International remittances provide the most tangible link between migration and development. At more than three times the size of official development assistance, remittances are a lifeline for many people in developing countries. In 2017, remittance flows to developing countries reached a new record of $466 billion. However, the true size of remittances is considerably larger than official estimates due to the high use of informal channels, which provide less transparency, less security, and fewer benefits for the millions who rely on international remittances.

In the publication released today, we highlight how mobile money can help to address three key barriers driving the use of informal remittance channels and to accelerate the digitisation of international remittances through formal channels:

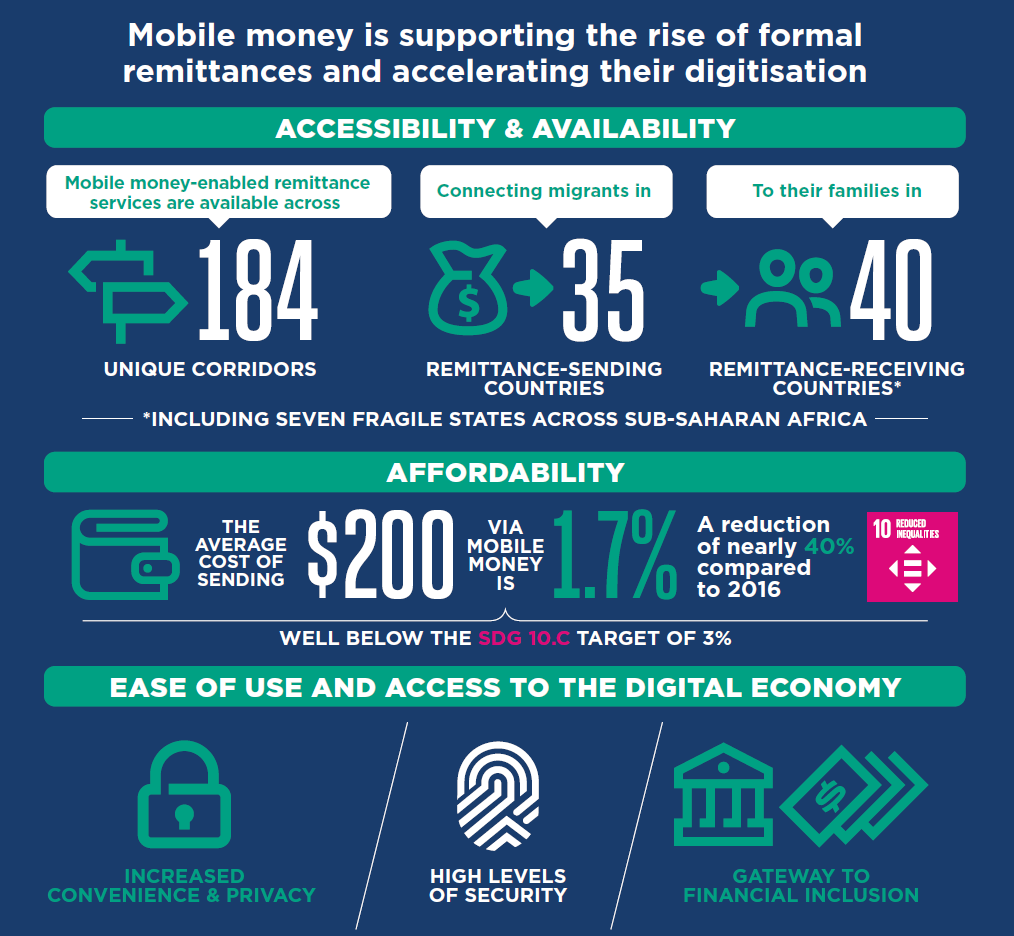

- Availability and accessibility: Extending the reach of international remittances. Mobile money is becoming a widespread channel for remittances, with mobile money-enabled remittance services available across 184 corridors and connecting migrants in 35 remittance-sending countries to their families in 40 remittance-receiving countries. This includes seven fragile states across Sub-Saharan Africa, where reliance on international remittances is often most acute. By catering to the needs of rural households, women, migrant workers and refugees, mobile money has expanded access to international remittances for the most underserved.

- Affordability: Reducing the cost of sending remittances. The average cost of sending $200 using mobile money stands at 1.7 per cent of the transaction. This represents a significant reduction of nearly 40 per cent compared to the previous year, clearly indicating that low-cost mobile money-enabled remittances are a sustainable trend rather than the result of short-term promotional efforts. The cost of sending $200 using mobile money is actually below three per cent in most country corridors (96 per cent), illustrating the role of the service in supporting the achievement of SDG target 10.c. Mobile money is particularly compelling for low-value remittances, with the average cost of sending $50 and $100 standing at below 3 per cent in August 2017 – a significant reduction compared to 2016.

- Convenience, security, and access to the digital economy: Offering unique advantages to compete with informal remittance channels. While less tangible than cost savings, the unique attributes of mobile money such as convenience, security and the ability to access a broad range of digital financial services can maximise the benefits of remittances. As such, mobile money-enabled remittances can serve as a gateway to financial inclusion for migrants and their families.

For a more detailed analysis and a map of the country corridors read our report; Competing with informal channels to accelerate the digitisation of remittances.