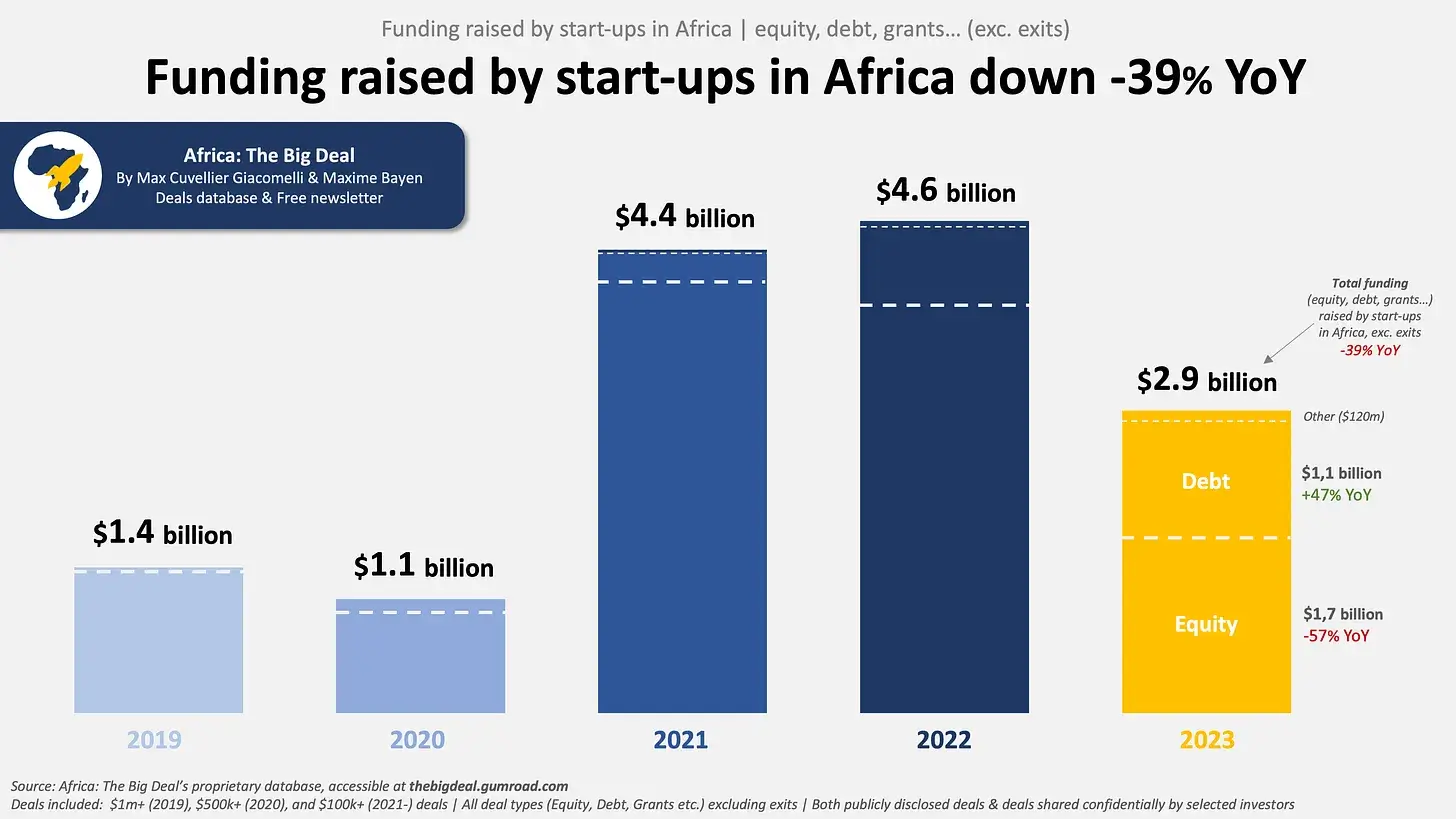

This is an impressive figure for a few reasons. First, all companies in the cohort were pre-series A or earlier at the start of the grant period. Second, and significantly, these raised took place during a prolonged ‘tech funding winter’ driven by the changing global macro-economic context post-pandemic, and that followed the collapse of FTX in November 2022 and Silicon Valley Bank in March 2023. This winter has continued to have a long tail, with H1 2024 funding to tech startups in Africa down 57% compared to H1 2023. The blog discusses the series raises, climate finance, debt and grant funding to the cohort, before discussing what these tell us about the wider state of climate tech funding in the utilities sectors.

