On October 31 2018, different stakeholders including mobile network operators, governments, and development organisations joined GSMA M4D Twitter chat, as part of the activities for this year’s Financial Inclusion Week under the theme Getting Financial Inclusion Right. The chat focused on how to get inclusion right by discussing different solutions to advance financial inclusion through mobile across multiple countries and sectors; including the evolving role of mobile money in agriculture, the digitisation of payments, the challenges of increased smartphone uptake, among others. This blog is a synthesis of the discussion with a gender angle and highlights the actions that public and private sector organisations are taking to accelerate women’s adoption and use of mobile money. An overview of the overall Twitter chat can be found here.

Mobile money is a key tool for women’s empowerment and can contribute to reduce the financial inclusion gender gap. Mobile money has the power to support financial inclusion by delivering significant positive outcomes not only to end users but also to the economy and society. At the micro level, mobile money can empower women by increasing their financial independence and strengthening their role as financial decision-makers. At the macro level, ensuring that women are financially included has broader societal benefits and contributes to many of the UN Sustainable Development Goals. When asked what “getting financial inclusion right” means, participants mentioned the importance of creating and distributing financial services that meet the needs and improve the lives of the underserved, especially women, rural populations and vulnerable groups.

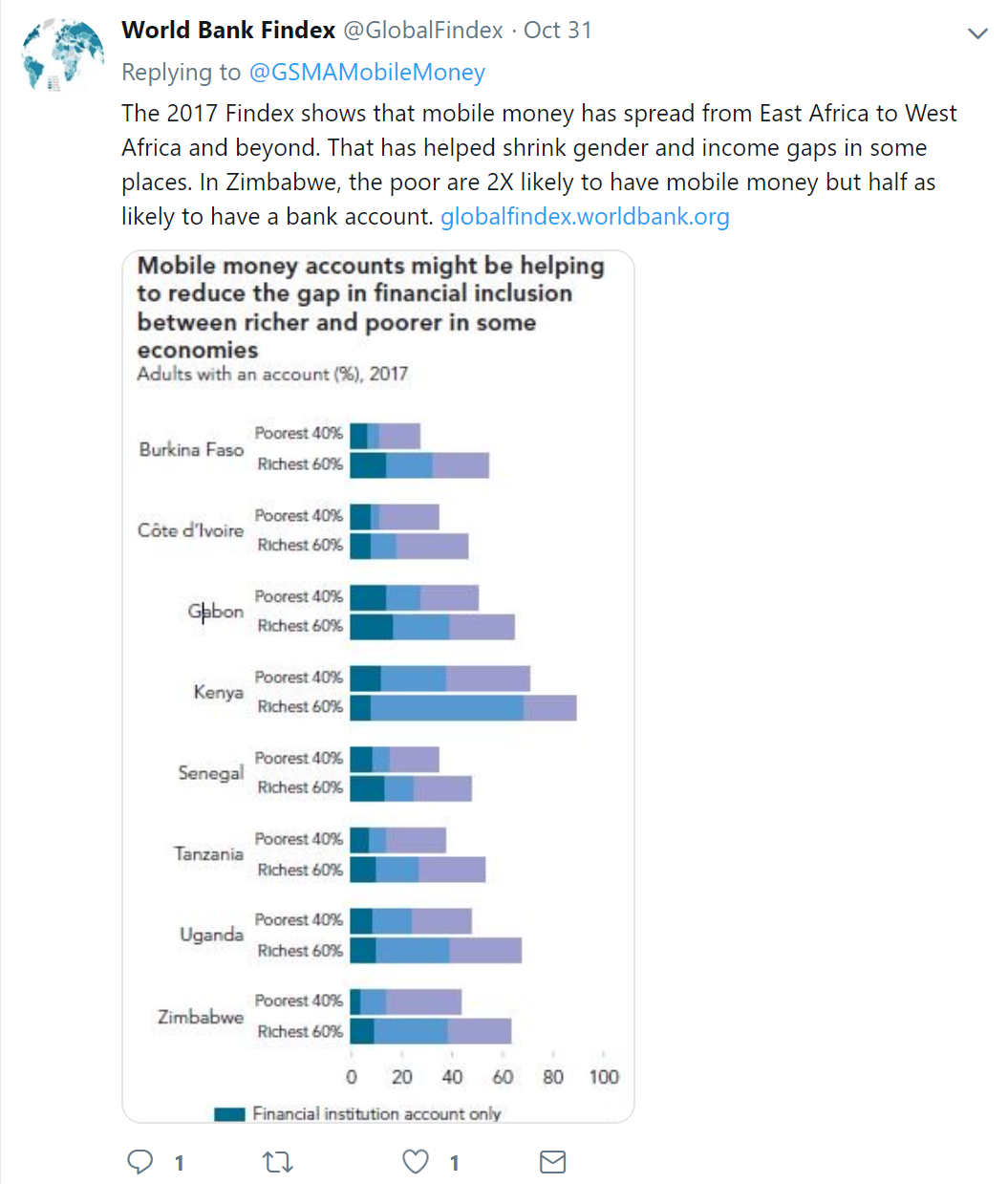

Mobile money is now available in three quarters of low- and lower-middle-income countries, yet, of the 1.7 billion people who remain ‘unbanked,’ the majority are women. Indeed, while women in low- and middle-income countries are estimated to be 10 per cent less likely than men to own a mobile phone, they are on average 33 per cent less likely to use mobile money. However, data from the 2017 World Bank Global Findex also indicates that while there is a gender gap in mobile money across low- and middle-income countries, mobile money can help to reduce the gender gap in account ownership and advance women’s financial inclusion.

Operators are aware of opportunity that mobile financial services provides for women and their businesses and are working to address the challenges that women face in accessing and using these services. Airtel-Tigo Rwanda, MTN Ghana, Dialog Sri Lanka and Telenor Pakistan joined the chat and emphasised the need to ramp up efforts to drive the adoption of mobile money among women. All these mobile operators have joined the Connected Women Commitment Initiative and committed to reduce the gender gap in their mobile money or mobile internet customer base by 2020.

