On the eve of COP30 in Brazil and on the occasion of World Cities Day 2025, this blog takes stock of some of our recent research on digital adoption in cities. It looks across city contexts, from large-scale smart city IoT deployments in megacities to new city projects as well as the start-ups working in rapidly growing intermediary cities.

Home to the majority of the world’s population and centres of economic activity, cities account for the bulk of GDP, tax receipts, and emissions in most countries. The world’s largest 3,000 cities account for 67% of global GDP, and the World Bank estimates that the total urban share of global GDP may be as high as 80%. With this economic footprint comes significant emissions, with the IPCC estimating that cities accounted for 67%-72% of global emissions in 2020. The vast majority of these emissions – 84% – are generated in cities in high and upper-middle income countries, with low and lower-middle income countries generating only 14% of urban emissions despite housing a third of the urban population. The cities in lower income countries are most exposed to the risks of climate change, whilst contributing the least the problem. Additionally, it is these cities, and notably smaller cities of less than a million that are set to account for a significant proportion of the growth of the urban population. The population of African cities is set to double to 2050, accounting for approximately a third of global urban growth over the period.

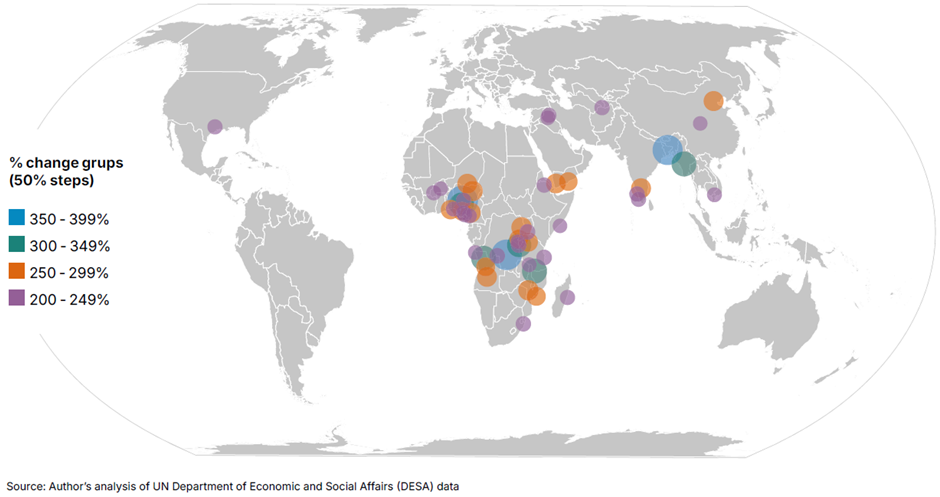

Figure 1: The world’s 50 fastest growing cities 2010-2030

Key impact areas for digitalisation

While of course not a panacea, there are some priority areas in which digital technologies can make an important contribution to both climate mitigation and adaptation; tied to the essential services on which thriving cities are built: energy, water, waste management, and transport.

In our review of smart city IoT deployments in eight focus countries we found that, on average, smart metering accounts for roughly half of all devices at present. In energy, advanced metering infrastructure is a core component of smarter grid management and demand responsive pricing; critical foundations for renewables integration. Electric mobility is another core area of focus, with digital technologies enabling digitally monitored pay-as-you-go and leasing models and enabling the tracking of distributed assets (batteries and vehicles).

Many of the key opportunities for digital innovation can be found in the ventures already operating and the underlying funding trends. Between 2019 and 2024, African Climate Tech start-ups raised a combined total of $4.3 billion, making it the second largest sector after fintech and accounting for just under a quarter of all funding to tech startups in Africa. Energy, and decentralised energy in particular, represented the largest share of this funding.

The GSMA Innovation Fund for Digital Urban Services

In May 2021, GSMA launched the GSMA Innovation Fund for Digital Urban Services with support from the UK FCDO. The fund was open to start-ups and early-stage companies providing essential urban utility services who leverage digital innovations to make these services more accessible, reliable, sustainable and affordable.

Pitches were received from 335 orgs in 43 countries, from which a cohort of nine was selected. Additionally, three organisations benefited from follow-on funding under the Accelerated Growth Cohort. The cohort collectively raised over $24 million within one year of grant close in follow-on funding. In 2025, two organisations made further substantial series raises to support their scaling: in September 2025 Koolboks – a solar refrigeration startup – closed a $11m Series A round to develop their manufacturing capacity in Nigeria and scale regionally; and ATEC – a clean energy startup focused on electric cooking and biogas – closed a $15.5m series raise to scale their clean cooking solution in African and Asian markets.

Mobile network operators are central to delivering these solutions, particularly in LMICs where rapid digital adoption is driving faster deployments and scale. Major technological changes have shifted the bounds of what is possible for urban solutions, notably, 5G and network slicing, Low Power Wide Area (LPWA) connectivity, digital payment platforms and developments in artificial intelligence (AI).

