Mobile money has become a vital tool for vulnerable populations in low- and middle-income countries (LMICs), revolutionising how they save, invest, spend and manage their financial lives. According to the GSMA’s State of the Industry Report on Mobile Money (2024), it has also driven progress towards the UN’s Sustainable Development Goals (SDGs), enabling households to lift themselves out of poverty. However, in countries like Sri Lanka, where traditional banking services are widely available with 89% of the adult population owning accounts (Findex 2021), the uptake of mobile money has been slower, limiting its potential impact.

While mobile money can be accessed through basic feature phones, its true potential lies in the advanced functionalities offered by smartphones. These devices provide a more seamless and user-friendly experience, and can unlock additional, potentially life-enhancing features and services, such as access to education and healthcare. However, as mobile money providers shift to developing smartphone “super apps”, there is a risk of excluding individuals who cannot afford these devices This oversight of the potential business opportunities that could be generated from serving low-income customers could result in significant revenue losses for mobile network operations (MNOs).

The rise of fintech apps has added another layer of complexity. With diverse financial services and sleek interfaces, these apps are intensifying competition in the digital finance landscape and making affordable smartphones vital. Smartphones not only offer enhanced user experiences but also expand access to mobile money services. When they are affordable, there is a better chance of bridging the digital divide and empowering more individuals, regardless of their economic status, to actively participate in the digital economy. This digital divide calls for urgent, innovative solutions that make smartphones more accessible and affordable for everyone.

Smartphone device financing is one way to bridge this gap and promote financial inclusion. By offering smartphones financing options, individuals previously excluded from the digital revolution can participate and benefit from all the opportunities mobile money offers. Led by a diverse coalition of stakeholders, these initiatives are pioneering efforts to increase smartphone access and drive the uptake of mobile money.

Several device financing programmes have been introduced by mobile network operators in LMICs. Some of these include Lesi Pay, launched by Dialog in Sri Lanka in 2015; Lipa Mdogo Mdogo, introduced by Safaricom in Kenya in 2020; and Easy2Own, rolled out by Vodacom in South Africa in 2021.

Dialog’s Lesi Pay offers financing various mid-range to high-end smartphones, while Safaricom’s Lipa Mdogo Mdogo and Vodacom’s Easy2Own provide financing options for entry and mid-range smartphones. These programmes are typically accessible, flexible and bundle services like data plans or device insurance for added value.

Some device financing providers also provide warranties and repair services. For example, Safaricom’s Lipa Mdogo Mdogo ensures that all devices have a one-year warranty with after-sales repair centres spread across the country.

Mobile money is a cost-effective way for service providers to collect loan payments for devices given the low transaction costs involved. And, since mobile money is accessible to a broad population segment, service providers can leverage it to offer more digitally and financially inclusive services. This is especially important for customers who live in rural areas and far from service centres, as using mobile money is much more convenient than travelling to make loan payments in cash.

Service providers also benefit from real-time transaction settlements, as they avoid the inevitable delay associated with cash payments and can quickly activate device locking if a payment is not made on time. Mobile Network Operators (MNOs) often benefit from increased mobile money uptake by new device financing users. In Kenya, M-PESA’s immense reach and scale allows Safaricom’s Lipa Mdogo Mdogo to accept all loan repayments through mobile money.

However, in South Africa, where mobile money adoption is low due to the high banking penetration, Vodacom’s Easy2Own leverages bank payments for device financing. Monthly loan instalments are deducted from a customer’s bank account on an agreed date. Of the three MNOs mentioned here, only Vodacom offers standing order debit payments via banks and mandates them as the only repayment method for devices.

As with Safaricom’s Lipa Mdogo Mdogo or Vodacom’s Easy2Own, a user must be an active customer of an MNO for at least one year before they qualify for device financing and satisfy credit scoring criteria. However, such requirements can exclude a significant number of people and MNOs should consider offering device financing for more recent customers, too.

Overcoming barriers to mobile internet access

There is still a long way to go to improve mobile internet access. According to the GSMA State of Mobile Internet Connectivity Report 2023, around 3 billion people, or 38% of the global population, live in areas with mobile broadband coverage but are not connected to the mobile internet. Two-thirds of these do not own a mobile phone.