When discussing the most significant actions public and/or private sector organisations can take to accelerate women’s use of mobile money, participants recognized that there are five main challenges that need to be addressed to drive the adoption of mobile money among women: accessibility; affordability; relevance; usability and skills; and safety. In low- and middle-income countries, cost as a barrier tends to be quoted more often by women than by men when it comes to using mobile phones. However, to drive uptake of mobile money it is also essential to ensure that products and services are developed based on an understanding of all the challenges that women face, such as lack of digital skills, limited mobility, and safety concerns. For example, when it comes to accessibility, women often rely more than men on agents being available to help them trust the service. Moreover, research shows that female agents can be an important mechanism to drive adoption, as some women prefer interacting with fellow woman and can feel more comfortable using financial services if another women shows them how.

The gender gap in mobile money use is driven by a complex set of socio-economic and cultural barriers negatively affecting women. Thus, the need to offer financial services that consider women’s capabilities and their preferences and circumstances; such as G2P, agricultural payments, or international remittances. Consulting and involving women and their local communities in the development of products and services from the outset can ensure these are centred on women’s needs. Tapping into traditional behaviours, like women’s savings groups, can also provide a compelling new use case for digital financial services.

In addition, the lack of supply and demand-side gender-disaggregated data prevents stakeholders from measuring the gender gap in mobile money access and use and from gaining a better understanding of the barriers that women face. A number of demand-side studies are already available and provide gender-disaggregated data that can be used to start examining the financial inclusion gender gap; these include the World Bank’s Global Findex, Intermedia’s Financial Inclusion Insights, Finmark’s FinScope Survey, Gallup Payment Surveys and the GSMA’s Mobile Gender Gap Report 2018. However, to address the gender gap in financial inclusion more detailed and consistent evidence is required to inform policy and business practices. During the chat, there was a wide call to collect data on women’s access to and use of mobile money services to develop commercial strategies and the implementation and monitoring of new policies.

Lastly, participants discussed the need for public and private sector partnerships that holistically tackle the barriers that women face to be part of the digital economy and the digital future. There has been a growing momentum among regulators and policy makers to focus on women’s financial inclusion. One year ago, in September 2017, AFI members (central banks and other financial regulatory institutions from more than 90 developing countries) adopted the collected ambitious target of cutting the financial inclusion gender gap by half in each participating country by 2022. Nevertheless, more targeted interventions by all stakeholders are crucial to drive women’s financial inclusion through mobile services.

This Twitter Chat highlighted that the barriers preventing women from accessing and using mobile money are complex, diverse and inter-related and cannot be addressed in isolation of each other. Moreover, it illustrated that coordinated action by many different stakeholders working together is needed to address the gender gap in financial inclusion and ensure women are not left behind.