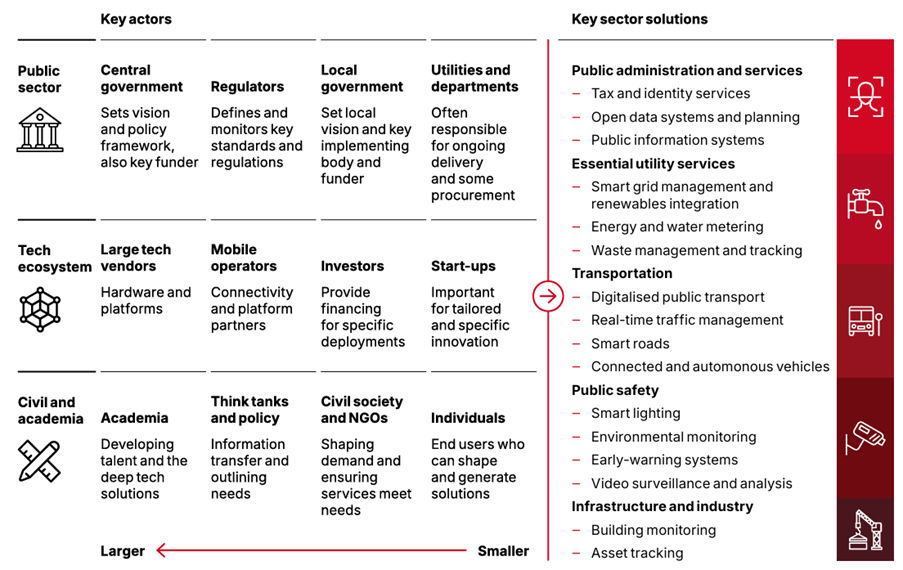

Figure 2: Key smart actors and use cases

A decade of devices

While the potential of digital solutions has long been touted, the policy foundations for smart city implementation have only emerged recently and in many countries – particularly LMICs – they are still taking shape. Smart city objectives are commonly embedded across national urbanisation plans, digital transformation agendas and national development plans. In a UN survey of 250 municipalities, 44% had a dedicated city-level plan, with these notably more prevalent in higher income and Asian countries. Additionally, strong national programmes, such as the Smart Cities Mission in India, have been key in driving progress. Beyond financial resources, these programmes provide a clear structure for implementation, enabling public private collaboration and the creation of centres of expertise within municipalities.

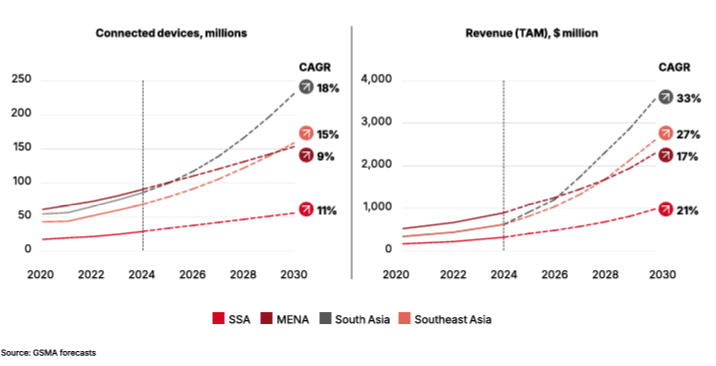

In June the Digital Utilities programmes published the ‘Digital Foundations: The Path to People-Centred Smart Cities’. The report explores the trends shaping smart city deployments across Sub-Saharan Africa, South and Southeast Asia. The opportunity for mobile operators is quantified through total addressable market forecasts for eight countries and across regions. By 2030, utility solutions will account for nearly 30% of IoT connections across the focus regions and between 2020 and 2024, smart city IoT connections increased from 173 to 271 million – increasing another 222 million to 2030.

Figure 3: IoT devices and revenues from smart city solutions, by region

Old challenges, new cities

A key theme in our recent urban research has been to draw attention to three broad modes of digital adoption in cities. The first is the large-scale deployment of digital infrastructure in large and mega-cities, supported by national programmes. A key exemplar of this is India’s Revamped Distribution Sector Scheme (RDSS), which represents one of the world’s most ambitious smart meter initiatives, aiming to replace 250 million conventional meters by 2026. In Nigeria, the Presidential Metering Initiative is a key energy reform initiative and aims to deploy 5 million meters by 2027. These centrally funded programmes often focus on larger cities – and in both water and energy, generally have the same core aims of reducing technical and commercial losses, enhancing revenue collection for cash-strapped utilities and seek to build a ‘virtuous cycle’ of service improvement.