The series raises

Three of the organisations in the cohort made significant series raises (Seed to Series A) over the grant period: ATEC, Koolboks, and ReCircle. One particularly encouraging facet of all these rounds was the mix of global and national investors, and that these included impact-orientated and more commercially focused capital. A final note here is that equity raises made within the cohort that are not public are not discussed here.

In August 2022 Koolboks had a $2.5 million seed round. This was led by Nigeria-based growth equity fund Aruwa Capital Management, who had also made an earlier equity investment. The round also included participation from Acumen and PG Impact (Verein), with All On also signing a debt deal a few months later. That seed round was focused on the initial launch and scaling in Nigeria, with some additional grants (discussed later in the blog) following hot on the heels of this seed round.

Later in the period, at the end of 2023 ReCircle closed a pre-Series A round with backing from Flipkart Ventures, Acumen, and 3i Partners. This followed an enormously successful 2022-23, which saw ReCircle nearly triple the volumes of waste processed. ReCircle have now prevented over 100,000 tonnes of plastics from being improperly managed, and operate at 270 sites across India. In September 2024 ReCircle closed a further bridge round, with funding from Venture Catalysts and Mumbai Angels, among others.

Following the grant close, ATEC made a $3.75 million Series A raise in July 2024. The round was co-led by Schneider Electric Energy Access Asia (SEEAA) and the Spark+ Africa Fund. Other investors in the round included: DRW, Save the Children Australia Impact Investment Fund, Kibo Investments and iDE. The funding will support ATEC’s scaling in South and Southeast Asia, and expansion into African markets.

Looking to the carbon markets

Two of the cohort also made moves in the carbon markets. While not large capital injections, and not counted in the figures above, these deals are significant as they open new revenue streams for the start-up pursuing them. They are also exciting as in both cases digital technologies are used to address some of the deeper challenges within the Voluntary Carbon Market.

In April 2023, ATEC signed a deal with global energy supplier ENGIE for the purchase of up to 11.5 million tonne’s worth of carbon credits. This deal was significant as it underscored the demand there for high-quality high-integrity carbon credits, and enabled ATEC to significantly lower the costs of their eCook stove for end customers. ATEC’s credits are produced using one of the few digitised methodologies used by the major carbon standards – the ‘metered and measured methodology’ – which they worked with the Modern Energy Cooking Services (MECS) programme to develop. ATECs entry to the market via Gold Standard certification was thanks to $1.3 million in pre-financing in the form of convertible notes from elea.

In September 2023 Koolboks signed a deal with Carbon Clear to generate ‘micro carbon avoidances’. Koolbok’s solution displaces the use of diesel gensets to power refrigeration, and as such prevents CO2 from entering the atmosphere, their mid-sized freezer will prevent roughly half a tonne of emissions per year. Carbon Clear, and other similar emerging standards like CavEx, have a different proposition: they only work with digitally-enabled monitoring and charge no up-front fees. Instead, they work on a revenue-share basis with the platform and the enterprise splitting the revenue as credits are sold. Additionally, the prices these credits can command are above market due to both the demonstrable social impact, and the rigorous digital monitoring in place. Encouragingly, CavEx themselves recently closed a $6 million seed round, with backing from E3 Capital and FSD Africa Investments (FSDAi).

Blended finance, concessional debt, and grants

In one of the biggest single deals in the round, Freetown Waste Transformers (FWT) and The Waste Transformers secured a $3.9 million investment from the Climate Investor Two fund (CI2). This blended finance facility mixes public and private-sector capital as well as commitments from development finance institutions. FWT’s solution is based around the deployment of biogas facilities that process organic waste and produce clean energy for off-takers, collections are managed through an app offering from FTW that the city council are also using for municipal collections. The solution requires a large up-front capital investment for the waste transforms, and in this context concessional debt and grant has an important role in the funding mix. This initial ‘pilot’ under the CI2 funding is ahead of a prospective $20 million investment opportunity in the city.

Koolboks secured the single biggest grant (with a repayable component) from Fonds français pour l’environnement mondial (FFEM). This $1.5 million deal was focused on Koolboks establishing the capacity to manufacture their freezers in Nigeria. In June 2024, this was followed by Koolboks receiving a share of a $17 million FDI from a UK-funded Manufacturing Africa programme to enhance clean energy in Nigeria. Koolboks secured a $1.6 million subsidy component from Beyond the Grid Fund for Africa (BGFA) to power their expansion in Uganda.

The first two grants signal the increased emphasis donor, and commercial, funding is placing on developing local manufacturing and jobs, a trend particularly notable in the e-mobility sector (see Norfund example also). These capacities will only become more relevant in the context of strengthening intra-regional trade within African sub-regions as well as under pan-African initiatives (AfCFTA and PAPSS).

