Introduction / Overview

Why is energy important for MNOs?

For many operators, energy consumption has historically been a significant consideration as it is one of the highest operating costs, alongside employee remuneration (see figure 1). Energy is becoming even more important due to climate change and sustainability considerations. The potential increase in data traffic (up to 1,000 times more) and the infrastructure to cope with it in the 5G era could make 5G to, arguably, consume up to 2-3 times as much energy. This potential increase in energy, coming from a high number of base stations, retail stores and office space, maintaining legacy plus 5G networks and the increasing cost of energy supply – call for action.

The current reality is that overall energy usage by the telecoms industry needs to come down as the industry consumes between 2 – 3% of global energy currently. Many national governments are mandating businesses to adhere to energy reforms (e.g. EU’s 2030 climate and energy framework) with the global goal to reduce greenhouse gas (GHG) emissions, since 2014, by 30% in absolute terms by 2020 and 50% by 2030. The telecoms industry is not exempt from these pressures and the evolution to 5G is an opportunity to deliver a cleaner, greener telecoms footprint – indeed, 3GPP’s 5G specification calls for a 90% reduction in energy use.

A growing number of operators have taken a leading role in sustainability, and the use of renewables to meet or exceed these decarbonisation goals and these will expand in the 5G era. The many solutions to enhance network energy efficiency fall into two major groups: increasing the use of alternative energy sources to reduce dependence on the main power grid; network load optimisation to reduce energy consumption.

Figure 1

Network energy costs

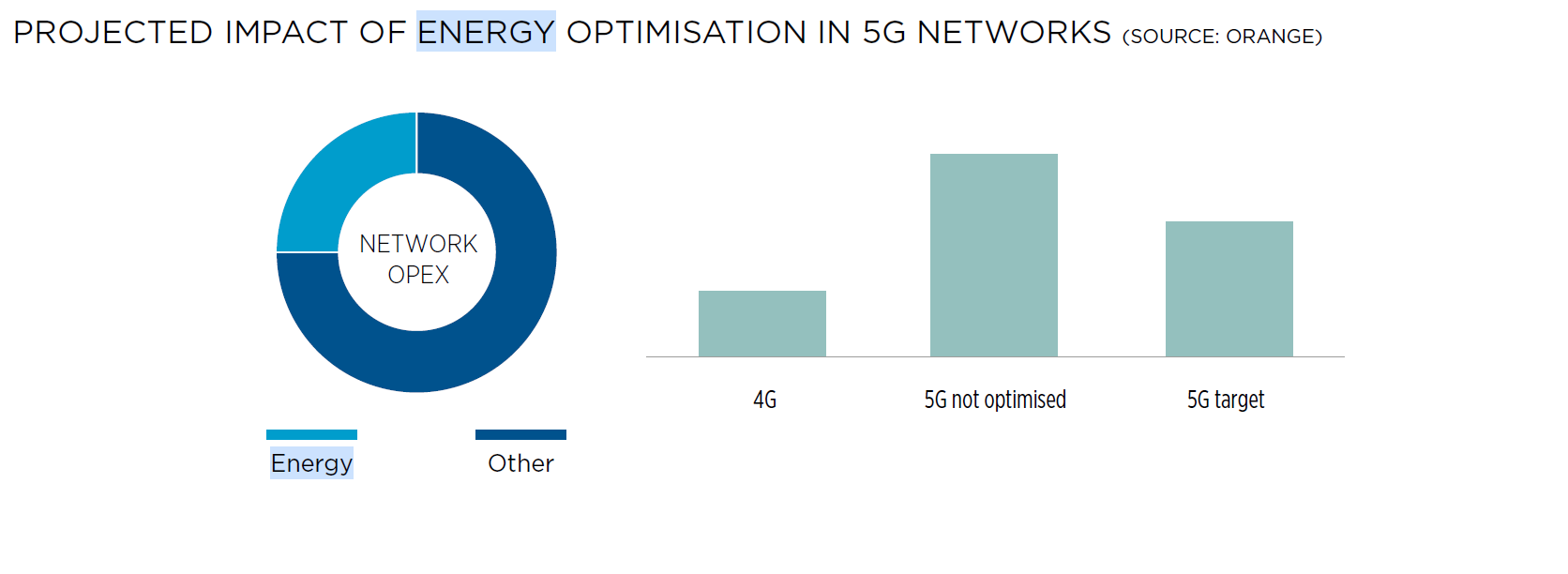

Energy consumption constitutes between 20 – 40% of network OPEX, and there are two schools of thought on how this will evolve for 5G.

