Mobile connectivity is vital for people and businesses across Africa, providing access to critical information, services, and income-generating opportunities. Disruptions in connectivity have widespread impacts on households and economies across the continent.

Mobile towers owned and operated by mobile operators and tower companies are fundamental to providing this connectivity. While the power requirements of a mobile tower depend on what cells the tower supports, and on what frequencies, mobile towers in general depend on reliable and affordable energy to provide constant connectivity. Mobile tower networks are unique commercial end-users of energy: they are highly distributed with up to thousands of base stations per country.

Across Africa, access to reliable, affordable, and sustainable energy is one of the key challenges facing mobile operators. For instance, in Nigeria, mobile operators and tower companies are reported to purchase and transport over 40 million liters of diesel per month to operate diesel generators at tower sites due to recurrent grid outages and lacking energy access. The cost of buying and purchasing diesel can amount to 30-60% of total operational expenditure of some operators in the region. It is both a commercial and a climate imperative for mobile operators and tower companies to address their energy challenges and find more sustainable, cost-effective alternatives.

This blog outlines some of the key energy access challenges facing business and households in Africa, discusses the specific implications of these energy challenges for mobile operators and tower companies, and highlights some scalable renewable energy solutions such as energy-as-a-service solutions and anchor-business-community models for towers located in off-grid and weak-grid areas across Africa.

The energy landscape in African markets

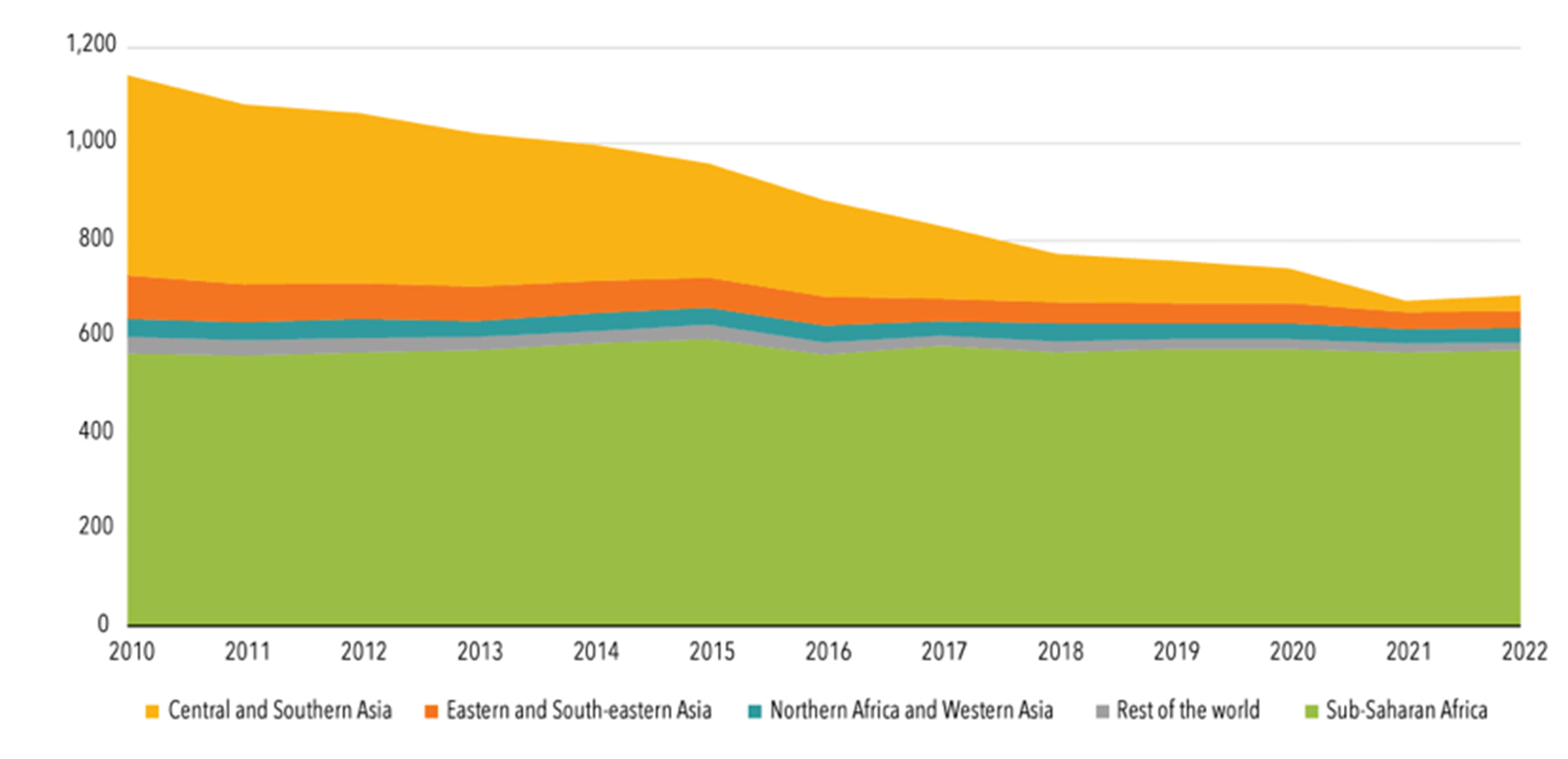

Sub-Saharan Africa accounts for over 80% of the global population without energy access and 18 out of 20 countries globally with the largest number of people living without electricity (see Figure 1). Across the region, there are significant differences when it comes to progress on energy access. While some countries such as Ghana, Kenya and Rwanda have made significant progress over the last decade and are on track to achieve universal energy access (SDG 7) by 2030, other countries such as the Democratic Republic of Congo (DRC), Malawi, and Chad still have energy access rates below 20%.

