Cities are vibrant centres of innovation and opportunity, driving economic growth, cultural exchange, and improved quality of life. Today, nearly 60% of the global population resides in cities, a figure anticipated to reach close to 70% by 2050. Although cities are a global economic engine contributing over 80% of the world’s GDP, they are also responsible for 70% of global GHG emissions. These factors make decarbonisation of cities necessary, and crucial to achieving the net-zero goals.

Digital solutions provide cities with innovative ideas to tackle both current and future challenges on adaptation, mitigation and resilience by achieving economies of scale, reducing infrastructure needs, and unlocking new opportunities for growth and sustainability. Through innovative approaches to governance, public investment, public-private partnerships, and financial incentives, municipalities and utility service providers are adopting digital innovations to improve services and meet the growing needs of urban populations.

The role of IoT in smart cities and smart grid solutions

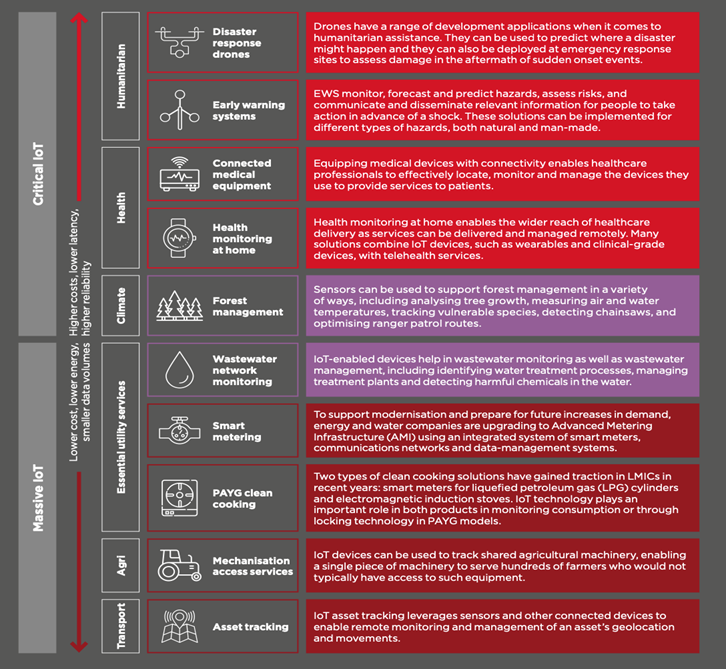

IoT in smart cities holds huge potential for either improving services or developing completely new ones. Key applications of IoT in cities include smart transportation – traffic optimisation and real-time transit updates, environmental monitoring – air quality, waste and water management, energy management – smart grids and renewable integration, public safety – surveillance and emergency response, and smart buildings – energy-efficient controls. Figure 1 below lists a few IoT use cases for development and climate action.

Figure 1: IoT Use Cases

Source: IoT for Development: Use cases delivering impact

GSMA estimates that the total number of IoT connections will more than double between 2021 and 2030, reaching 37.4 billion with utility sector deployments overtaking consumer IoT by the middle of the decade to become the market driver.

For grids, IoT-enabled solutions can improve stability by enabling seamless communication between energy producers and consumers. Sensors and smart devices embedded in the grid can monitor energy production, consumption, and system performance, allowing utilities to anticipate demand fluctuations, prevent overloads, and react quickly to outages or faults. Predictive maintenance powered by IoT can reduce downtime, optimise performance, and ensure overall grid reliability.

The role of smart meters

A critical component of this ecosystem is the smart meter. The smart meter technology has evolved over time from basic AMR (Automatic Meter Reading) to advanced AMI (Advanced Metering Infrastructure), highlighting increasing functionality such as integrated service switching, time-based rates, remote meter programming, and home are network interfaces. This allows for more sophisticated uses cases benefitting both utilities and consumers such as load forecasting, demand-side management, strategic marketing, and power procurement.

Figure 2: Evolution of metering capabilities

Source: World Bank (2019), Can Utilities Realise the Benefits of AMI Infrastructure?

By the end of 2023, utility service providers globally are projected to have installed over 1.06 billion smart meters for electricity, gas, and water. North America leads in smart electricity meter adoption (76% market penetration), followed by the APAC region driven by nationwide deployments in China and Japan (49% market penetration), and Europe, where adoption differs greatly by country (47% market penetration). While North America, Europe, and East Asia have mature markets for smart meters; South Asia, Latin America, and Africa represent a high-growth potential.