There are two opposing schools of thought with regards to network energy consumption in 5G. Some stakeholders point to no overall net increase in the energy consumption of 5G networks by more efficient equipment. For example, Telia and Ericsson believe that the rise in energy usage will be offset by more efficient equipment resulting in no net increase in energy usage. This view is also shared by Nokia, who also, in 2017 found that existing site equipment renewal delivered efficiencies of 44% which are expected to offset any increase.

On the other hand, other stakeholders believe that the energy consumption of wireless networks will initially fall before picking up again. Huawei estimates that energy consumption will fall initially until “around 2021” (MDPI report). However, in the same way, 5G data traffic (and network deployments) increase, so does energy usage. They calculate this increase to be at a rate of 5% p.a. from 2022 until 2025. Even this value is contingent on a breakthrough in “efficient 5G technologies”, a delay of which could see global energy usage increasing by an additional incremental 30%.

In addition to the data load question, i.e., equipment will be able to handle more bandwidth with the same or lower energy consumption, this does not address the increase in cell sites with Huawei pointing to a doubling of network energy consumption. It is worth highlighting that issues of power capacity at existing sites, may also affect CAPEX and deployment times.

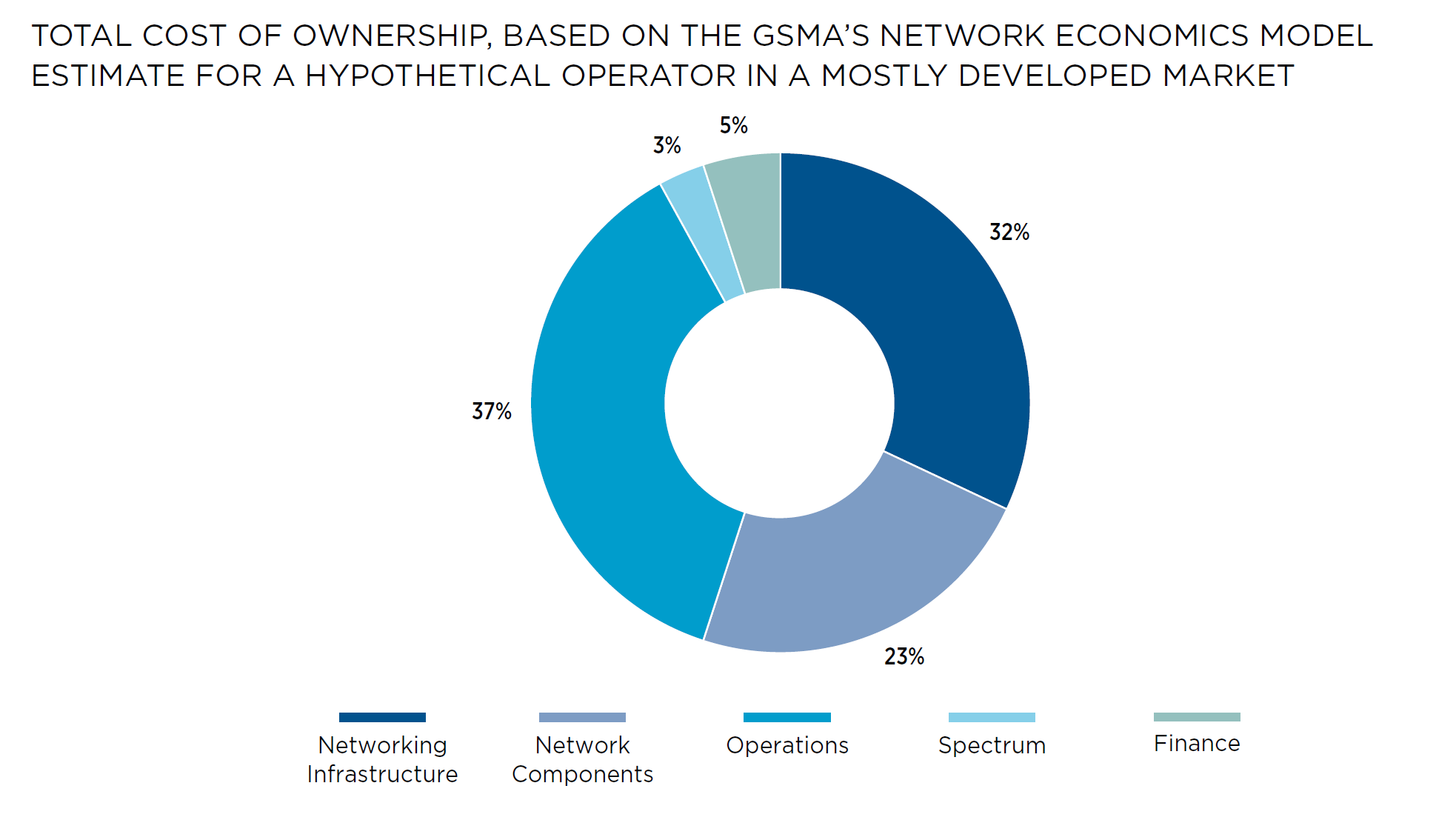

Figure 2 highlights the cost contributions and total cost of ownership (TCO) for a hypothetical operator in a developed market. It is based on the GSMA’s Network Economics Model and has been designed to support operators in understanding the critical value levers to deliver lower TCO.

Figure 2

Key drivers in the case for energy

Energy is a crucial consideration for the following reasons:

- 20-40% of network OpEx – for many operators RAN and base stations make up much of this, and cost reduction is a key driver

- Stagnating revenues in many markets and clarity around revenue opportunities meaning cost reduction is a key priority

- Energy increase in 5G, while the jury is still out on just how much this energy increase may be through densification and increased traffic demand, what’s clear is many operators will maintain a 2G, 3G, 4G and 5G networks (GSMA, 5G report)

- Carbon energy market volatility, cost of carbon-based energy is affected by geopolitical events

- Cost reduction in renewables – 90% reduction in PV cost in last ten years, further 50% in the next five years (IRENA report?) Cost of wind turbines has fallen 37-56% and PVs by 80% in last 10years? (check IRINA 2018b). Cost of renewables cheaper than the grid in many markets – price parity