Figure 1: Population without access to electricity by region 2010-22 (Millions)

Source: World Bank, Tracking SDG 7 Report (2024)

Even when households and businesses across Africa have grid connections, they are not necessarily guaranteed reliable energy access. Fewer than half of Africans benefit from a supply of electricity that works most or all of the time. In Nigeria, grid outages significantly dampen economic growth and private sector development with the World Bank estimating that it costs the country around $28 billion or 2% of GDP annually.

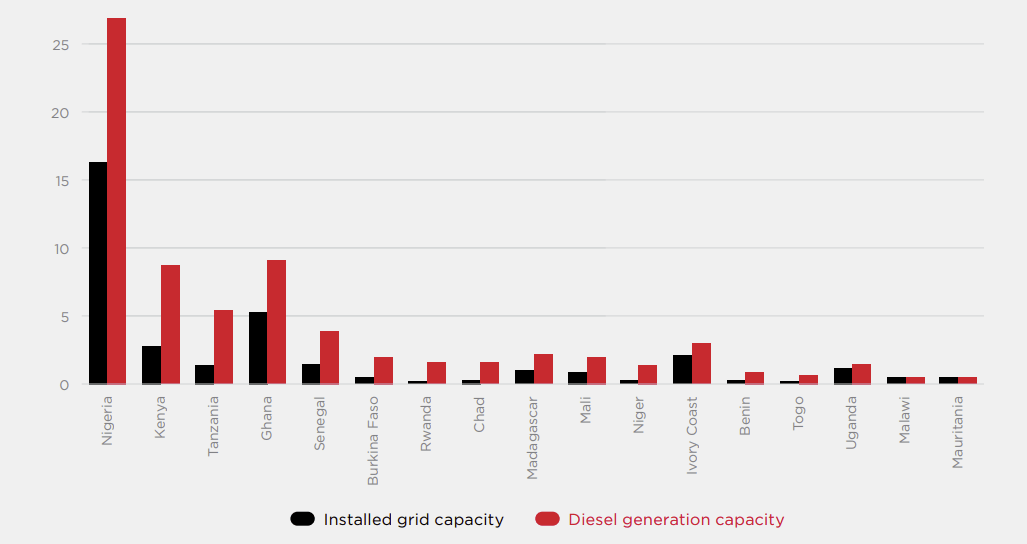

In the absence of reliable grid infrastructure, many households and business across the continent rely on costly polluting alternatives such as diesel generators (see Figure 2). Diesel backup capacity in Sub-Saharan Africa today likely exceeds 100 gigawatts (GW), equivalent to 200 typical coal-fired power plants. In about half of Sub-Saharan African countries, the installed capacity of backup generators is greater than grid-connected power plants. For example, Nigeria has around 60% more backup diesel capacity than grid capacity and households are reported to spend $12 billion annually to operate diesel generators. With electricity demand on the continent projected to grow rapidly over the coming decades, scaling access to renewable energy sources will be key to meeting the region’s energy needs.

Figure 2: African countries with more diesel generator capacity than installed grid capacity (Gigawatt)

Source: Energy Monitor

Why operators in Africa need to go green

As some of the largest private sector businesses across Africa, mobile operators are acutely sensitive to the region’s energy challenges. A recent GSMA survey of operators highlighted that the key energy challenges facing the industry include frequent power outages, lack of grid access, high energy costs and difficulties accessing renewable energy.

Like other business and households in Africa, many mobile operators and tower companies rely on diesel generators as a source of reliable energy when the grid fails. According to a 2020 GSMA study, 75% of mobile towers in the DRC located in off-grid and weak-grid areas are powered by diesel. But this reliance on diesel carries significant cost and operating disadvantages for mobile operators and tower companies across Africa:

- 1. High and volatile costs: Generating electricity with diesel generators typically costs three to four times more than grid-based electricity in the region, with even higher ratios in countries like the DRC, Ethiopia and Zambia. Prices also fluctuate depending on international price dynamics, countries’ foreign exchange positions and government policies such as subsidies. In 2023 mobile operators in Nigeria spent an estimated 430 billion Naira (~$270 million) on fuelling tower infrastructure, an increase of 35% on 2022. This rise was driven by a mix of foreign exchange movements, the rising cost of crude, and the removal of a longstanding government fuel subsidy. Transporting diesel to remote sites can also be expensive – particularly in countries facing significant infrastructure challenges. Across many countries the cost of buying and transporting diesel can make up 30-60% of a mobile operator’s total operational expenditure.