The Revamped Distribution Sector Scheme (RDSS), introduced by the Government of India in 2021, represents one of the world’s most ambitious smart meter initiatives, aiming to replace 250 million conventional meters by 2026. While India has made some progress, the country has only deployed 16 million smart meters (about 7% of the target), and several implementation challenges remain.

One of the challenges is convening the entire cross-sectoral ecosystem of stakeholders required for successful large-scale smart meter implementations, and avoiding siloed approaches:

- At the heart of smart metering are the consumers – residential, commercial, and industrial users of energy resources who interact with smart meters to manage their energy consumption.

- Distribution Companies (DISCOMs) are charged with the distribution of electricity and are key players in deploying smart meters to consumers and managing grid stability.

- Mobile operators provide the communication infrastructure (NB-IoT, LTE-M) that allows smart meters to transmit data between consumers and utility providers. The meter manufacturers design and produce smart meters with IoT capabilities, enabling real-time data transmission and monitoring.

- Meter manufacturers play a crucial role in designing and producing reliable, secure, and accurate smart meters that meet industry standards. They also support utilities by providing technical expertise, maintenance, and upgrades to ensure seamless integration with grid management systems.

- The national government sets the regulations and standards for smart meter implementation, ensuring security, data privacy, and grid efficiency.

- State and local governments provide permits and authorisation for project implementation.

- Finally, the start-ups/tech innovators develop advanced technologies such as AI-driven analytics, demand response solutions, and grid optimisation tools that enhance the functionality of smart meters and grids.

Given the complexity of the network of players in the ecosystem, it becomes imperative that all parties are aligned on the key objectives, ambitions, and interoperability protocols of the smart metering programme.

In this context, GSMA, in partnership with Climate Collective hosted the Digital Urban Utility Forum (DUUF) to discuss challenges and opportunities in scaling smart metering in India. The DUUF brought together key stakeholders, including mobile operators, policymakers, meter manufacturers, DISCOMs, and smart grid start-ups, to discuss the path forward for India’s smart metering and grid management initiatives. This blog summarises insights that emerged from the discussions.

Challenges and opportunities for mobile operators in India’s smart grid ecosystem

Mobile operators have a significant opportunity to further integrate into the smart meter ecosystem, enabling a more connected and efficient energy landscape. While challenges exist, such as addressing ‘Right of Way’ (provision of a legal right, to pass along a specific route through grounds or property belonging to another) for meter installations, these also open avenues for mobile operators to collaborate with local authorities to streamline access and expand network infrastructure. Network interoperability and legacy systems present hurdles, but they also create demand for innovative solutions that allow for seamless communication between traditional systems and smart meters, enhancing operators’ roles in modernising utilities.

- Standardisation and certification of communication modules within smart meters present an opportunity for operators to lead industry standards, ensuring robust and reliable connectivity and minimising issues like signal loss or frequent network switching. The adoption of e-SIMs for smart meters, paired with enhanced network interoperability across telecom providers, can solidify mobile operators’ role in facilitating consistent connectivity across various regions. The Telecom Regulatory Authority of India’s (TRAI consultation paper on Issues Related to Critical Services in the M2M Sector, and Transfer of Ownership of M2M SIMs provides a strategic framework, presenting operators a chance to shape regulations that support resilient smart metering networks under the RDSS.

- Operators can also capitalise on the need for preventive maintenance, offering services that enhance fault detection and network diagnostics, which help identify whether issues stem from network coverage or meter functionality. This proactive approach minimises repair costs and enhances customer satisfaction, with operators positioned as essential partners in maintaining uninterrupted smart meter services.

- Lastly, although NB-IoT coverage remains a challenge, especially in rural areas, it also offers an opportunity to leverage fallback networks like 2G and 3G, ensuring reliable coverage where NB-IoT is unavailable. By optimising network resources to manage congestion during peak transmission times, operators can improve the efficiency of real-time updates and utility alerts, solidifying their role as key enablers in the digital transformation of utilities.

Lessons from AMI rollouts across the world

- Globally, the adoption of smart meters is primarily driven by the need for enhanced revenue collection, reliability improvements, integration of renewable energy, real-time data exchange, and opportunities for new products and services. Institutional capacity, effective procurement and technology acquisition, progressive regulation with a focus on interoperability and the standardisation of communication protocols, as well as comprehensive customer engagement have been key factors for the long-term success of smart meter deployments worldwide.