- Climate change – Paris Agreement’s objective of keeping the rise of global average temperatures to well below 2 degrees Celsius above pre-industrial levels

- Corporate sustainability of growing in importance for consumers and investors

Scope

The scope is network infrastructure:

Out of scope:-

- Operational infrastructure (offices, factories, fleets, supply chain)

- End-user consumption

- Device-level efficiency

- Equipment components (e.g. processor efficiency)

- Supply chain efficiency

- Regulatory matters

Sourcing

Sourcing refers to where energy supply is can be obtained either directly or using conversion or transformation, for example, solid fuels, liquid fuels, solar energy, and biomass.

The traditional approach for legacy networks has been to use grid-supplied energy as a primary power source, and main supply of energy is conventional grid supply were available with diesel generators providing back up power, or often as a primary power source in a bad-grid or no grid scenario.

A growing number of operators have taken a leading role in sustainability, and the use of renewables to meet or exceed these decarbonisation goals and these will expand in the 5G era. The many solutions to enhance network energy efficiency fall into two major groups: increasing the use of alternative energy sources to reduce dependence on the primary power grid; network load optimisation to reduce the energy consumption.

Grid energy

For over 100 years, coal and other fossil fuels have been used by power plants to produce the electricity we use every day. The grid is a network of powerlines and substations that carry electricity from powerlines to homes and businesses. In many markets, the grid faces many problems, including the need to update and capacity issues. When powerlines break or power stations cannot produce enough power, blackouts can occur, which can have significant economic and social impacts.

Traditional grids are often reliant upon a single power source and often lack detailed information on usage, making electricity challenging to manage. To address these problems in the past, utility providers have built more power stations to deal with the demand thus addressing any shortfall. It is worth noting, in many markets, utility providers are working towards sustainability and reducing their reliance upon traditional carbon-based fossil fuels by moving to alternatives such as nuclear energy or renewables adding stability and efficiency while improving their “energy mix”.

In doing so businesses and consumers, can purchase cleaner energy directly through green tariffs, often at a premium, facilitating decarbonisation strategies.