- 2. Poor reliability: Multiple generators need to be installed to guarantee continuous energy supply for network uptime. Disruptions in network uptime can have significant economic consequences since mobile connectivity is the foundation for a range of essential services. For instance, the annual transaction value of mobile money transactions in Africa is over $836.5 billion highlighting how mobile connectivity is a critical foundation for economic activity across the continent.

- 3. Regular maintenance visits: Diesel and filters need to be frequently replaced, which means remote sites have to be visited up to every 10 days. Generators themselves typically need to be replaced or rebuilt every 18-24 months because they are designed to provide back-up power when the grid fails rather than acting as a constant source of power.

- 4. Greenhouse gas emissions: An average single-tenant telecom tower site powered 24/7 by a diesel generator consumes about 28,000 liters of diesel per year. Diesel generators contribute to poor local air quality and generate 60% more CO2 than the average grid-based electricity in Africa. The need to reduce CO2 emissions across the mobile industry stands out as a crucial challenge for mobile operators. Around half of mobile connections in Sub-Saharan Africa are represented by operators with science-based targets and net zero targets.

- 5. Theft: Up to 30% of diesel stolen according to estimates by tower companies. A GSMA study estimated that theft added 10-15% of diesel to the cost of supplying diesel to towers.

Beyond these issues, digital inclusion and the usage of mobile services stand out as other important reasons to pay closer attention to the energy challenges facing mobile operators and tower companies across the region. Sub-Saharan Africa is the region in the world with the largest gaps in both mobile coverage and usage (Figure 3). Around 180 million people in sub-Saharan Africa are not covered and not connected to mobile broadband (the coverage gap). But more importantly, 680 million people in the region are covered by mobile broadband but are not using it (the usage gap).

Figure 3: The coverage and usage gaps in sub-Saharan Africa

Source: GSMA State of Mobile Internet Connectivity (2024)

Lack of affordable, reliable, and sustainable energy access affects the coverage and the usage gap through three main channels:

- Limiting network deployments – Some network deployments in rural areas can be prohibitive due to high energy costs. As mobile operators determine whether to invest in new deployments, high diesel costs (and associated cost of transportation which often tend to be higher for remote rural sites) are a strong deterrent.

