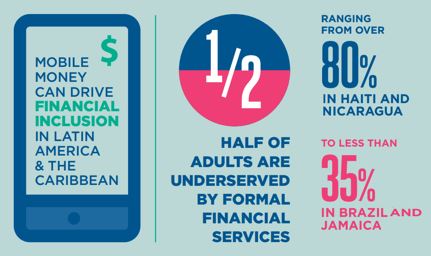

For years, the mobile money industry in Latin America has been playing catch-up with the rest of the world. While low rates of financial inclusion coupled with a rapidly increasing penetration of mobile technology have presented a fertile ground for the growth of mobile money, it hasn’t proven an easy business, requiring heavy and continued investment for several years before achieving scale and maturity. Attracting the necessary investment is particularly difficult when the business is not regulated, or the regulation is unclear.

Earlier this week, we published our global report, the Decade Edition of the State of the Industry Report on Mobile Money, based on the GSMA Mobile Money Programme’s annual Global Adoption Survey. A closer look at our survey data from Latin America provides regional insights and illustrates how regulatory change is impacting the growth of mobile money services in the region.

Over the last few years, the majority of financial regulators in the region have understood the power that mobile money has to deliver financial services to the underserved, combat poverty, and boost the economy. Therefore, most regulators across the region have adopted an enabling regulatory framework for mobile money, [1] or are actively working towards adopting one for their market.

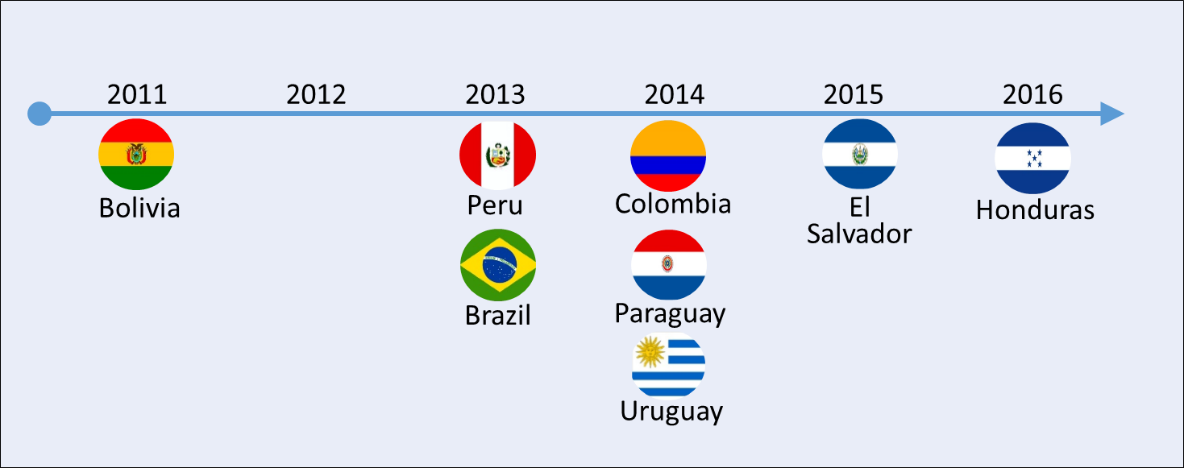

Enabling mobile money regulation timeline

Regulators’ efforts are paying off and, coupled with industry investment, mobile money services are responding with very fast-paced growth across all the relevant metrics: accounts, agents, and transaction volumes and values. Latin America was the fastest-growing region in terms of growth in registered accounts in 2016.

*The Findex database did not cover 3% of the total adult population in the region

Other 2016 highlights

- Active mobile money accounts grew from less than a million in December 2011 to more than 10 million by the end of 2016

- The number of live mobile money services in the region grew from 10 to 33 during this period. At least three countries have more mobile money accounts than bank accounts