Smart Grids

The smart grid means adding sensors and software to the existing grid giving new information to utilities and individuals to help them understand and react to changes in supply quickly. For example, if a tree falls on a power line and 1000 homes lose power, with the current grid, utility engineers often physically reroute power, taking time. With a smart grid, sensors and software would detect and immediately re-route power around the problem, limiting the issues. Also, the price of electricity changes throughout the day, but we can’t see it with the current metres, it may be experienced in the peak hours and cheaper in off-peak hours. The installation of new smart meters at home, driving consumer behaviour provided more predictability around usage and also pricing.

The smart grid is being rolled out in many markets, but soon we’ll be able to make a more informed decision of usage.

TESCOs & IESCOs

A crucial driver of the conversion to greener alternatives will be Energy Service Companies (ESCOs) that provide energy to towers owned by Mobile Network Operators (MNOs) and dedicated Tower Companies (TowerCos). [1]Many MNOs across the world, especially in Asia and Africa, are in the process of selling off their tower assets, including the energy infrastructure, to third-party structures. This trend, brought on by a strong imperative to cut network deployment and operating costs, is expected to intensify in the 5G era. In a rapidly evolving tower energy landscape, that requires a high degree of customisation across multiple tower sites and specific technical expertise, MNOs are not best-positioned to drive energy efficiency. Moreover, MNOs have an incentive to reduce the complexity of non-revenue generating operations like power, to focus on revenue-generating parts of their business. MNOs place a priority on expanding networks and upgrading technology of active equipment.[2] With limited funds for CAPEX, MNOs will always favour investments in existing radio equipment over investments in energy solutions. There are two types of ESCOs in the market today, each facing specific challenges related to the transition of the industry to greener tower energy solutions:

TowerCo ESCOs (TESCOs)

These are TowerCos that generate and provide electricity to their MNO tenants at telecom tower sites. TESCOs typically bundle their energy services with other standard functions of dedicated TowerCos (e.g. site security, monitoring of active equipment and upgrade of passive infrastructure), and charge an all-inclusive fixed monthly fee for all rendered services. Critically, TESCOs own, operate and bear all operating costs for the tower’s energy assets. Because energy generation and provision can constitute up to 60% of all annual operating expenses, TESCOs are incentivised to continuously seek long-term opportunities for energy efficiency, energy cost reduction, and cost predictability. Their primary challenge is that historically, TowerCo and MNO contracts are structured to provide TowerCos with little or no commercial or business incentives to prioritise energy cost reductions and energy efficiency, i.e. they had incentives to be TESCOs. While the contracts have now reversed, inertia remains that work against greater adoption green and renewable energy solutions, even though on paper they promise substantial cost reductions.

Independent ESCOs (IESCOs)

These are dedicated or pure-play energy companies that own and operate energy assets at power telecom tower sites. IESCOs derive revenues from selling energy to MNOs as well as dedicated TowerCos,6 and share similar incentives as TESCOs to reduce energy costs by upgrading energy assets. Financing new energy generation assets, primarily through debt financing at viable interest rates is the primary challenge facing IESCOs today. The small size and low asset base of existing IESCOs and those looking to enter IESCO market, has proved particularly limiting when banks evaluate funding applications. Also, banks often have an incomplete understanding and experience of IESCO business models, and often lack effective frameworks to assess funding needs and requirements. As the drive to decrease telecom tower energy costs gathers momentum over time, TESCOs are expected to develop appropriate contract management structures in their dealings with MNOs, which would offer clear incentives for energy efficiency, innovation and cost reductions. This transition is already underway in key markets. For example, in India, TowerCos, which currently comprise about 60% of the total market of 400k telecom towers, have switched from almost universally deployed ‘pass-through’ models to fixed-fee contracts with their MNO tenants, all in the past 2-3 years.

Renewables

Operators are increasingly shifting their energy sourcing away from carbon sources towards green renewable technologies and alternative energy sources, such as photovoltaic modules and fuel cell generators as their cost continues to fall. Such non-carbon energy sources can exempt an operator from the burdens of carbon emissions regulation and enable the networks to be more resilient to natural disasters or power outages.

The optimal choice of renewable energy will differ depending on the context of the operator (e.g., fossil fuel costs in the nation, power outages, carbon emissions regulation), but alternative energy source solutions can be cost-effective. This is important because energy costs from the central grid or by energy generators with fossil fuels is a primary concern for operators: the former because the electricity needs depend on the utilities and the latter because carbon emissions are being regulated/taxed by some regulators.