- France’s Linky program offers valuable insights, particularly in cybersecurity, service reliability, and consumer trust. Linky’s robust cybersecurity framework, shaped by collaboration with France’s ANSSI (French Cybersecurity Agency) and adherence to General Data Protection Regulation, ensured strong data protection and transparent data practices, building consumer confidence. Its high service standards for uptime, accuracy, and fault resolution, backed by preventive maintenance and specific Service Level Agreements (SLAs), enhanced operational reliability. Linky’s scalability and collaborative approach across utilities, and consumers enabled shared best practices that helped foster public understanding and smoother adoption.

- Landis+Gyr’s smart meter programs in East Asia reveal key strategies for successful deployment: partnering with local utilities to meet specific regional needs, prioritising technological innovation with interoperable meters like the E570; adhering to regional regulations and standards; and engaging consumers through transparent communication to foster acceptance. These elements collectively support effective deployment, operational efficiency, and user satisfaction in smart meter initiatives.

Early insights from deployments in India

- GoI data shows that over 222 million smart meter tenders are approved, of which 115 million smart meter contracts are awarded, but only 16 million meters (7%) are deployed. The discussion highlighted the crucial role that cities, local governments, and the Ministry of Urban Affairs must play in smart meter rollouts, given their potential to drive implementation, enhance citizen engagement, and connect smart metering to broader smart city initiatives. This aligns with India’s Smart Cities Mission, where integrated infrastructure projects depend heavily on reliable energy management, supported by smart metering.

- A recurring theme during the forum was the importance of breaking down silos within both government and the private sector to foster cross-sectoral collaboration. Engaging multiple ministries and regulatory bodies can drive unified progress, particularly when cross-cutting issues such as energy, and urban development converge – for instance when it comes to use cases like e-mobility a sector which is set to grow rapidly over the coming years. Another significant barrier identified was the hardware shortage in the metering industry, which has hampered implementation timelines. Addressing this could involve boosting domestic production capacity or easing import restrictions, providing a pathway to accelerate deployments.

- In India, interoperability across hardware, network, and application layers is fundamental to prevent vendor lock-in and ensure seamless data exchange. Therefore, there is a need for standardising communication between smart meters and Head-End Systems (HES) to allow flexible meter replacements without changing underlying system infrastructure. A solution proposed by the India Smart Grid Forum is the implementation of a single Meter Data Management System (MDM) for each DISCOM to reduce costs, streamline operations, and improve data integration across billing and management applications. A study undertaken by GIZ-Accenture, highlights that the Indian smart meter ecosystem currently lacks support for dual communication systems, which would enable reliable data transfer across varying geographies. Dual technology use is suggested to address regional connectivity challenges starting with setting up technical standards, increasing testing capacities, and incorporating universal HES protocols. This includes a comprehensive approach to network and application-level interoperability to ensure a modular AMI system.

- Time-of-Day (ToD) tariffs comprising separate tariffs for peak hours, solar hours and normal hours send price signals to consumers to manage their load in accordance with the tariff. As ToD tariffs are being rolled out in India, the need for advanced data analytics capabilities, reliable data management and storage solutions will likely increase. It is also important that mobile operators have access to diagnostic data such as battery status, memory status, communication module functionality, log of power outages and restoration times. Having access to more data can enable predictive maintenance, reducing the need for in-person visits to address faulty meters, thus improving compliance with the SLAs. The utilisation of initiatives like India’s Universal Service Obligation Fund (USOF) and Gati Shakti can help improve digital infrastructure, and enable efficient deployment, especially in remote areas.

From smart meters to smart grids and smart cities -the role of start-ups and private sector innovators

Smart meters serve as the foundation of several innovative use cases that change how DISCOMs and customers can interact and build on broader opportunities in India’s growing smart cities ecosystem. Start-ups are playing a vital role in fostering collaborative innovation, particularly in areas like AI-driven analytics, demand forecasting, and load management:

- Trillectric is working with DISCOMS & demand response aggregators using both hardware & data infrastructure for distributed renewable energy asset management. Flock Energy has built data-as-a-service platform which uses advanced analytics to disaggregate data, providing valuable insights into energy consumption patterns. Bharat Smart Services has built an Al-powered Optical Character Recognition platform that ensures accurate meter readings for precise billing. These insights help utilities detect inefficiencies, predict demand peaks, and optimise usage. TekUncorked’s low voltage IoT platform combines IoT, AI, and cloud services to monitor and predict grid performance, addressing inefficiencies, outages, and maintenance issues in real-time. The company also supports demand forecasting, load management, and asset monitoring.