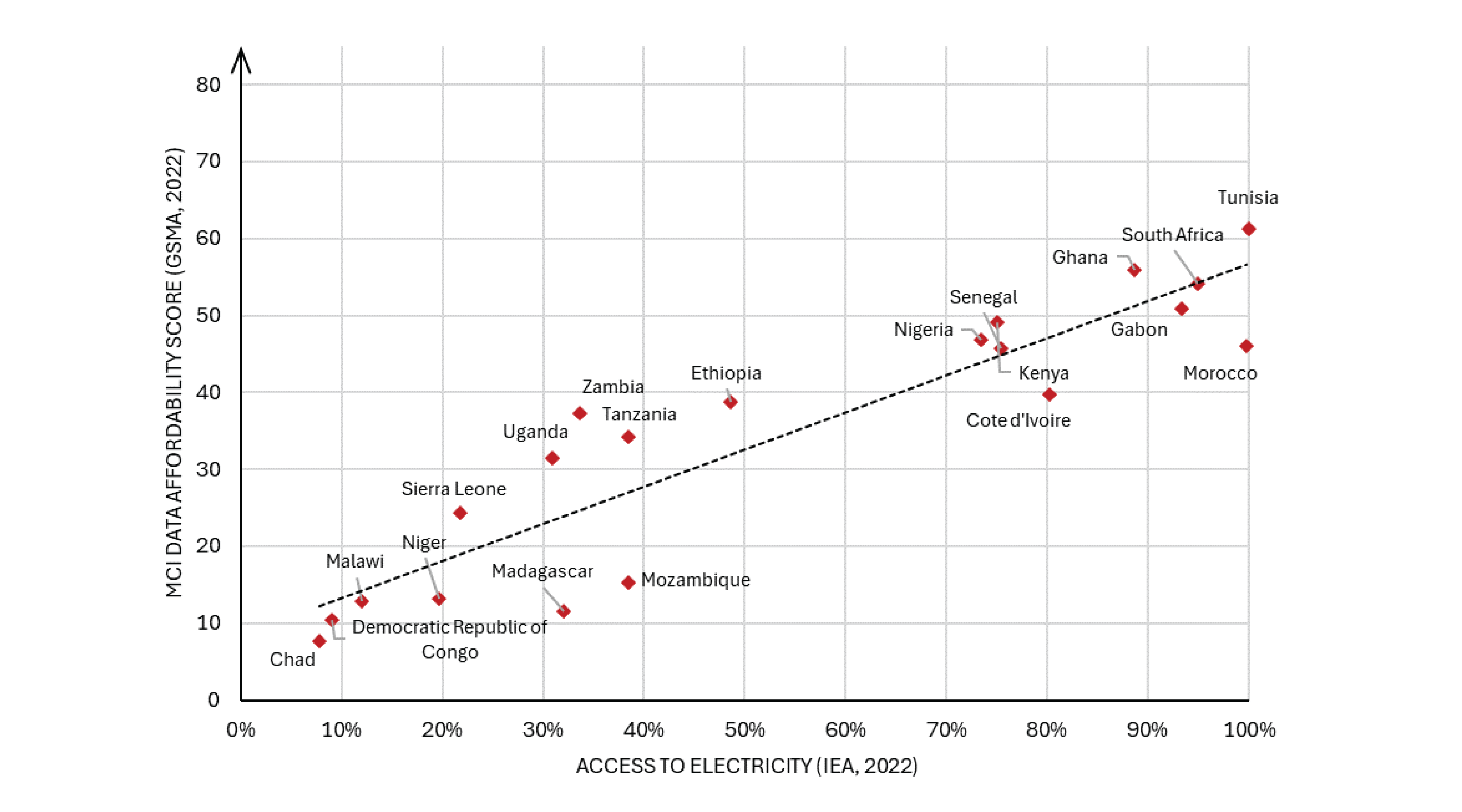

- Costs passed onto customers limit data affordability – While data affordability has improved substantially, Sub-Saharan Africa is still the region with the least affordable data. Fewer than half of the countries in the region have met the UN Broadband Commission’s target of 1GB costing less than 2% of average monthly income. High energy costs facing operators often are passed down to consumers in the form of higher data costs. Countries with the most pronounced energy and infrastructure challenges also tend to have higher data costs (see Figure 4).

- Customers’ own energy access – for both existing customers (in the case of the usage gap) or potential customers (in the case of the coverage gap), peoples’ inability to regularly charge devices discourages mobile usage, and diminishes the commercial potential associated with mobile network extensions in more remote areas. Beyond lacking energy access, the quality and reliability of power supply also matters as grid outages and power surges can result in compromising and breaking mobile devices, or discouraging more mobile usage by households and businesses.

Figure 4: The relationship between energy access and data affordability across selected African countries

Source: GSMA Mobile Connectivity Index (2022), International Energy Agency (2022), author’s calculations

Notes: The GSMA Mobile Connectivity Index Data Affordability Index score provides a score from 0-100 based on the data costs as a % of monthly income across countries

Emerging use cases and the path to scale

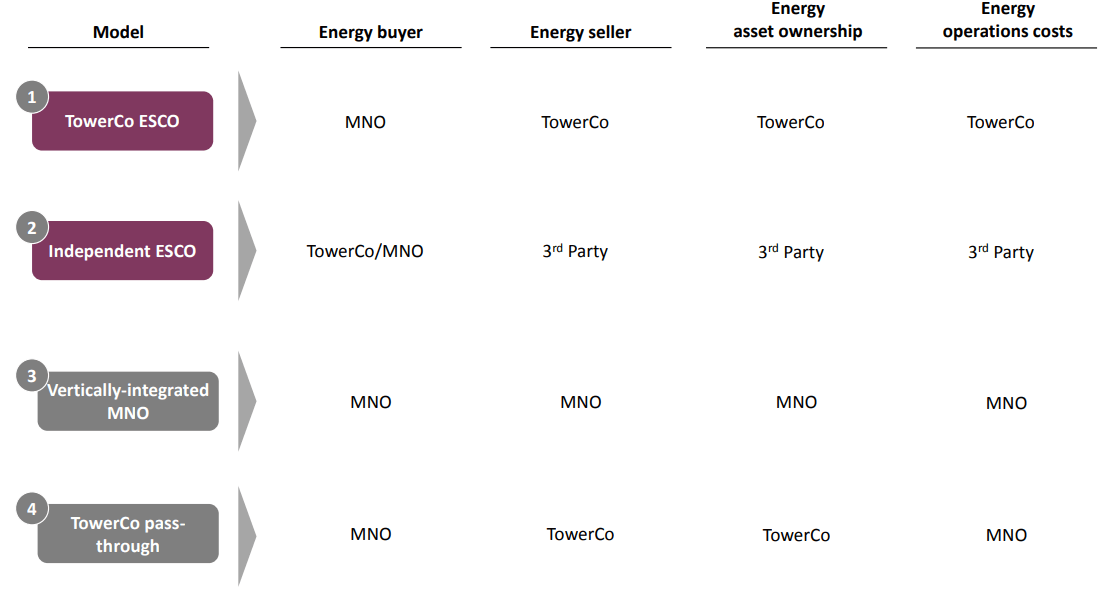

The main prevailing business models in the tower infrastructure industry are defined and differentiated according to how ownership of energy assets as well as the costs of energy generation are shared between energy buyers and sellers (see Figure 5). Business models vary across the continent depending on country context and regulations, mobile operator strategies, and tower ownership dynamics. Ownership of assets signifies not only incurring substantial upfront capital investment, but also the attendant risks that could potentially diminish the value of that investment. Asset owners have the power to upgrade or replace energy assets. This responsibility determines ability and incentives to switch to renewable energy solutions.