Increasingly companies are turning to renewables for their energy requirements, which have primarily been as a result of massive reductions in the cost of renewables coupled with a more conscious drive to corporate sustainability from investors and consumers[3].

Decreasing costs in Renewables tech

The pace of renewable energy deployment in recent years has been remarkable, a report by IRENA (International Renewable Energy Agency)[4], estimates that it must be accelerated at least six-fold to meet the climate goals and achieve the necessary decarbonisation of the energy sector by 2050.

Findings from this report indicate that companies actively consumed approximately 465 terawatt-hours (TWh) of renewable electricity in 2017; this is comparable to the entire electricity consumption of France.

Corporate sourcing of renewables has the potential to drive significant additional investment in renewable energy. With the right framework in place, it can help to accelerate the energy transformation and move the world closer to achieving the Paris Agreements’s objective.

Non-energy producing companies are increasingly turning to renewables as their preferred energy choice. In addition to cutting emissions, the economic benefits os sourcing renewables often cost include cost savings, long-term price stability and security of supply.

Renewable energy is now the cheapest source of power generation in many parts of the world and investment in renewable energy is outpacing that of conventional energy. The cost of wind turbines has fallen by 37 to 56% (IRENA, 2018b)[5] and that of solar photovoltaics (PVs) by approximately 80% (IRENA and IEA, 2017)[6]

Renewable electricity sourcing occurs across a broad range of companies. Although the most significant industry to report renewable electricity consumption is the Industrial Sector (238 out of 531, presenting 45% of company reporting data), it is the Telecommunication Services sector that has reported the largest proportion of companies sourcing renewable electricity (46 out of 72, presenting 64% in companies reporting data). Moreover, it is the IT sector that is pioneering some of the most innovative corporate sourcing models, including different forms of PPAs, entered into to supply operations such as data centres.

Models for corporate sourcing of renewables

Operators have several options for alternative energy sourcing. First, operators may purchase green energy directly from their utility provider (often at a premium).

Second, they can use energy attributes certificates (EACs), which allow an offset of energy consumption through equivalent renewables-based certificates.

Third, a third-party power purchase agreement (PPA) as a means to shift supply to renewables without the initial CapEx investment, agreeing to purchase energy from the solar or wind farm at a specific rate for a particular period, e.g. 5-20 years.

Lastly, operators can self-generate energy either at the base station with standalone or hybrid solar-based solutions, (which may extend to off-grid scenarios); or with large-scale solar and wind farms, requiring CapEx investment. For base station, energy solutions see later section on energy saving.

Unbundled energy attribute certificates (EACs).

- A company purchases attribute certificates of renewable energy separately ‘unbundled’ form its electricity. Example – Guarantees of Origin (GO) and renewable energy certificates (RECs).

- An EAC is a contractual instrument that represents information about the origin of the energy generated. It allows markets to track renewable energy production and permits consumers to make credible claims of renewable energy use.

- The best practice is considered to be the sourcing of certificates within the geographical region where a company’s electricity purchasing takes place.

- Prices for EACs vary depending on local supply and demand, technology, locational attributes, and contract length.

- Advantages of EACs are flexibility, simplicity and lower operational risk

- Disadvantages are the low average price of unbundled EACs tend to cast doubt on the extent to which trading them in will help to support existing or create new additional capacity.

Power Purchase Agreement (PPA).

- A company enters into a contract with an independent power producer, a utility or a financier and commits to purchasing a specific amount of renewable electricity, or the output from a particular asset, at an agreed price and for an agreed period.

- The typical duration of a PPA for a newly built project is ten years or longer. However, the term can vary between sectors and locations.

- PPAs are an option for companies to lock in a cost-competitive price.

- Virtual PPA is a contract where the renewable energy generator sells its electricity in the spot market and then settles the price based on the difference between the variable market price and the strike price with the company who receives the associated EACs

- Sleeved PPAs are where the renewable energy generator sells the electricity and related EACs directly to a company.

- In 2017, a record level of new corporate PPAs was reached, with over 5 GW of capacity contracted, this was predominately in wind and solar projects. This is almost an increase of a third on 2016 numbers. (RMI, 2018)[7]

- PPAs often include energy storage to ensure reliability and security of supply.

