This blog was written by both guest author Jorund Buen, Strategic Project Manager and co-author, Maria Hardie, from Brighterlite. Brighterlite was awarded a GSMA Mobile for Development Utilities Innovation Fund grant in 2015 – 2016, you can read the learnings from their grant in Myanmar here.

During its operations in Myanmar, Brighterlite, a pay-as-you-go (PAYG) provider of solar electricity, gathered plentiful information about the off-grid rural electricity market in Myanmar. In relation to a start-up grant we received from the GSMA Mobile for Development Utilities Innovation Fund, we conducted a telephone survey of our customer base, mapping consumer patterns. In addition, daily sales tracking and reporting from staff, field trips to several regions and townships in Myanmar (both in the Dry-zone and Delta areas), and data gathering support from the Asian Development Bank have given us detailed insights about the Myanmar off-grid electricity consumer.

Most publications about Myanmar’s off-grid electricity market are outdated

The electricity market in rural off-grid Myanmar is changing rapidly. According to Myanmar’s 2014 Census, only around 14.9 per cent [1] had access to the national grid in the rural areas. The rest of the rural population relied on other sources for lighting, mainly kerosene, candles and batteries, and only 12 per cent had solar electricity access. Therefore, Brighterlite and others have tried to tap into what we believed was a sizeable un-served market, replacing candle and kerosene usage with cleaner and healthier electricity solutions.

However, our experience from villages around Myanmar is that the on-the-ground reality now differs substantially from the one described in the Census. Solar technology, especially modular solutions where parts such as the panel and battery are bought separately, is becoming the new standard in rural Myanmar. It is rapidly replacing candles and kerosene, but also battery usage. In Myanmar today, kerosene users are very few and far between – in some rural areas the average household member may not even know what kerosene is anymore. Rather than having the opportunity to tap into an un-served market, solar home system providers now need to compete in a market already served with rather similar products.

Beyond basic needs

The mobile phone market in Myanmar is booming and most households now have access to at least one mobile phone, even in rural Myanmar. In most places, the majority uses smart phones just like you and me (but cheap Chinese brands). They need more power, and smart phone usage is rapidly increasing. Charging a smart phone commonly costs 0.15 USD/charge at the small shop on the corner (4.5 USD/month if the phone is charged every day, which many phones are), which equalled our monthly fee, so we thought households wanting to save mobile charging costs would constitute a sizeable market for us. However, while there was some demand for mobile charging, most households already had a small battery or a solar panel that did the job.

The Myanmar mobile phone market has been booming since 2014, but so has its market for off-grid charging solutions. In both cases, most households have by now acquired solutions meeting their basic needs. Mobile charging and lighting are now becoming minimum requirements. Consumers frequently aspire for entertainment solutions, such as TVs and loudspeakers. Many rural households already have TVs, but want access to more than the national TV channels, which often means they need to power a satellite dish and receiver.