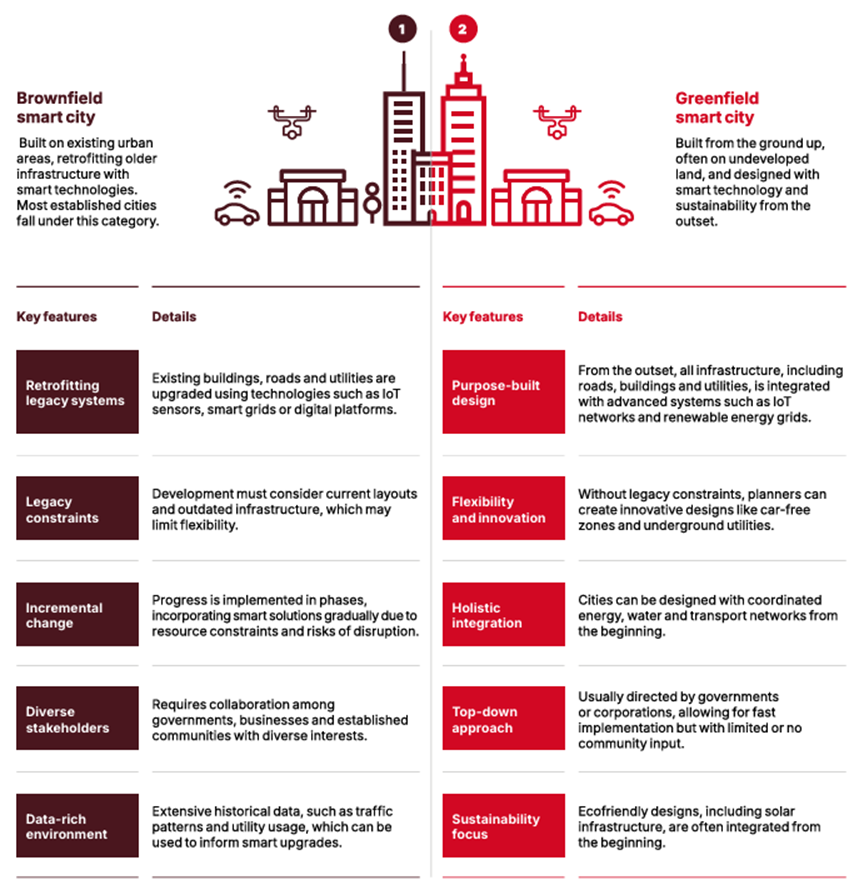

Second is a renewed focus on new city development globally. Between 2000 and 2020, 159 new city projects were launched worldwide, compared to 126 between 1945 to 1999. In many cases these new cities are focal points for smart city implementation, as retrofitting infrastructure and service provision in existing cities can be up to three times more expensive than planning for infrastructure in advance. Many of these new cities are being developed on greenfield sites adjacent to existing economic or administrative centres, with the goal of circumventing the structural challenges faced by older urban areas. Notable new city projects include: Prospera in Honduras, Nkwashi in Zambia, Itana (formerly Talent City) in Nigeria, Konza Technopolis in Kenya, Kigali Innovation City in Rwanda and GIFT city in India, as well as new capitals in Egypt (New Administrative Capita) and Indonesia (Nusantara). While these cities often serve as focus points for FDI and can serve as centres of growth, they also carry a risk of becoming high-cost, high-tech, elite enclaves detached from wider national development challenges.

Third is the set of fast-growing intermediary cities of under one million people. While megacities, capitals and new city projects are prone to grabbing headlines and policy attention; cities of under one million are home to 60% of the urban population and are set to account for a significant proportion of the growth in the urban population – particularly in African countries. These cities face a more challenging policy environment than their larger counterparts. With a more limited tax base and different forms of governance than large cities, their policy autonomy and fiscal freedom is often limited. Yet, these cities sit between the complexity of national capitals and the small-scale limitations of rural areas, have critical services gaps and represent a significant serviceable market makes them an important locus for testing context-specific technology and business models. Our recent report ‘Priming Urban Development: Digital innovation in East Africa’s intermediary cities’ explores exactly this potential through nine city case studies in Rwanda, Kenya, and Uganda.

Figure 4: Key features of greenfield and brownfield developments

Belém and beyond

On the 10th and 11th of November the world will gather at COP30 to discuss adaptation in cities including infrastructure, water, waste, local governments, the circular economy, technology and Artificial Intelligence. While nuance is often a lot to ask of such events, our recent research points to the importance of approaching digital adoption in cities through context-specific lenses that centre solving the challenges populations face. Similarly, building the ecosystems needed for these solutions to emerge and be adopted at scale can rarely be implemented through only top-down approaches. You can find more information on our past innovation funding and research on cities on the GSMA Digital Utilities webpage.

This initiative is currently funded by UK International Development from the UK government and by the Swedish International Development Cooperation Agency (Sida) and is supported by the GSMA and its members.