- FIDE’s approach to leveraging open networks, like the Beckn Protocol, to address climate change, highlighted interesting opportunities. FIDE’s open network approach is built to minimise coordination costs and enhance transparency, fostering trust among participants. The decentralised, interoperable design supports low-cost discovery and fulfilment of resources, makes it easier to mobilise climate solutions. The Unified Energy Interface (UEI), a standardised digital framework designed to integrate and manage energy systems uses open network to enable transactions between digital energy system such as EV charging, battery monetisation, P2P energy sharing. Pulse Energy, Sheru, and Trillectric are a few start-ups already building solutions on UEI.

Start-up and public sector partnerships are becoming essential in advancing digital utilities and infrastructure. A key goal of the GSMA Digital Utilities Programme is to foster Business-to-Government (B2G) collaborations that leverage innovative solutions from start-ups for public service improvement. By building these B2G partnerships, our programme aims to address infrastructure challenges, extend digital services, and increase efficiency in utility sectors, especially in low- and middle-income countries (LMICs). Our public-private partnership toolkit provides structured guidance to facilitate these collaborations, aiming to maximise societal impact through scalable public-private innovation.

Conclusion

The growth of the IoT market in India, combined with ambitious initiatives like the RDSS, underscores the importance of smart metering for energy efficiency and grid stability. However, challenges remain, particularly in ensuring consistent connectivity, interoperability, data analytics capabilities, implementing relevant use cases, managing high data volumes, and addressing community concerns. Innovations from start-ups and collaborations between telecom operators, utilities, and regulators can unlock new opportunities through advanced analytics and AI-driven solutions. A major trend that will define the decade is that enterprise IoT, which includes many utility sector deployments, will overtake consumer IoT, doubling total IoT connections between 2020 to 2030. Smart metering is a core component of smart cities, with both gas and water supply in a similar position to benefit from smart meter deployments. Many countries that have a high penetration in smart meter deployments are starting to develop, implement, and test several use cases that are commonly referred to as the transition to AMI 2.0. This includes use cases such as digital twins, network-based GIS & ADMS integration, demand response/demand-side management, and distributed generation.

This forum provided a platform to facilitate knowledge sharing and partnership building. It showcased the role of mobile operators in India’s smart meter ecosystem, learnings from global deployments, insights from early projects across different states in India and the role of start-ups and private sector innovators in building use cases that leverage smart meter deployment to benefit consumers, DISCOMs, and cities.

Over the past three years, our programme has hosted several forums across cities in Africa and Asia, working alongside local partners to bring together relevant public and private sector stakeholders aiming to leverage digital innovation to improve urban service provision. Insights from our previous forums in Freetown, Kigali, Lagos, Kathmandu, and Islamabad can be found here. We look forward to continuing our engagements and support partnerships in these markets and are open to exploring partnerships to host similar forums in other cities. As this forum in Delhi highlighted once again, cross-sectoral collaboration and public-private partnerships are critical to make essential urban utility services in LMICs more reliable, affordable, safe, and sustainable.

Next steps

- We will continue to support partnerships among different stakeholders to drive the smart cities agenda. We aim to develop recommendations through continued stakeholder engagement that can drive a more enabling environment, sharing best practices and learnings.

- We are conducting a research piece to understand the role of mobile operators in delivering smart city solutions focussing partly on the Indian sub-continent.We aim to understand the addressable market for mobile operators in key markets and regions (including India), and to review key mobile operator strategies and engagement. The study will have a heavy focus on centralised utility services (especially in energy, water, and transport), the large scale IoT deployments that can be associated with these, as well as the supporting data and analytics offerings.

- We aim to explore the role of digital public infrastructure and open networks (such as UEI) in smart city solutions.

- Lastly, we look forward to continuing to fund startups working on smart city solutions through our GSMA Innovation Fund.

We would like to thank our partners, session moderators, and all the attendees for their time and contribution and hope the forum spurred the conversation on the critical role of digital innovation and partnerships in improving smart meter deployments in India. For any queries, please reach out to us here.

This initiative is currently funded by UK International Development from the UK Government and is supported by the GSMA and its members.