Examples:

- Telefonica Mexico Case Study

- Orange Jordan Case Study

- AT&T Blog

Renewable energy offerings form utilities or electric suppliers.

- A company purchases renewable electricity from its utility either through green premium products or through a tailored renewable electricity contract, such as a green tariff programme.

- Green premium products enable corporate buyers to conveniently purchase renewable electricity directly from the utility without a long-term commitment.

- Utility green tariffs (also known as renewable utility contracts) are longer-term agreements whereby customers purchase renewable electricity bundled to a specific renewable energy asset.

- The telecommunication Service sector purchases 40% of their electricity through various utility contract.

Production for self-consumption.

- A company invests in its own renewable energy systems, on-site or off-site, to produce electricity primarily for self-consumption.

- In Direct investment in self-generation, the company is responsible for the entire project life cycle, from commissioning, assuming the associated risks and financing responsibilities

- Alternative models can involve a third party developer installing an on-site system for a self-generation under a lease contract, thus limiting the end users risk.

- Direct investment for self-generation takes place in almost every country that permits some form of grid connection at a rate of compensation (through net metering or feed-in tariff scheme.

- Other examples of direct investment for self-generation include companies with agricultural by-products capable of producing biomass or biogas, such systems allow direct control over the conversion of waste products into energy.

- Most commonly, self-generation projects are located on-site; however, in some cases, electricity is generated off-site and transferred either physically or under a financial contract to the end-user.

- For off-site projects, transmission or wheeling charges may apply, if access to transmission assets is required to deliver the electricity to the sites.

- Sourcing trends indicate that direct investment will increase its share in the coming years as the cost of renewable energy systems continues to decline and companies continue to source renewable electricity more directly.

Storage

Energy storage is the answer to balancing intermittent generation – the capture of energy produced at one time to be used at another. Common examples of usage in mobile networks are largely battery and fossil-based generators, though more recently this is shifting to alternative technologies, e.g. fuel cells.

Batteries

Innovation in battery tech is advancing at a rapid pace, but the elusive high capacity, long-life; the super battery is yet to be discovered. Batteries are particularly valuable because they offer sub-second frequency response – that is if there is a failure of power, batteries can instantly take over. However, this is often for a short period, usually 4-6 hours. The scaling of other industry such as the electric vehicle (EV) and photovoltaic (PV) or solar panel markets are helping to reduce costs. Batteries are By controlling the batteries exposure to heat; you can lengthen the life cycle and keep your battery running like new.

Lead Acid

While the use of smart (or electronic) batteries has been increasing in recent years, lead-acid batteries remain the industry standard used for storage in backup power supplies in cell phone towers, high-availability settings like datacentres, and stand-alone power systems.

VRLA

VRLA is a replacement for the traditional flooded lead-acid battery. In valve regulated lead acid (VRLA) batteries, hydrogen and oxygen produced in the cells largely recombine into the water – retaining moisture within the battery. VRLA batteries are often referred to as maintenance-free as they do not require regular checking of the electrolyte level. However, this is somewhat of a misnomer. VRLA cells do require maintenance. As the electrolyte is lost, VRLA cells “dry-out” and lose capacity, which can be detected by taking regular measurements to determine whether further action is required. New maintenance procedures have been developed allowing “rehydration”, often restoring significant amounts of lost capacity – this should be checked in conjunction with supplier warranty.

Different types of batteries have been developed to overcome this leakage, e.g. gel cell VRLA batteries, which add silicate to ensure efficacy. However, these are often at a premium and have challenging charging processes.