The remaining grants across the entire cohort totalled to another roughly $1 million and were from a range of funders including corporate CSR, government bodies, foundations, and embassies. Many of these grants were to companies within the cohort that are at an earlier stage of scaling, and while the total is not as eye catching as some of the larger numbers above these grants can be vital in ensuring companies and solutions scale to the point where they are ready for more commercial capital.

What these investments tell us about the state of the sector

2023 was undoubtedly a very tough year for tech funding. Global VC deal numbers dropped to a five-year low, and total VC funding fell by roughly a third from $530 bn to $340 bn. 77% of investors active in African markets are based elsewhere than the continent, and in the context of the global slowdown much of that capital retreated. The figures for African investment mirror the global trend. Similar plunges in deal value were tracked in APAC, where deal value dropped 44% in 2022, and a further 25% in 2023.

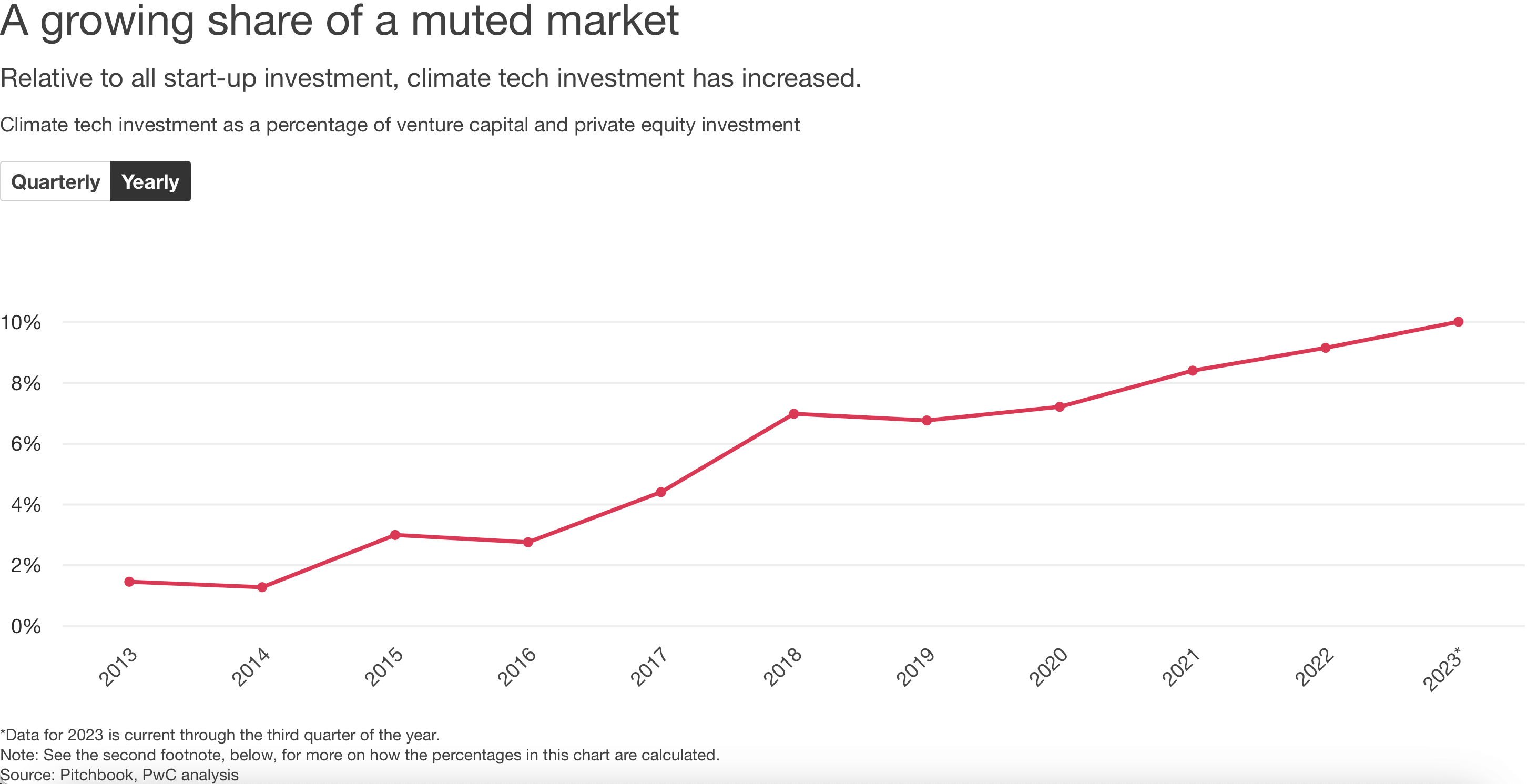

This broader context makes the raises by the cohort all that more impressive, and is a strong endorsement of both the sectors and solutions that these start-ups are working in. The grantees making significant raises during the funding winter were all climate tech solutions with a clear carbon impact. While not immune to the effects of the changing global context, the sub-sector has remained more resilient than others during this funding downturn, and climate tech increasing its share of VC investment over the period (see figure below). The more nascent sector of nature tech was also robust during the period, growing in 2023 after a fall the year before.

