Over the past few years global shocks, including the COVID-19 pandemic, climate change, conflicts and the ongoing cost of living crisis have reinforced the importance of access to mobile internet. Mobile phones have enabled people to mitigate some of the negative impacts of these global shocks by providing ongoing access to information, health care, education, e-commerce, financial services and income-generating opportunities. Indeed, mobile is the primary way people access the internet in LMICs, accounting for 85% of broadband connections in 2022.[1] While more people are using mobile internet than ever before, growth in connectivity is slowing down and access is unequal. Those who are unconnected are more likely to be women, poorer, less educated, rural and persons with disabilities.

The GSMA will be publishing its annual State of Mobile Internet Connectivity report prior to MWC Kigali in October, which shows the latest trends on mobile internet coverage and usage worldwide, along with the key barriers to mobile internet adoption in low-and middle-income countries (LMICs). The report draws on the GSMA Consumer Survey[2] and the recently updated GSMA Mobile Connectivity Index, which measures the performance of 170 countries against the key enablers of mobile internet adoption.

More people than ever are connecting to the internet through a mobile phone, but the rate of growth has slowed

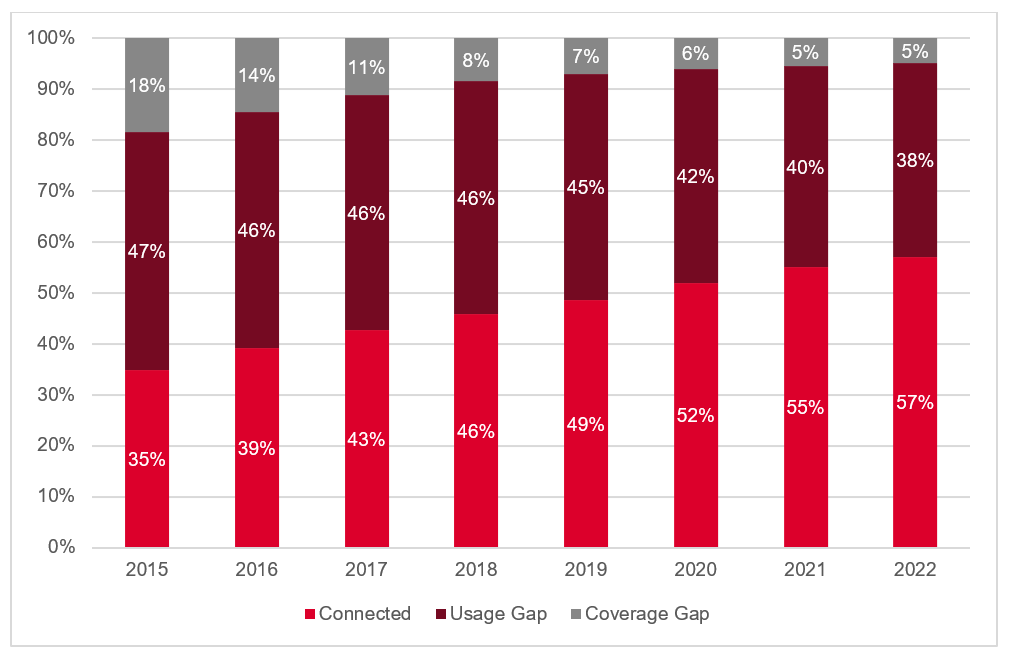

Our new analysis shows that at the end of 2022, 4.6 billion people, equivalent to 57% of the world’s population, were using mobile internet – up from 35% in 2015 (see Figure 1). Although 200 million people came online in the past year, this represents a slowdown in the growth of mobile internet users compared to 2021 and 2020, when 300 million new users went online each year. Just over three quarters of the growth in mobile internet in 2022 came from low- and middle-income countries (LMICs), where 95% of the unconnected population live.

Figure 1: Evolution of global mobile internet connectivity 2015-2022

Base: Total population, 198 countries (totals may not add up due to rounding)

Unique subscriber data is sourced from GSMA Intelligence, combining data reported by mobile operators with the annual GSMA consumer survey. Coverage data is sourced from GSMA Intelligence, combining data reported by mobile operators and national regulatory authorities. Population data is sourced from the UN.

