In a 2016 blog, we argued that smartphones have the potential to drive innovation in product and user experience (UX) design, in addition to supporting increased competition in the mobile money industry. Last year, to understand how growth of smartphone customers will change the mobile money business, we studied the trend of technology use in financial services industries, analysed the entry of internet businesses into financial services, and considered key features of new digital businesses that disrupted the incumbents.

Can smartphone adoption drive a fundamental rethink of providers’ strategy for mobile money businesses? A typical mobile money business can be distilled into five broad functions: fulfilling license responsibilities, building agent networks and customer services, investing in technology platforms, acquiring and maintaining customers, and building products and services. Facebook Messenger’s recent partnership with mobile money providers (MMPs) in the Philippines is just one example of an evolving payments and financial services sector in which mobile money operators have the opportunity to strategically open up access to their assets and leverage a new channel to serve new customers, potentially transforming their businesses.

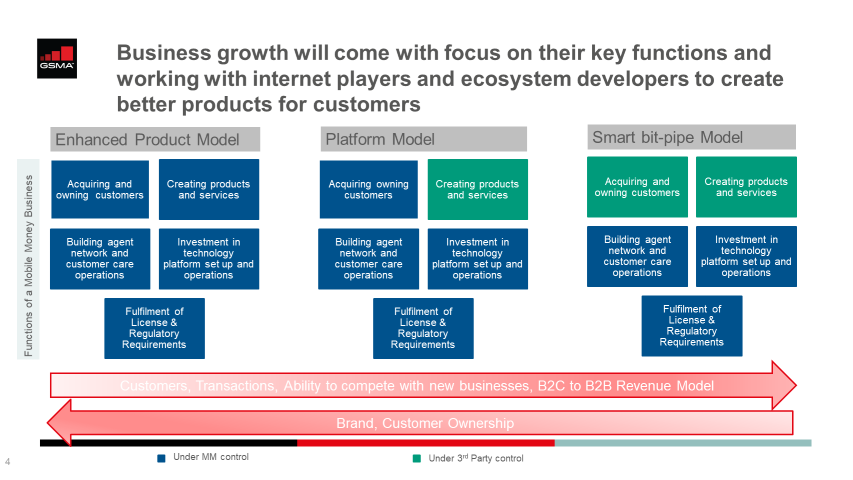

We have identified three possible models for MMPs to follow based on their existing market position, their business assets1 and their aspiration:

1. Mobile money as an enhanced product:

In this model, an MMP maintains the hold over all five functional areas (see Fig 1a) and offers its customers an app that improves the UX compared to a USSD or STK based service. Today, almost all MMPs are following this model.

The advantage of this model is that a provider maintains strong brand and market position to continue offering simple products mapped on a sophisticated user interface (UI) to cater to general market needs. The downside, however, is that ecosystem growth is limited to the organisation’s own innovation and ability to integrate and broker partnerships one by one.

This model is a natural choice for the providers satisfied with their existing position in the market and pace of ecosystem growth. However, they may also remain susceptible to competition outside of mobile money businesses, especially dynamic internet players hungry to grow their ecosystem.

2. Mobile money as a platform:

In this model, an MMP holds control over all functions, but embraces a new openness to partnerships to grow the development of products and services (See Fig 1b). External entities such as start-ups and ecosystem players are encouraged to develop innovative financial services solutions for mobile money customers by providing them access to the platform through APIs. This creates a market place of services for mobile money customers. Smartphones UI provides an opportunity to offer sophisticated product sets such as bundled services, customised solutions and instant services that were not possible due to limitations of USSD and STK based UIs.

This is a B2B2C service model and revenues may be generated by transactions and/or access to the platform. Here, the MMP is leveraging access to the customer base to attract external innovation. Once a provider decides to allow third parties to develop products for their customers, they can experience faster ecosystem growth owing to the roll out of multiple products by third parties.

This model could thrive in markets where fintechs are growing and looking for a means of electronic payment, as well as access to customers. MMPs can position themselves strategically for simple integrations and quick access to customers. Customers, in turn, gain access to a variety of digital products and services. This relieves MMPs of the pressures of product lifecycle and allows them to concentrate on building a robust platform and innovative ecosystem. The providers can also develop new insights from new usage patterns and data, in turn tapping into new revenue sources.

3. Mobile money as an infrastructure:

In emerging markets, internet players have been able to create huge customer bases riding primarily on mobile broadband access and smartphones. This model allows MMPs to retain control of licensing, agent networks and technical platforms, while offering access to these mobile money services to third parties who can develop products and services for their own customer base (see Figure 1c).

This transforms the mobile money business into a B2B model where revenues are generated by access to infrastructure with a service fee. As the mobile money service is plugged into the third party’s business (such as e-commerce or a messaging service) the provider can see exponential growth in service usage (with the right choice of partner).

This model may be suited to providers that have invested in the agent network and built out the operational capabilities and technical platform for the provision of mobile money, but who have not been able to gain traction independently in the consumer-facing model. Such MMPs can partner with one or more third parties interested in launching payments services in the market and benefit from the volume of transactions that a third party such as an internet player could bring.

Figure 1 (a, b, c)

The above models depend on the strategic choices made by providers based on today’s business, market situations and the rising smartphone customer base. The decision should take into account the provider’s business condition, market competition, availability of the right market partners and business aspirations. However, in this dynamic market context, the need for such a strategic rethink may soon become an imperative for a growing number of MMPs looking to secure their future.

Footnotes

[1] Typical mobile money business assets are license, customer base, agent network, customer care and operations and tech platform.