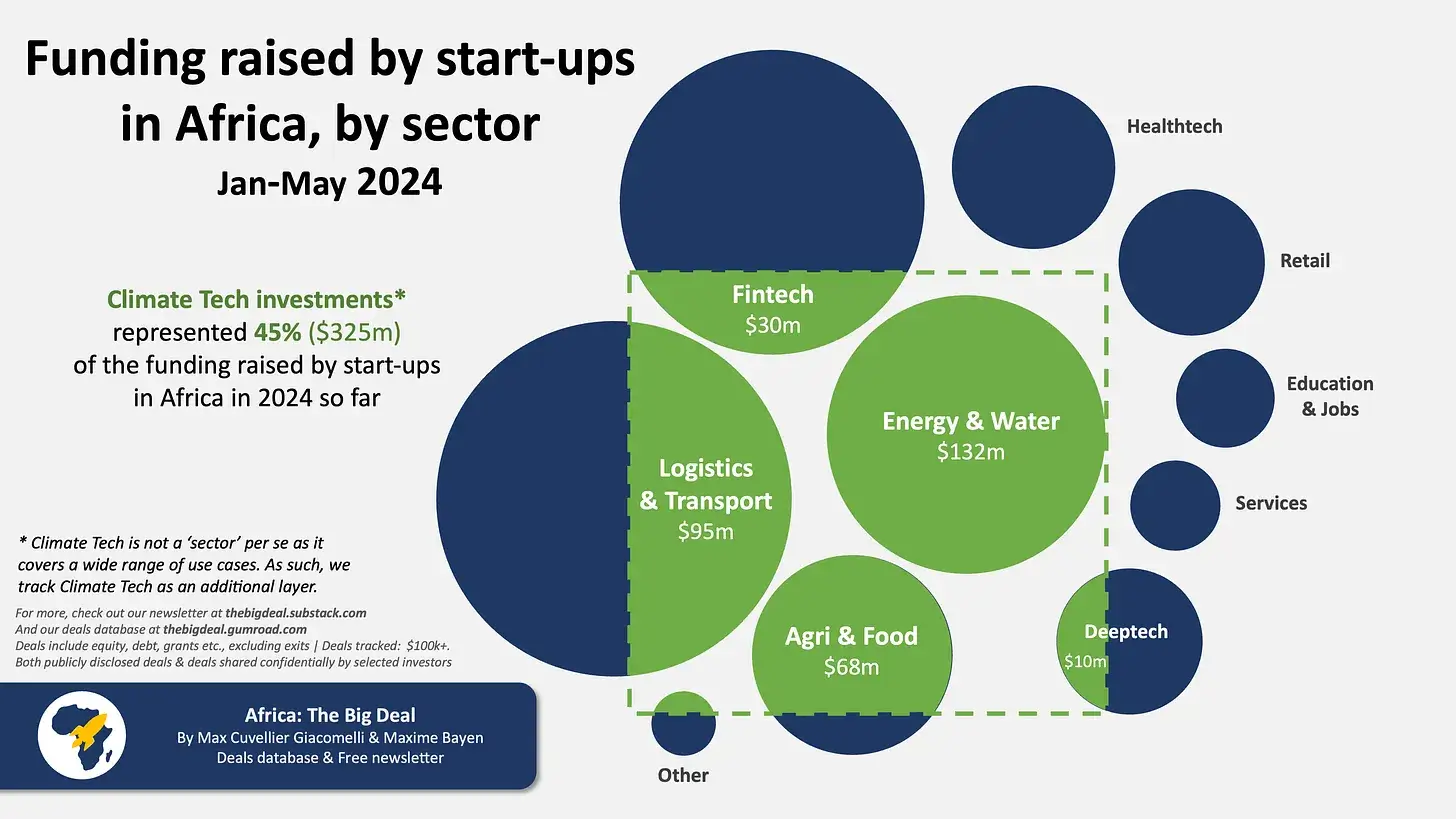

In H1 2024, climate tech investments represented 43% of all VC investment on the African continent. This was driven largely by investments in energy, productive use assets, and transport. Some of the largest deals taking the form of receivables securitized debt, a financing option growing in prominence on the continent, particularly in relation to digitally enabled pay-as-you-go offerings. In February 2024 a major solar sector industry milestone was reached when AFC and d.light repaid, in full and ahead of schedule, the senior debt of their $110 million securitisation facility. Deals such as this pave the way for institutional investors to make subsequent sizable investments in new sectors and asset classes using connected assets and digital payments.