Figure 5: Business models deployed at telecom tower sites

Source: GSMA (2014) The Global Telecom Tower ESCO Market

Notes: 3rd party here refers to energy service companies (ESCOs). For more context see ESCO section below

While the scale of the renewable challenge remains immense across all tower business models, many mobile operators, tower companies, and distributed renewable energy (DRE) companies across Africa have made significant progress and have showcased what kind of solutions are scalable and commercially sustainable. Over the last decade the growth of the DRE sector has been enabled by declining international prices for key solar inputs, increased donor support, private investment, integrated energy planning through geo-spatial data analytics, and regulatory reforms. The increased maturity and scale of the sector has also enabled more partnerships with the mobile industry.

Given that African countries have different energy contexts, regulatory landscapes, geographies, and operating environments, there is no one-size-fits-all solution to the energy challenges facing the mobile industry in the region. The two approaches profiled below – energy-as-a-service and anchor-business-community models – are particularly relevant to towers located in located in off-grid and weak-grid contexts and have shown replicability and scalability across different markets and mobile tower business models.

The Energy Service Company (ESCO) model

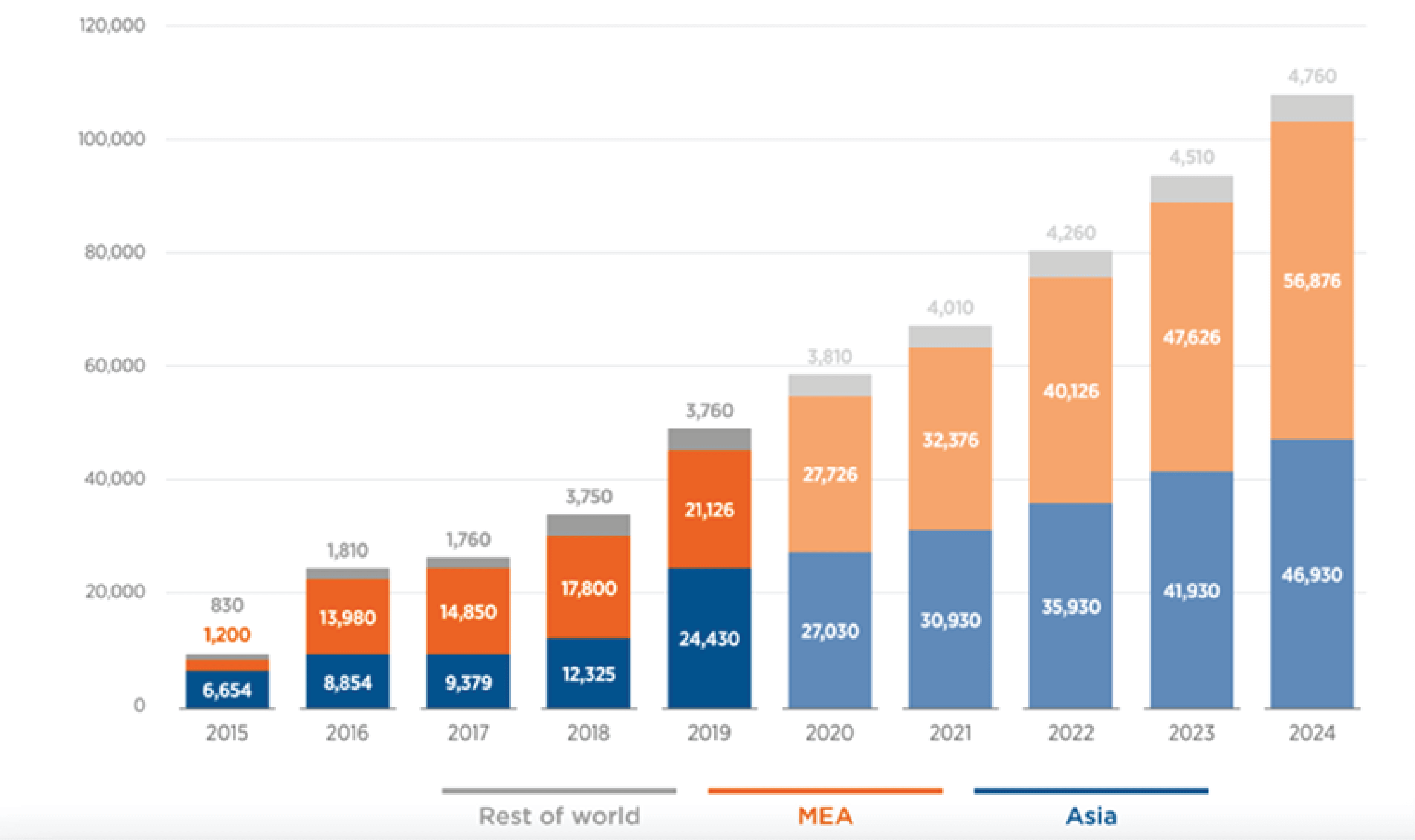

In the same way that mobile operators often outsource to tower companies because of their specific skills in managing tower site requirements, there is an increasing trend towards outsourcing the supply of reliable power at tower sites to ESCOs. Managing power at tower sites is subject to sector-specific generation, delivery, and financing risks. By outsourcing this function to an ESCO through a power purchasing agreement (PPA), which includes penalties for non-performance, operators can offload some of the challenges associated with operating towers in off-grid or weak-grid areas. Figure 6 highlights the actual and projected growth of the ESCO market in Africa and the Middle East in recent years.