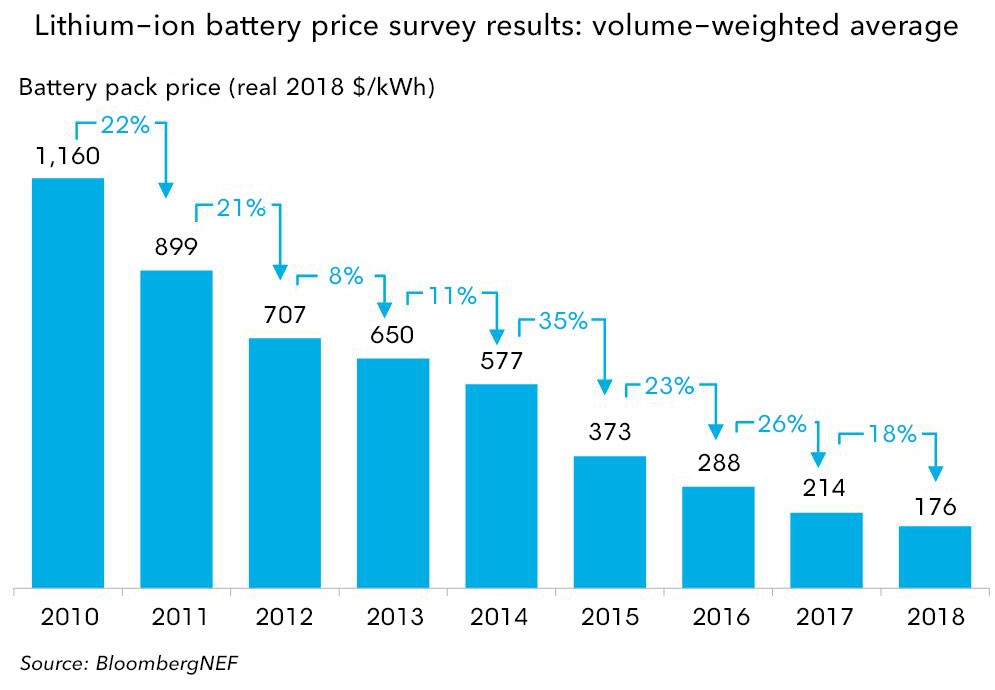

Lithium Ion

The lithium-ion family receives the most attention and is gradually replacing the lead-based predecessors that dominated the battery world.

Li-ion is presently more expensive than lead-acid; however, when calculating the price-per-cycle, it is superior to lead acid when repeat cycling is required and basing calculations on cost per kilowatt hour (kWh) no longer holds; operational costs must be considered.

Developments in EV and PV sectors are significantly reducing the cost of lithium-ion, which has fallen dramatically – over 80% since 2010.

Figure 3

Future developments

The pace of demand in battery tech drives constant innovation that either enhance or could potentially replace existing solutions. These include graphene, solid-state and ultrafast charging, which may provide a step-change in capabilities. When adding timelines to tech adoption, it takes an estimated 4-5 years for new technologies to be fully commercialised, so it is not expected that solid-state batteries to make a meaningful contribution to the global EV market until the late 2020s at the earliest.

Generators (back up and primary source)

Diesel

Diesel Generators often referred to as generator sets or “gensets” are one of the most economical ways to generate electricity and are often relied upon as a backup power once batteries have become depleted or as a primary power source in off-grid/bad grid scenarios. Proper dimensioning and sizing of diesel generators is critical to avoid low-load or a shortage of power, which is particularly challenging with modern electronics and non-linear loads.

Generators can be adapted to support Liquid and natural gas.

Fuel Cells

A fuel cell is an electrochemical energy conversion device that produces electricity by combining hydrogen and oxygen into water. Like batteries, fuel cells convert potential chemical energy into electrical energy and generate heat as a by-product. However, the chemical energy is stored inside batteries—rather than generated— they can only operate for a limited duration until they need to be discarded or recharged. Fuel cells, on the other hand, can continuously generate electricity subject to sufficient fuel supply (e.g. hydrogen) and an oxidant.[8]

Hydrogen distribution is an issue, and alternative fuels such as methane and ammonia have been explored as an alternative which can overcome safety and cost concerns.

Energy efficiency in Networks

Network load optimisation is essential to ensure a reduction in total energy consumption. This is a prescient requirement for 5G era networks. Improving energy efficiency to consume less energy can be achieved through a multitude of solutions, including smart building, virtualising the core, and enhancing RAN efficiency through modernisation of legacy equipment and implementation of low-powered solutions.

While existing core networks enjoy the benefits of having well-established energy management systems (including remote management systems), the critical elements for access network infrastructure such as power systems, batteries, air conditioners, free cooling and generators (gen-sets) often do not come with holistic, well-developed energy management systems.

Remote monitoring and automation of management functions for the main site infrastructure elements allow operators to identify CapEx and OpEx reduction opportunities and develop energy efficiency strategies. Further energy efficiency gains will also come from network automation and using shared network infrastructure.