Beyond the sector-level trends a notable feature of the funding to this cohort was the diversity of investors participating in the various funding rounds. Particularly the mix of: impact-orientated VC funders (such as Acumen), international VCs (3i Partners and PG Impact), VC funders within the markets of operation (Aruwa Capital Management and Venture Capitalists), and corporate venture funds (Schneider Electric Energy Access Asia and Flipkart Ventures). The mix and diversity of these funders is both a credit to the organisations raising, and a positive sign for the ecosystem more broadly.

Alongside these investments, the grants received by the organisations highlight the continued need of such funding alongside these other investments to support either: reaching the very poorest, developing the new capabilities or products, or launching in new markets. And as highlighted above, these can be vital in bridging the gap between initial market validation and significant equity/debt raises.

Finally, also notable is the sizable debt component in the funding mix. This high proportion links to the fact that many start-ups in the utilities space are asset-heavy, and funding for them – and for other productive use assets in e-mobility and energy – will often require a debt component as part of funding mix. While a higher debt:equity ratio can spook some investors and has balance sheet implications; debt is also a positive sign of industry maturity and can encourage more active risk management.

It has been an immense privilege for all of us at the GSMA to have had the opportunity to work with these companies in their journeys. We’re hugely excited to see where the companies go next as they join the 130 other GSMA Innovation Fund alumni. To date, within two years of the grant those organisation have collectively impacted 47 million people and raised over £660 million in follow-on funding (from grant disbursements of £25 million).

At MWC Barcelona this year the GSMA announced a five-year extension to our long-standing partnership with the UK FCDO. This new phase of the strategic partnership will focus on digital and gender inclusion, climate change mitigation, adaptation and resilience, and digital innovation in low- and middle-income countries. Recent GSMA innovation funds focused on climate resilience have also been capitalised with co-funding from SIDA. Under this partnership our innovation funding will continue and those interested in hearing about future funding rounds can register interest here.

Finally, three of the cohort – ATEC, Diyalo, and Freetown Waste Transformers – were included in the GSMA Innovation Fund for Accelerated Growth. This follow-on funding provides grant funds and additional technical assistance to these GSMA Innovation Fund alumni to support their path to scale, reach a wider user-base, and ultimately accelerate the sustainability of their solutions that make a positive impact on low-income populations.

More about the cohort

This blog is the tenth in a series covering the learnings from this innovation fund. The nine other blogs to date cover the leanings from the individual grantees and provide more detail on their solutions and impact. Learn more about them below.

Solar-Powered Cooling Solutions: Koolboks freezers in Nigeria

Building a national circular supply chain platform – ReCircle’s ClimaOne platform in India

IoT quality assured water delivered to the doorstep: JanaJal in India

Electrifying clean cooking – ATEC eCook stoves in Bangladesh

Health insurance through plastics recycling – Soso Care’s model in Nigeria

ERP and IoT solutions for water providers – Diyalo in Nepal

Digitising waste collection: Freetown Waste Transformers’ DortiBox app in Sierra Leone

Incentivising recycling through a virtual currency – Regenize in South Africa

Digitalising public toilets – Bhumijo’s affordable smart toilets in Bangladesh

The GSMA’s work on digital technologies and innovative finance models for start-ups

You can read more about the GSMA’s work on innovative financing instruments in the recently published GSMA report ‘Digitalising Innovative Finance: Emerging instruments for early-stage innovators in low- and middle-income countries’, published alongside a shorter guide for start-ups. That report takes stock of the role digital technologies are playing in crowding in private sector capital through innovative financing mechanisms to social enterprises in low- and middle-income countries. It focuses on how digital technologies enable new structures for combining commercial and impact-oriented capital in ways that help scale innovative utility service delivery models aimed at closing service gaps and addressing climate change. It also highlights how these instruments can help start-ups in LMICs overcome common challenges associated with foreign exchange fluctuations, hardware financing, and the high cost of capital for climate-tech innovations in LMICs.

For more information, watch the webinar recordings below where we cover some of the key findings.

| Digitalising Innovative Finance: Carbon credits and results-based financing | Digitalising Innovative Finance: Receivables financing and revenue-share |

This initiative is currently funded by UK International Development from the UK Government and is supported by the GSMA and its members.