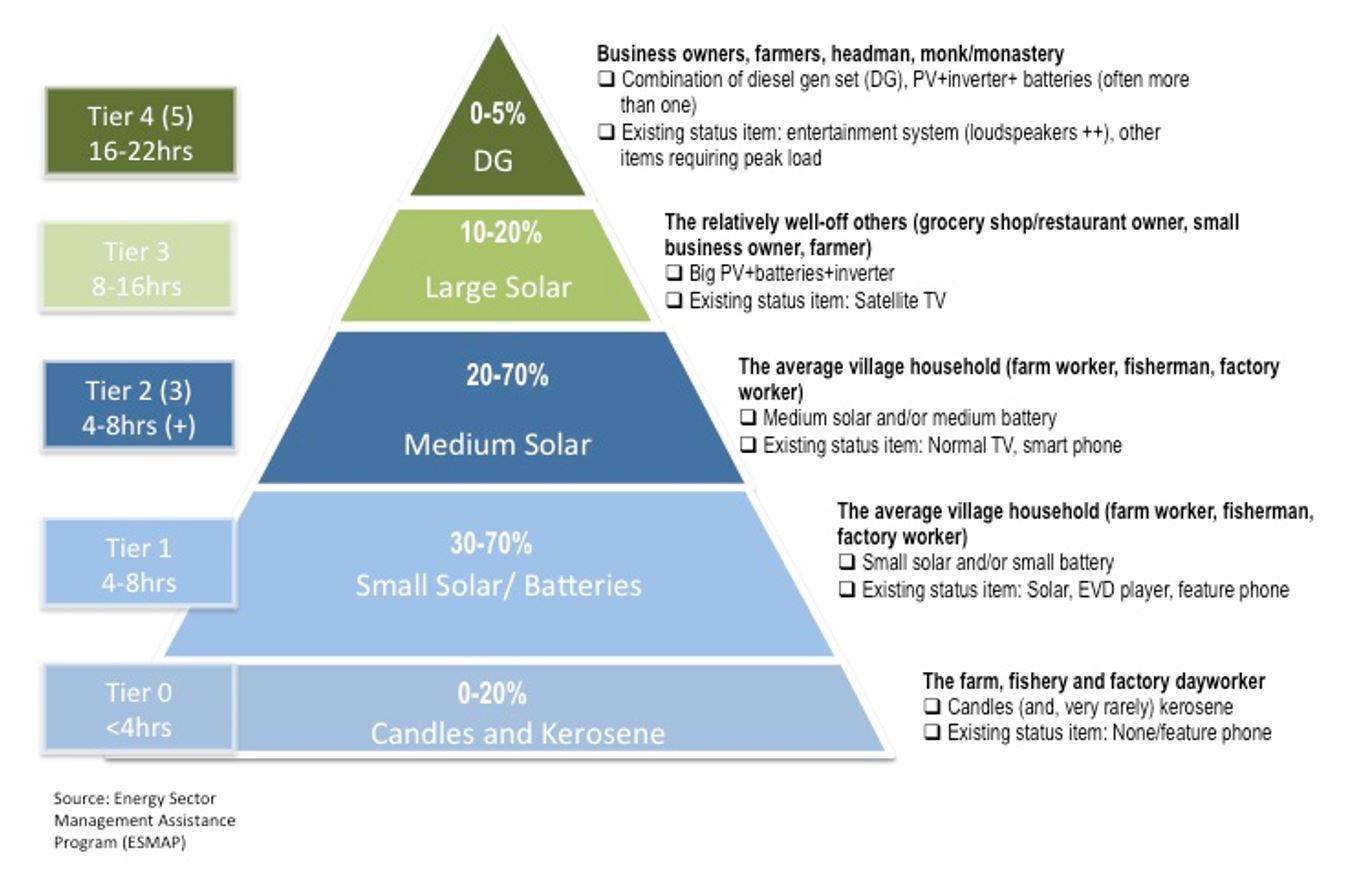

Off-grid electricity consumer pyramid: A simplified segmentation

Based on these findings we attempt to visualise off-grid electricity consumer segments in a typical village in rural Myanmar [2].

The further up the pyramid, the more advanced (and power-hungry) appliances the customers aspire for, and hence the more advanced power solutions they require [3]. Such consumers expect products that can power entertainment solutions such as satellite TV and loudspeakers. The illustration does not directly consider income-levels, but households on the top of the pyramid are more likely to have higher income levels than the lower tiers. While solar is becoming the new standard, there still is a large market consisting of consumers belonging to the lower/middle levels of the pyramid that can be targeted with more advanced solutions. Providers of both electricity and appliances need to analyse how to differentiate themselves within each segment and target group. Targeting the lower tiers (bottom of the pyramid; BoP) should not be underestimated, despite lower income levels, because often: “the lower the BoP income tier is, the higher the percentage of expenditure is used for food and energy” [4].

Energy Sector Management Assistance Program (ESMAP) [5] defines and segments household electricity access into a multi-tier matrix, divided into five tiers, which we have added to the figure for illustrative purposes. Tier 0 represents “no electricity” and tier 4 to 5 represent access of 22 hours (and more). In the pyramid above, the lowest level with candle (kerosene) can be compared to tier 0, small solar/battery with Tier 1 (although the smallest and lowest-quality solar may not satisfy Tier 1 requirements), medium solar with tier 2 (and 3), large solar with tier 3 and diesel gen set with tier 4 (and perhaps even 5). However, the criteria of the multi-tier matrix are more detailed [6], and not fully tested in this context.

Always think one step ahead

The off-grid electricity market in Myanmar changed substantially in the time between Brighterlite’s initial business idea and the implementation phase. Since solar is becoming the new standard, and consumers demand products that cover more than basic needs, off-grid electricity and appliance providers need to find other ways to differentiate themselves, and think one step ahead. While your product package might currently seem to fit well to the realities described in this article, this might not be the case a year or two from now, when you start selling in a rural area in Myanmar. Focus should be on what consumers aspire for, and not only on replacing what they have today.

But what comes after having access to entertainment solutions? Refrigerators and rice-cookers seem to be on many households’ wish list (and to some extent fans, but not as often as one would perhaps expect, given the high temperatures in Myanmar and experiences from other countries). Other possible paths towards differentiation could be to target appliances and power solutions for productive use, and distribution models sharing value with the local community. It could also be wise to start off with solutions targeting the top two segments in the village. While they are not so numerous, they can afford the power solutions and appliances the others in the village aspire for, and after acquiring your products they may function as your enhanced marketing channel towards the larger, lower segments of the ‘village pyramid’.

[1] NGOs, private companies and development actors tend to equalize having grid access to having any electricity access, when referring to Myanmar’s electricity access status. However, this is a misconception, and while only around 14% of the rural population were connected to the grid, alternative electricity sources are being used.

[2] The percentages are only rough estimates and they are not adding up to 100%, because of different possible combinations.

[3] The segmentation pyramid does not consider how product quality (or the importance the customer attaches to product quality) changes when moving up the layers.

[4] (Panapanaan et al., 2016, p. 295).

[5] http://www.esmap.org/sites/esmap.org/files/DocumentLibrary/Multi-tier%20BBL_Feb19_Final_no%20annex.pdf

[6] The ESMAP defines energy access as “the ability to avail energy that is adequate, available when needed, reliable, of good quality, affordable, legal, convenient, healthy & safe for all required energy services across households, productive and community uses”

This initiative is currently funded by the UK Department for International Development (DFID), and supported by the GSMA and its members.![]()