Saving

The many solutions to enhance network energy efficiency fall in two major groups: increasing the use of alternative energy sources to reduce dependence on the main power grid, and network load optimisation to reduce the energy consumption.

The following solutions are considered a means to improve energy consumption in networks in addition to the backhaul, infrastructure and automation online documents which by their nature, reduce energy consumption.

Ran Infrastructure Modernisation

As technology advances, developments in new tech can bring a significant reduction in energy consumption. However, ran infrastructure modernisation often requires high CapEx investment, coupled with long break-even time. Ran modernisation is usually executed with other scenario change (Vendor band, technology, format, refarm, and others). However, this can “hide” OpEx increases related to additional tech-band support.

Lightweight base station

Recent developments in free air cooling and outdoor sheltering are now evolving into deployments of light-weight base stations, coupling limited coverage and capacity with low power, renewably sourced solutions, deployed at a fraction of the cost benefiting, in particular, rural connectivity scenarios.

Moving radio power equipment to exterior shelters

The relocation of equipment from interior sites to exterior shelter reduces the HVAC energy consumption, usually executed during modernisation projects.

Installing Free Cooling Equipment

The commissioning of free air cooling can reduce the AVAC and in some climates can prove very useful to address only the heat aspect. Free Air Cooling requires moderate CAPEx investment and mostly applicable if external cooling is available most of the year and only valid if external cool air is available most of the year

Pure software /Self-optimising network solution

Intelligent site connectivity

With the addition of intelligent connectivity through software and IoT sensors at a base station or other infrastructure sit, more significant data can be captured which can drive intelligence, for example, in site power consumption, maintaining cooling, battery life cycle management.

Alternative Energy Sources

See section on sourcing.

Other power strategies and solutions

- A good example is CommScope Powershift dynamically voltage adjustment system, interesting for new deployments.

- Partial integration of alternative power systems, like solar panels can be attractive as the cost is lower than the total of a grid-like supply, though, retrofitting may be somewhat complicated depending on existing configurations

- Higher efficiency rectifiers though most modern rectifiers achiever 95%+ efficiency

- Tight battery ageing control (old-lead acid batteries burn energy)

- Migration to Lithium Ion/alternative energy storage solution

Energy Recovery

Heat

While ICT and telecoms technologies continue to become more efficient, the facilities that support them have been traditionally energy intensive. To take advantage of this, designers and engineers need to adjust how they approach hot air conditioning – thinking in terms of heat recovery, as opposed to cooling. The application of waste heat recovery is impacted by two significant obstacles: the size of the installation and the physical distance to facilities which could utilise the recovered heat.

Datacentre heating

Data centres can consume large amounts of power and generate significant waste heat, often more than is required by to heat a typical office building and so are often coupled with a central campus or increasingly, municipal district heating projects[9].

Please sign in above to make comments or edits to this document. To sign up for our newsletter, please click here.

[1] https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2015/01/140617-GSMA-report-draft-vF-KR-v7.pdf

[2] Core radio equipment (including equipment) that is responsible for broadcasting mobile phone signals to users. Passive infrastructure, on the other hand, includes the non-electronic equipment including the tower itself, energy infrastructure, etc.

[4] IRENA (2018), Corporate Sourcing of Renewables: Market and Industry Trends – Remade Index 2018. International Renewable Energy Agency, Abu Dhabi.

[5] Renewable Power Generation Costs in 2017, https://irena.org/-/media/Files/IRENA/Agency/Publication/2018/Apr/IRENA_Report_GET_2018.pdf

[6]Perspectives for the energy transition – investment needs for low-carbon energy system ©OECD/IEA and ORENA 2017, https://irena.org/404?item=%2fpublications%2f2017%2fmar%2fperspectives-energy-transition-investment-needs-for-a-low-carbon-energy-system&user=extranet%5cAnonymous&site=IrenaLivehttp

[7] RMI (Rocky Mountain Institute) (2018), Corporate Renewable Deals 2013 – 2018 YTD, https://businessrenewables.org/?s=corporate+transactions

[8] https://www.gencellenergy.com/gencell-technology/what-is-a-fuel-cell/

[9] https://www.siliconrepublic.com/enterprise/stockholm-heat-data-centres