Figure 6: ESCO operated mobile towers worldwide: 2015-24 (actual and estimated)

Source: ESCO Report 2020, TowerXchange (2020)

ESCOs historically were engaged to manage fuel supply and the operation of diesel generators, but in recent years have evolved to provide renewable energy installations. That the contracts with operators tend to be long-term (10 years or more) is a key enabler for these investments, as ESCOs can depreciate renewable energy equipment over a longer period and generate attractive financial returns.

| Examples of renewable ESCO deployments in Africa: – In Nigeria, Airtel Nigeria has chosen Watt Renewable Corporation, an independently owned provider of hybrid solar solutions, to install solar power and lithium-ion battery storage across 600 sites under an energy-as-a-service PPA. – Energy Vision is another ESCO solution provider with operations across Ethiopia, Nigeria, and Gabon, and a focus on hybrid and pure solar solutions as well remote management systems to maximise energy efficiency at every tower site. – AktivCo, the ESCO of Camusat, provides energy service solutions to telecom towers across Africa. The company currently operates over 6000 ESCO sites. In 2022, AktivCo obtained financing from the Facility for Energy Inclusion to provide clean energy and expand its operations in Chad, Niger, Cameroon, Côte d’Ivoire and Burkina Faso. – Communication and Renewable Energy Infrastructure (CREI) holds a portfolio of telecom tower and renewable power assets across Africa and Asia, and powers several mobile operator sites in high energy deficit countries such as South Sudan and the Central African Republic. |

Other companies that have found success in Africa’s C&I (commercial and industrial) solar market such as CrossBoundary Energy are developing and deploying suite of energy solutions tailor-made for the mobile industry. Similarly to the mobile industry, other C&I segments in Africa such as manufacturing, mining, or brewing are also increasingly opting for DRE solutions to meet their energy needs. This is partly due to grid-connected energy becoming more expensive as struggling utilities look to improve their finances while the reliability of these grid-connected energy services is not improving. It is also because – similarly to mobile operators -corporate social responsibility (CSR) and environmental, social and governance (ESG) requirements by publicly traded companies require companies to reduce emissions across their supply chain. These dynamics are a catalyst for the growth of energy as a service companies providing renewable energy solutions focussed on the C&I segment, which has benefitted from increased funding and merger and acquisition (M&A) activity.

Many tower companies now also offer energy-as-a-service solutions. From 2018-22, American Tower Corporation invested approximately $345 million to reduce emissions and generate energy across sites in Africa, primarily focusing on solar arrays for onsite power and lithium-ion batteries for energy storage.

While high the cost of capital for renewable energy projects in Africa, which can be 2-3 times higher in Africa than in advanced economies, continues to be a barrier to growth, energy-as-a-service and C&I solar solutions are set for a decade of growth and expansion.

The Anchor-Business-Community (ABC) mini-grid model

In many African countries, mobile operators are providing connectivity in the absence of grid-connected energy services. In these off-grid locations, there is an opportunity to deploy mini-grid systems with mobile operators and tower companies as the “anchor customer”, while these systems also supply power to local businesses and households. For mini-grid providers, having a mobile tower as an anchor client ensures there is a constant energy demand, which helps balance energy loads, and improves the commercial viability of the entire project.

ABC model project in Bukavu, DRC Source: BBOXX (2022)

The ABC model has been considered for over a decade, but faced several challenges in implementation, financing, and stakeholder alignment. Key trends over the last decade have enabled the model to be scaled and replicated across more sites: the maturing mini-grid sector in Africa and the associated increase in financing, geo-spatial planning tools to identify optimal sites for deployments, growing mobile industry interest in DRE solutions, and successful pilots and blueprints that can be replicated and scaled. The following use cases from countries with high energy access gaps such as the DRC and Madagascar highlight these trends (see box below).