- Four deployments have more than a million active accounts each

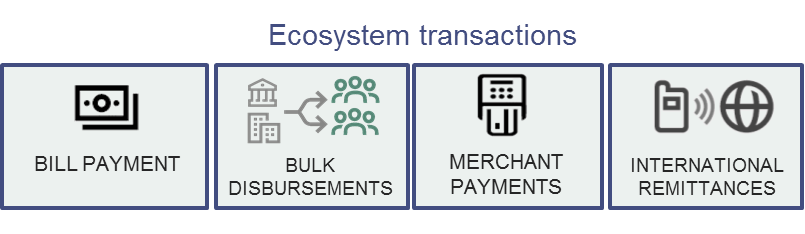

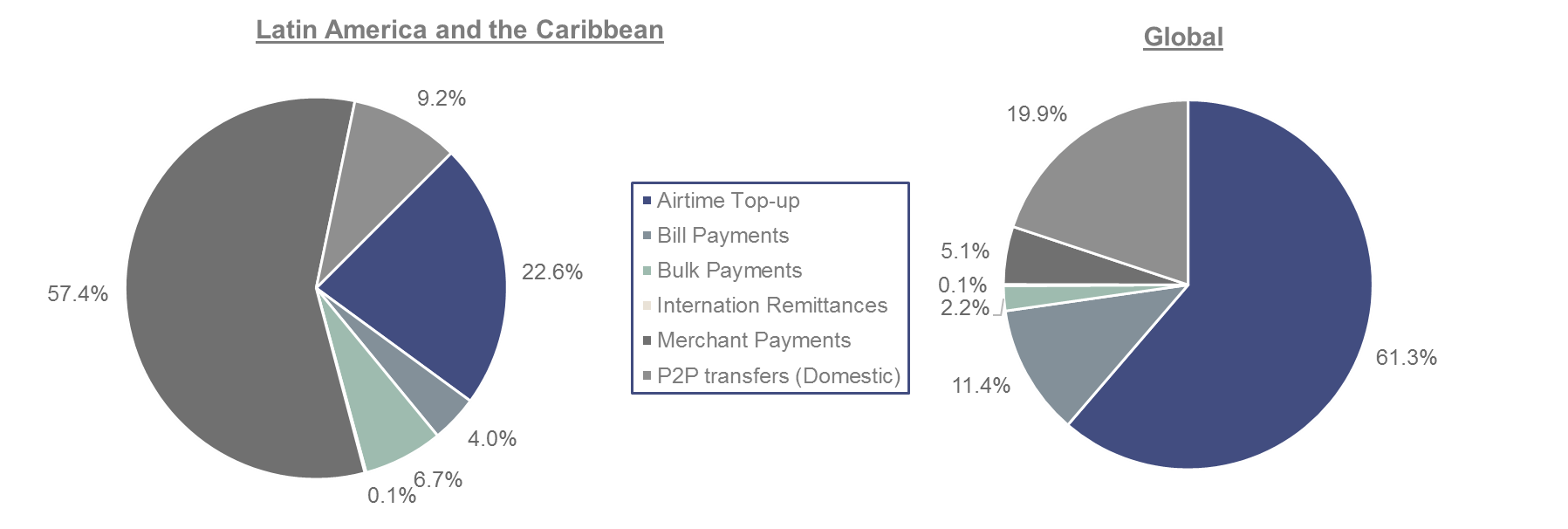

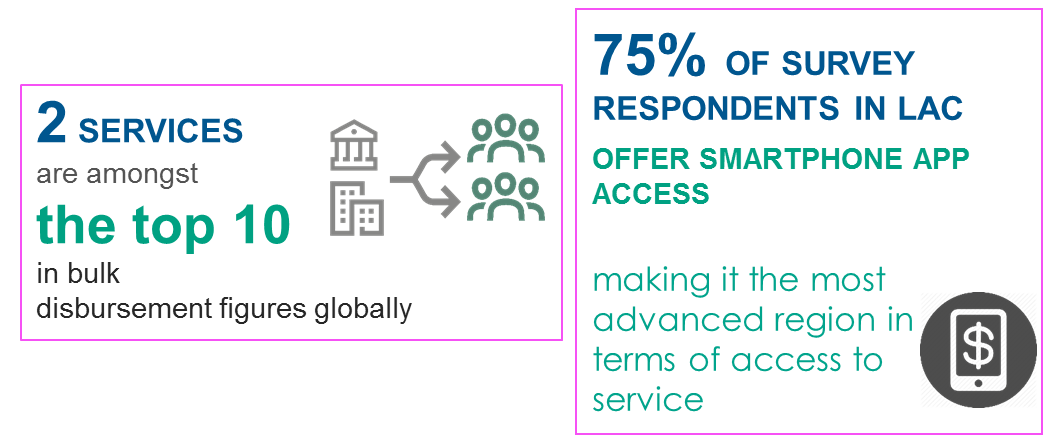

This paints a very promising picture for the future of the mobile money industry in Latin America. Moreover, in 2016 the region had the highest proportion of “ecosystem transactions”—bill payments, bulk disbursements, international remittances, and merchant payments—as compared to any other region. This is particularly promising as ecosystem transactions are a key driver of profitability for mobile money providers, helping them to achieve sustainability and ultimately continuing to expand their product offerings for customers.

Volume of ecosystem transactions in LatAm and Global (2016)

Setting global examples for access to financial infrastructure to grow the ecosystem

As mentioned, one of the region’s strengths is the development of ecosystem transactions. The overall maturity of the financial sector in some countries in Latin America encourages greater interdependence of mobile money providers and traditional financial institutions—here Bolivia and Peru have taken bold steps to support this need and growing ecosystem of transactions.

