There are many technical ways to achieve mobile money interoperability

For over a decade, mobile money has been driving financial inclusion, opening access to digital transactions and giving people the tools to better manage their financial lives. Today, there are over one billion registered mobile money accounts globally, spread across 290 mobile money deployments that are live in 95 countries.

The rapid rise of the mobile money industry has been accompanied by an increasing emphasis on the need for account-to-account interoperability. In some markets, service providers have proactively adopted interoperability (either via bilateral connections or through an intermediary), drawn by the promise of commercial and strategic advantage. In some countries, the government or regulator has taken a more active role and created a central technical infrastructure and encouraged players to join. Whereas in other places, regional associations are carrying out projects promoting centralised assets to bring about a more interconnected financial ecosystem. Other market developments add to the current context surrounding interoperability, such as the launch of a mobile industry-led scheme and the provision of industry assets by philanthropic organisations. We have covered in detail the prevalence of these different approaches to interoperability in key mobile markets around the world in our report on Tracking the journey to mobile money interoperability.

As we’re faced with this wide array of potential routes into interoperability, it can be difficult to assess which approach is best suited for a particular market or operator. To the best of our knowledge, no guideline or treatise currently exists to assist mobile money providers in choosing between different technical options for interoperability in a structured and logical manner. Today, the GSMA is releasing a report to address that gap.

A logical framework to assess the pros and cons of interoperability models

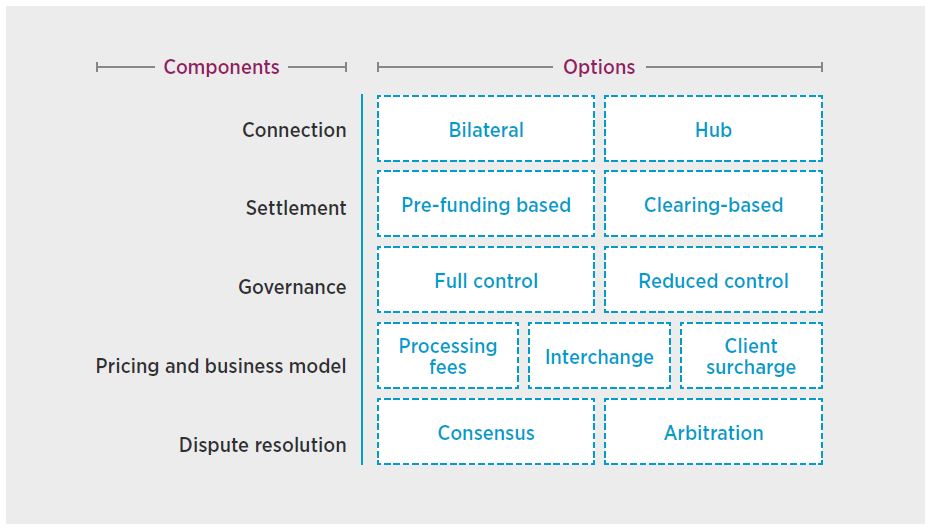

The report adopts a simple methodology to unlock this question. First, it distils the core building blocks of interoperability to classify four broad technical models: bilateral; aggregator-led, mobile money hub-enabled; global payments hub-enabled. It then draws out the technical architecture of each model and studies its specific implications for mobile money providers on key technical and commercial parameters. Finally, the report applies a set of decision criteria to assess the relative strengths and weaknesses of different technical models for interoperability in varied contexts.

Figure 1: Interoperability core components options matrix

Our analysis reveals a number of interesting insights. We find that an industry-owned interoperability hub is likely the best option for the long-term growth and sustainability of the mobile money industry, but the complexity entailed in setting it up implies that bilateral connectivity continues to remain a valuable option for operators.

We also find that different technical models for interoperability may have different liquidity requirements associated with them, which has significant implications for mobile money providers given the specificity of their business model. Many mobile money providers consider the pre-funding requirements of a hub model to be higher than that for a bilateral model, and more needs to be done to provide assurance and clarity to industry participants on this front to address their concerns.

The report also highlights that hub-based models of interoperability (if not implemented with sufficient care) could reduce the ability of industry participants to differentiate themselves, thereby taking away the incentive to innovate, invest in and grow their services. Over time, this may, in fact, have a negative impact on financial inclusion, contrary to the objective of interoperability.

Continuing industry commitment to achieve interoperability in a sustainable manner

The mobile money industry remains committed to furthering interoperability and finding sustainable models to make it happen. We hope this report provides practitioners and policymakers alike with a useful guide to assess the best technical approach to adopt interoperability in a specific context and chart the best course forward. Together with the other report on Tracking the journey to mobile money interoperability that is also being released today, this report continues to make the case for mobile money interoperability in a sustainable manner. We look forward to hearing your feedback on the report!