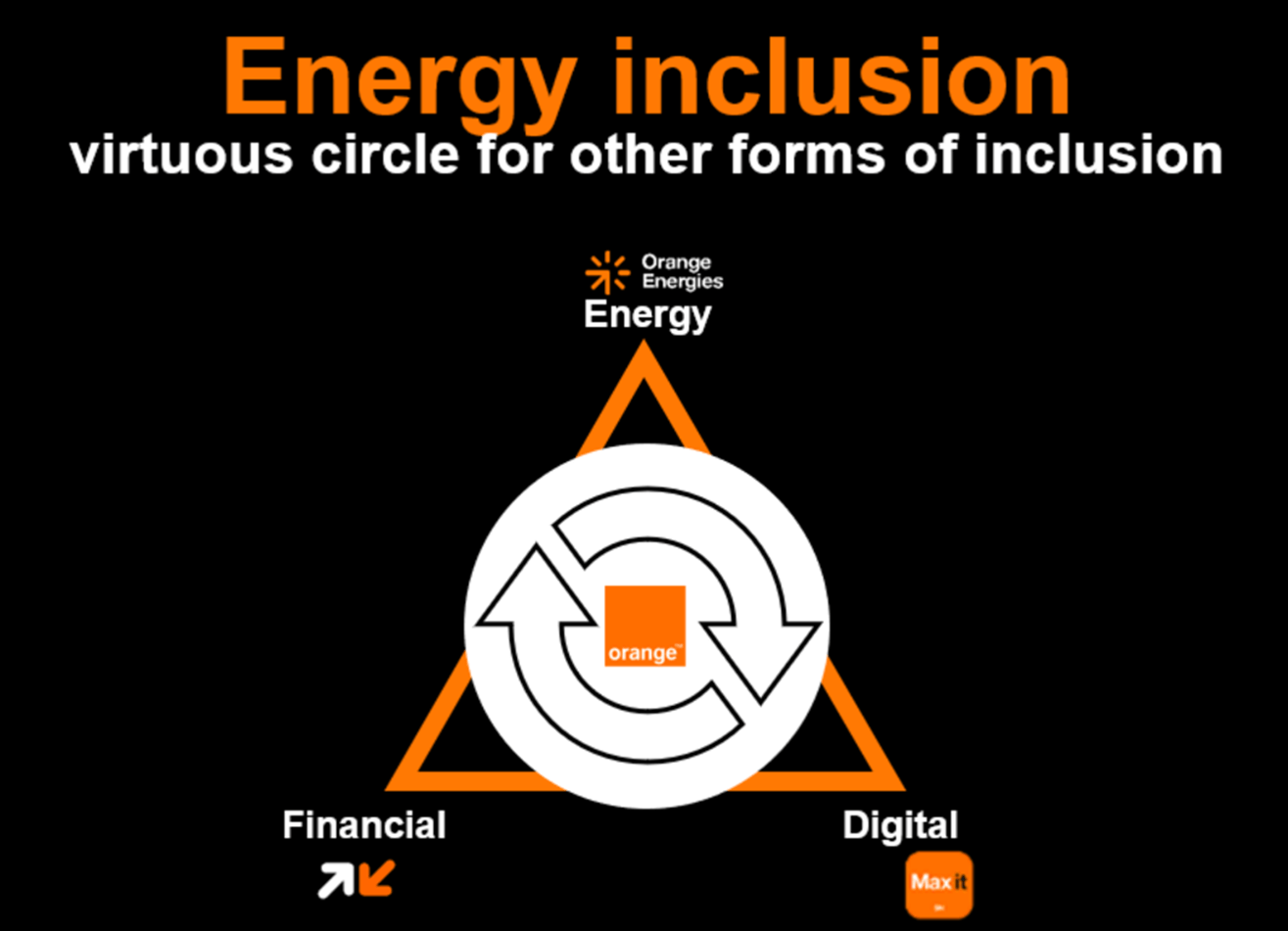

| ABC model deployments in the DRC and Madagascar In the Congolese city of Bukavu, which faces frequent grid outages, Orange has partnered with a joint venture between Bboxx, a pan-African off-grid solar provider, and GoShop, the largest solar engineering, procurement and construction company in the DRC. The joint venture built a hybrid mini-grid plant (85% solar) to supply energy to Orange’s telecoms infrastructure as well as connecting more than 600 households around the tower to reliable electricity (see more in this short clip about the project). The partnership also allowed for the integration of Orange Energies’ smart metering platform and Bboxx Pulse®, Bboxx’s integrated operating system. The merger of these technologies enables the monitoring of the mini-grid’s performance and the remote management of customers, including collecting and managing payments through pas-as-you-go (PAYG) solutions. BBOXX and Orange hope to scale this model beyond Bukavu and replicate it across other tower sites in the DRC. For Orange, taking an integrated approach to energy- and digital connectivity is vital as the company sees as virtuous cycle between energy access, financial inclusion, and digital connectivity (see Figure 7). Our research on the value of PAYG solar for mobile operators confirms that a customer’s transition to PAYG solar benefits mobile operators commercially through higher mobile money and mobile usage, as well as building digital literacy and driving demand for digital services. Other mini-grid companies such as Nuru have also successfully implemented several ABC models in the DRC. The company is currently powering 10 mobile operator towers across four operational assets and is in close collaboration with mobile operators such as Vodacom and tower companies such as Helios Towers. Having closed over $40 million in Series B equity funding last year, Nuru aims to serve 35-40 towers in Goma, Kindu, and Bunia by 2026 as part of its scaling journey in the DRC. Madagascar is another country where we have supported and observed several successful ABC model projects. WeLight, a joint venture of Axian Group, Sagemcom, and Norfund, operates mini-grids in Madagascar and Mali and has pioneered several ABC model projects in Madagascar. In 2018, the GSMA Innovation Fund provided the company with a grant to test the commercial viability of providing electricity to off-grid villages in northern Madagascar, while also leveraging Telma’s off-grid mobile towers as anchor clients. After successfully demonstrating the viability of the model during the grant, WeLight has scaled it to other sites. WeLight recently raised €19 million from a group of investors including the European Investment Bank to bring clean, affordable and reliable energy to 120 off-grid villages in Madagascar. The company currently powers 31 off-grid mobile tower sites in Madagascar in collaboration with Helios Towers and Towers of Africa. |