Source: GSMA Intelligence

There are two ways people can be ‘unconnected’; either they live in an area not covered by mobile broadband, or they live in an area that is covered but do not use mobile internet. ‘Usage gap’ refers to those who live within the footprint of a mobile broadband network but are not using mobile internet services. ‘Coverage gap’ refers to those who live in an area not covered by a mobile broadband network.

By the end of 2022, the share of the world’s population living in areas without mobile broadband coverage stood at 5%. This coverage gap has seen little change in recent years and means that almost 400 million people are still not covered by a mobile broadband network, highlighting how the remaining uncovered communities – which are predominantly rural, poor and sparsely populated – are the most challenging to reach.

Meanwhile, with mobile internet adoption outpacing network expansion, the usage gap has been declining slowly in recent years, having dropped from 40% in 2021 to 38% in 2022. However, with 3 billion people living in areas covered by a mobile broadband network but not using mobile internet, addressing the usage gap remains a much more substantial challenge to accelerating digital inclusion. The usage gap is almost eight times the size of the coverage gap.

Connectivity continues to vary substantially by region and income

These global figures mask substantial regional and intraregional differences. Sub-Saharan Africa remains the region with the largest coverage and usage gaps (15% and 59% respectively). By contrast, 85% of the population in North America is now connected to mobile internet. Most regions experienced a slowdown in mobile internet connectivity and it was particularly stark in South Asia, where the growth in mobile internet adoption in 2022 halved compared to 2021.

In Least Developed Countries (LDCs), which remain highly vulnerable to economic and environmental shocks, one in four people are now using mobile internet (25% of the population). However, this remains significantly below adoption levels not just in high-income countries (at 85%) but also other LMICs excluding LDCs (at 57%).

The cost-of-living crisis is stymying mobile internet and smartphone adoption

The report will feature detailed analysis of the barriers to mobile internet adoption, including affordability and literacy and digital skills, which remain the two greatest barriers to mobile internet adoption and use.

While the affordability of entry-level devices (a significant barrier to mobile internet adoption) was generally unchanged in most countries in 2022, the shipment of smartphone devices declined significantly in 2022.

A key factor in the reduction in smartphone sales is likely to be the wider inflationary trend and cost of living crisis. This can impact device affordability for certain population segments by reducing real wages if incomes do not keep up with inflation or by making consumers reluctant to acquire a new device if they perceive a high risk of continued inflation. As highlighted in the upcoming report, affordability continues to disproportionately affect women and other underserved populations.

This wider economic outlook could also partly explain the slowdown in mobile internet connectivity growth in 2022.

Coordinated action is needed to ensure no one is left behind

The social and economic impacts of recent global shocks have been most strongly felt by the poorest and most vulnerable. Without access to the internet, it can be particularly challenging to mitigate the impact of these shocks. This underlines the importance and urgency of accelerating internet access and achieving universal connectivity to ensure those that are underserved are not increasingly left behind.

Our upcoming State of Mobile Internet Connectivity Report 2023 will provide a detailed analysis of the current state of mobile internet connectivity to help inform efforts to address the digital divide. It will include, for the first time, an analysis of the number of unique smartphone users globally and by region; connectivity by type of device, specifically the proportion of mobile internet users that own a 3G, 4G or 5G smartphone or a feature phone; and a more detailed breakdown of the global and regional usage gaps, including the proportion of the unconnected that have a mobile device but are not currently accessing the internet.

With our new data showing a slowdown in digital inclusion, we hope that our upcoming State of Mobile Internet Connectivity Report 2023 will provide valuable insights to inform action to accelerate digital inclusion. It is critical that we ensure no one is left behind in an increasingly connected world.

The State of Mobile Internet Connectivity Report 2023 will be available here from 11 October 2023.

[1] International Telecommunication Union (ITU) estimates for 2022

[2] Carried out every year since 2017, this survey is used to understand access and use of mobile and mobile internet in LMICs. In 2022, it was conducted in 12 low- and middle-income countries.

The Connected Society programme is funded by the UK Foreign, Commonwealth & Development Office (FCDO) and the Swedish International Development Cooperation Agency (SIDA), and is supported by the GSMA and its members.