The recent achievements in Bolivia are remarkable. An open dialogue between the regulator, the mobile money industry, and the financial industry has made it possible for the first mobile money provider to gain direct access to the national (and bank-owned) clearing house, and more will follow. This enables full account-to-account interoperability among mobile money users and bank account holders, helps the formalization of some sectors of the Bolivian economy, and opens up the potential of the ecosystem for all.[2]

In Peru, the national banking association developed a common platform called BIM, to integrate all bank-led mobile money accounts in the country. BIM has also opened its doors to other e-money providers. The system makes it possible to have agent interoperability, which has supported access to financial services in almost every municipality in the country. Additionally, the platform will soon expand its portfolio of services to include bill payments, micro insurance and micro loans to its whole client base.

Towards an enabling regulatory environment

In some markets, regulators have taken noteworthy steps to foster mobile money:

El Salvador and Honduras: Implementing new mobile money frameworks

El Salvador and Honduras each recently issued their respective mobile money regulations. While the regulations are still being implemented, these countries are already regional champions for the industry, now competing with some of the biggest markets in terms of active accounts within Latam. As detailed on a previous blog post, there are still some points of the regulation which require work, but we expect these frameworks will soon meet our definition of an enabling regulatory environment for mobile money. This could attract more investment and competition, which translates into greater and deeper financial inclusion. Honduras, in particular, has shown remarkable development in ecosystem transactions, with a growing number of merchants accepting mobile money payments across the country.

Colombia: The mobile money race picks up

Colombia’s Congress passed the financial inclusion law in 2014, creating a new financial license for non-banks to issue mobile money. The implementation of the law has been slow, but Colombia now has one of the most comprehensive and enabling regulatory frameworks for mobile money. In the coming month, we expect to (finally) see the first mobile money licenses granted. There has been much excitement for these licences and many stakeholders are likely to join forces and deploy mobile money services together with complementary service providers from inception. 2017 could be the year of mobile money for Colombia.

The missing enabling regulatory links

There are a handful of markets in Latin America that have not yet fully embraced the potential of mobile technology for financial inclusion.

Guatemala: Preparing a draft law for mobile money

Guatemala’s difficult political situation in recent years, alongside other factors, have delayed the necessary discussions on mobile money regulation in the country. Nonetheless, Guatemala’s regulators are aware of the huge opportunity that mobile money brings for expanding financial inclusion. To exploit the potential of the mobile technology for financial inclusion, regulators are starting to have an open dialogue with all relevant local stakeholders, with the support of the international development community to prepare the ground for mobile money regulation. Since most of the countries in the region have already been through a similar process, Guatemala can leverage their learning and have a quicker regulatory process.

Argentina: Taking a test-and-learn approach to innovation

Argentina’s new government is determined to modernise and digitise the country’s economy, which today relies heavily on cash. The Central Bank of Argentina is well aware of the potential of technology for this purpose, and has been discussing regulatory adjustments that could lead in the digitisation of the economy. Faced with many new start-ups every day looking to launch transactional services, the Central Bank is considering creating a ‘regulatory sandbox.’ This approach will allow select new players to test their services in a supervised, controlled environment. This allows the Central Bank to understand the risks and logic of the business in order to regulate in a way that does not limit growth. This progressive move may have a positive spill over effect onfast-pace the licensing of non-banks to provide e-money, which is currently not permitted and, despite a positive outlook from the Central Bank, is still detrimental to investment from mobile money providers.

Mexico: Transfer, the giant awakens

Mexico’s bank-led approach to financial inclusion has required mobile operators and banks to operate through interesting joint ventures. This is the case for Transfer, for example, the joint venture between Telcel (a mobile operator) and Banamex (a commercial bank). While such business models often struggle to reach scale, the government’s commitment to financial inclusion and the digitisation of the economy has given mobile money an outstanding push, by disbursing government payments through mobile money accounts. This is convenient and safe for users, and makes the process very efficient for the government.

If regulation were to become ‘enabling’ in markets like Guatemala, Mexico and Argentina, this would have a huge impact on the overall number of accounts in the region. Guatemala, the biggest country in Central America, is the only market in the sub-region that has not yet adopted an enabling mobile money legal framework.

Outlook for 2017

The mobile money industry in Latin America is still young, but 2016 was a year of rapid growth, showing a very positive response from the private sector to the regulatory developments made in the region. Moreover, some specific metrics show that mobile money in Latin America is already developing a mature ecosystem. This is good for the business and customers alike, as it supports business sustainability while giving the customers a richer user experience.

A great opportunity for mobile operators to offer mobile money services and close the financial access gap still exists in Latin America & the Caribbean (LAC). We foresee a progressive better regulatory environment and more open doors to access the financial services infrastructure, leading to better partnerships. We are looking forward to see how 2017 unfolds for the industry still expecting good growth figures.

Notes:

[1] See Mobile Money: Enabling regulatory solutions. Simone di Castri, February 2013. http://www.gsma.com/publicpolicy/wp-content/uploads/2013/02/GSMA2013_Report_Mobile-Money-EnablingRegulatorySolutions.pdf

[2] We are currently working on a case study which document this achievement, hopefully paving the wave for other markets to follow in Bolivia’s footsteps.