This blog was co-written by Anant Nautiyal and Francesco Pasti.

Merchant payments have not scaled in mobile money, but the opportunity is huge

With transaction values exceeding $325 million per month in 2015[1], merchant payments is a prominent use case for mobile money. However, this impressive figure masks the fact that the average number of merchant payment transactions per active mobile money customer currently stands at a very low 0.14 transactions per month – in contrast, the average global number of mobile money transactions (across all use cases) per active user is 11.2 transactions per month[2]. When compared to the number of merchant payment transactions performed by customers in markets where this use case has matured (closer to 8 transactions per month), we begin to realise the untapped potential of merchant payments. The overall size of this use case could be much greater, at $19 billion[3], translating into a potential revenue opportunity of $190 million per month for mobile money providers. Much more needs to be done to fully scale this important use case and expand the mobile money ecosystem.

Strategy fragmentation is the biggest reason for lack of scale

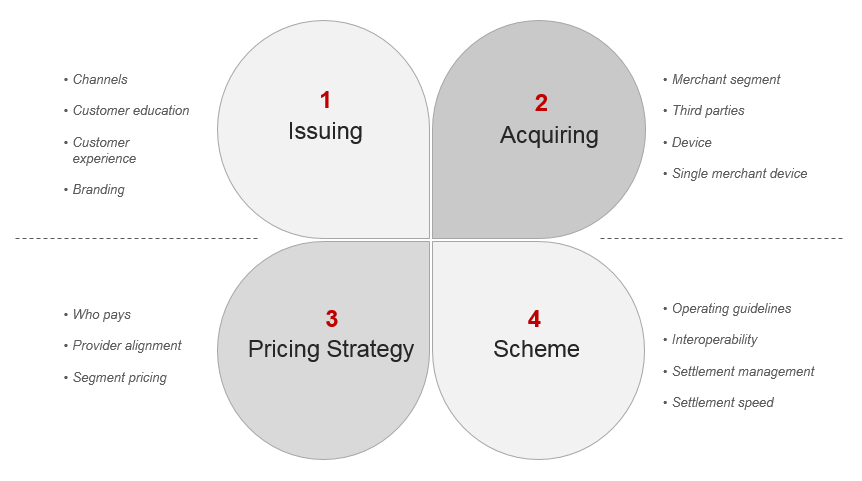

Merchant payments is one of the more complex use cases of mobile money, and may be viewed as comprising of four fundamental dimensions—Issuing, Acquiring, Pricing, and Scheme—with several further parameters to be decided under each.

Merchant payments fundamental dimensions

Providers engaged in merchant payments across Asia, Africa and Latin America are currently following a fragmented approach on nearly every single parameter of merchant payments. Everyone is trying something different and there is little or no collaboration between players, resulting in resources spread thinly across a raft of different strategies, and customers and merchants faced with a bewildering array of inconsistent options to choose from. Some examples of this include:

- Disjointed acquisition of merchants risking duplication of effort and wasted resources

- Non-standardised transaction flows and messaging for customers, leading to different competing experiences confusing the necessary consumer behaviour change

- Different settlement mechanisms resulting in confusion and inconvenience for merchants

Providers must be willing to collaborate and offer harmonised services to scale merchant payments

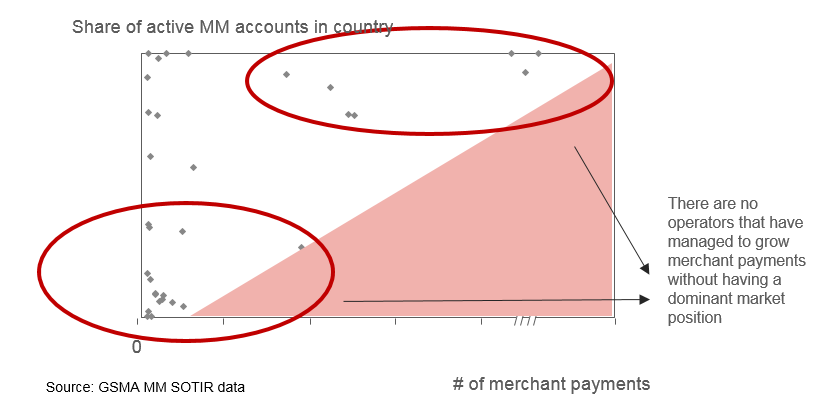

Empirical research suggests that unless a mobile money provider has a dominant market share, it is difficult to scale merchant payments without collaboration with other players. The chart below looks at the number of transactions per provider relative to the share of active mobile money accounts in a country. Providers who don’t have a dominating position in a market have not managed to scale merchant payments. For operators that have a mature agent network, but a low share of active mobile money accounts in a country, collaboration and interoperability are needed in order to scale merchant payments and capture the opportunity.

The case for collaboration to scale merchant payments

In addition to collaboration, when speaking to leading players engaged in mobile-money enabled merchant payments across diverse markets in Asia, Africa and Latin America, certain common factors emerged as the most important for scaling merchant payments:

- Customer education – As with mobile money, BTL marketing and trained representatives are key for the adoption of merchant payments. Joint marketing campaigns are likely to be more impactful – and cheaper.

- Customer experience – Both push and pull transactions have their advantages, but eventually a simple and quick transaction flow should be the end goal. Having many different transaction flows across services is not ideal, and there is a need for harmonised user experience across services.

- Pricing – Charging customers may not be the best option in emerging markets. Operators should explore adjacencies to meet the cost of transactions. Keeping the transaction pricing structure simple and uniform is ideal to build customer familiarity, although exceptions may be necessary in some markets.

- Settlement – Quick and easy settlement is crucial to encourage merchants to accept electronic payments. Having one single account in which all their money can be deposited, and being able to access the funds in real time (or near real time), are very important considerations for merchants.

If you would like more information on these topics, or a copy of our Merchant Payments Deep Dive Toolkit, please write to us at [email protected]

Notes:

[1] See GSMA Mobile Money State of the Industry Report 2015

[2] See GSMA Mobile Money State of the Industry Report 2015

[3] Calculated on the basis of the higher number of merchant payment transactions visible in mature markets