Figure 7: The virtuous cycle between energy access, financial inclusion, and digital connectivity

Source: Orange Energies (2024)

Other leading mini-grid providers in Africa such as Husk Power and PowerGen are also serving some mobile towers as anchor clients. Yet, they and others caution that despite some progress, there are important barriers to the implementation of the ABC model. Many mini-grid companies view mobile operators and tower companies as quite demanding clients due to their service level requirements, strict supplier contracts, and the operational complexities associated with servicing tower assets. There are also some practical challenges associated with geography and population density such as a settlement’s distance from the tower, the wider terrain, and the prospective energy demand of households and businesses surrounding the tower. All of these are crucial to effectively sizing a mini-grid and operating a commercial sustainable business model. Finally, contrary to the ESCO model, mobile operators, tower companies, and mini-grid providers need to align interests and objectives since aim is not just to power the mobile tower infrastructure, but to also support wider rural development by powering surrounding businesses and households.

A mini-grid project in rural Madagascar, Source: WeLight (2018)

Looking ahead

As the demand for digital services and digital connectivity will continue to increase across Africa, mobile operators will continue to upgrade existing network infrastructure and build data centres to accommodate the needs of governments, businesses and households. This will result in growing energy needs for both towers and data centres, and further underlines the need to transition to scalable, sustainable, reliable, and affordable energy solutions, and to increase energy efficiency across their networks. It also highlights the need for governments, regulators, and development finance institutions to pay closer attention to the intersections and synergies between the energy and digital sectors and promote cross-governmental action plans and strategies that recognise that energy is central to achieving digital objectives and that digital is central to achieving energy objectives. There are a range of new donor initiatives operating at the intersection of digital connectivity and energy access:

- The World Bank has a growing focus on the green digital transformation and works with a range of government and private sector stakeholders across the energy, and digital sectors to both ensure that the expansion of digital access is powered by renewable energy sources, but also to highlight the role that the digital ecosystem plays as a catalyst of the renewable energy transition across other sectors. Major new energy projects such as the Distributed Access through Renewable Energy Scale-up (DARES) project in Nigeria, and the Accelerating Sustainable and Clean Energy Access Transformation (ASCENT) programme across Eastern and Southern Africa, offer exciting opportunities to deepen the collaboration and synergies between energy access and digital connectivity.

- The Alliance for Rural Electrification (ARE) is currently working on their new ‘Powering Industries’ initiative, which seeks to connect renewable energy suppliers and industries in emerging markets with decarbonisation objectives and challenges in accessing reliable and affordable power. This may for example include “demand-side” sectors such as telecom, connectivity, tourism, agriculture, mining, healthcare and mobility.

- The Health Electrification and Telecommunications Alliance (HETA) is Power Africa’s flagship initiative for health facility electrification and digital connectivity in sub-Saharan Africa. Its mission is to catalyse public-private partnerships and sustainable business models that increase access to reliable, renewable energy and digital connections. These improvements are vital for supporting equitable access to care for people across the region.

It is also great to see many operators already taking concrete steps towards greening their network and meeting their net zero objectives. For instance, Orange has made significant progress on implementing both ABC and ESCO models and greening its network footprint across Africa and the Middle East. More than 8,000 sites, or nearly 20% of the group’s sites in the region are solarized, and it produces 3.4 MWp of solar energy to supply data centres across seven countries in the region. As Hassanein Hiridjee, CEO of Axian Group, highlighted in a high-level panel on energy at the World Bank/IMF’s spring meetings, the intersection of energy and digital connectivity is also at the core of Axian Group’s strategy. The company’s energy division Axian Energy working energy use cases such as renewable and hybrid energy production infrastructures (New Energy Africa), mini-grids (We Light), and hydroelectric power (CGHV). Despite this progress, mobile operators and tower companies need to accelerate their transition to renewable energy sources to meet both their net zero- and commercial objectives in the region.

Be a part of accelerating the industry’s renewable energy transition

The GSMA has united some of the largest mobile operators in Africa as part of a working group to accelerate the transition to renewable energy across the industry. As part of this effort, the GSMA has identified initial priority markets (Nigeria, and the Democratic Republic of Congo) in which we will drive concrete industry action to scale renewable energy solutions for mobile operator infrastructure, and share learnings, blueprints, and replicable models with operators across the continent.

Please reach out if you would like to participate in these identified markets. The GSMA will also a publish a study highlighting some key insights about mobile industry power needs at our upcoming MWC Africa conference. If you’d like to learn more, connect with us be emailing us:

This initiative is currently funded by UK International Development from the UK Government and is supported by the GSMA and its members.