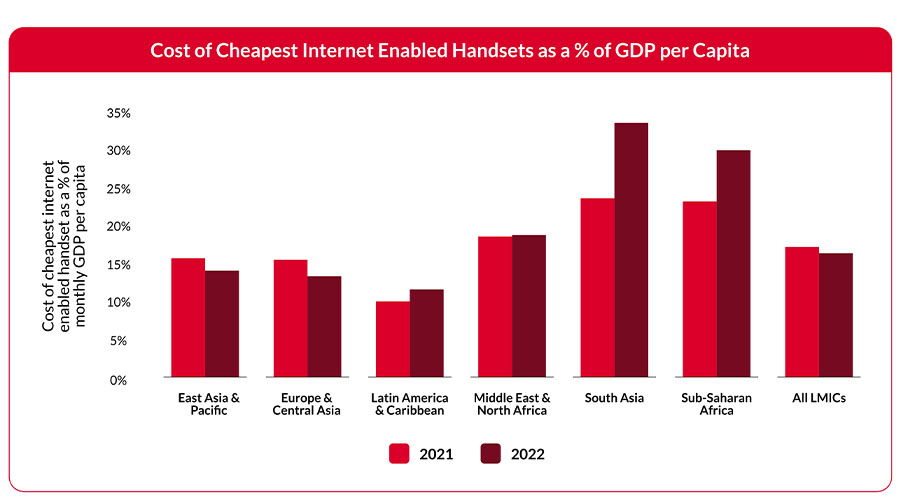

Cost of the cheapest internet-enabled handset as a % of monthly GDP per capita (GSMA Intelligence)

One of the most significant barriers to global mobile internet adoption is the affordability of internet-enabled handsets. Individuals in various regions cited affordability as the main reason why they do not access mobile internet services. Customers in Latin America, South Asia and Sub-Saharan Africa have all seen internet-enabled handsets become less affordable due to inflation, economic crises and supply chain disruptions. The situation is particularly pronounced in South Asia, where multifaceted economic challenges have compounded the issue.

Urban-rural disparities exacerbate the digital divide, not only in terms of smartphone ownership but also adoption rates. While smartphone ownership has surged in urban areas, rural communities continue to lag, perpetuating inequalities in access to information and opportunities. The GSMA State of Mobile Internet Connectivity Report 2023 highlighted these disparities, revealing significant differences in smartphone ownership rates.

Gender disparities also compound digital exclusion: women in South Asia were 41% less likely than men to own a mobile phone in 2022. The affordability gap is particularly wide, with entry-level handsets consuming a higher proportion of women’s monthly income compared to men. Coupled with low employment rates among women and gender pay gaps, there is an urgent need for gender-sensitive interventions to promote digital inclusion.

Device financing models for digital inclusion

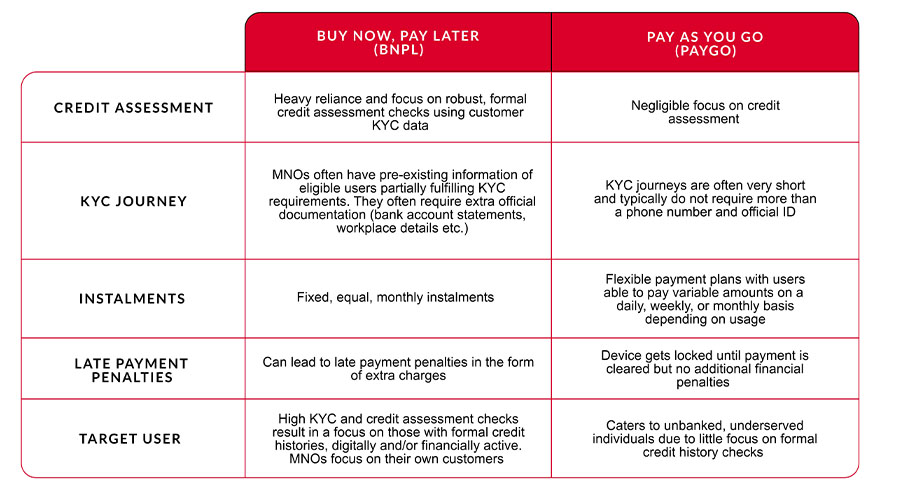

To address these challenges, various device financing models have emerged, offering pathways to affordable smartphone ownership for underserved populations. The buy-now, pay-later (BNPL) and pay-as-you-go (PAYGO) models are two approaches, each with its unique features and eligibility criteria.

In the BNPL model, users make an initial down payment and pay the remaining amount in instalments over a specified period. This model relies on credit assessment algorithms to determine users’ creditworthiness based on their usage patterns and bill payments. While BNPL models offer flexibility and convenience, they may require users to have a formal credit history, potentially excluding underserved populations.

The PAYGO model, on the other hand, provides devices to applicants with minimal credit checks, relying on built-in, device-locking technology to mitigate the risk of default. Under this model, devices serve as collateral, with users gaining full ownership once they have made all the payments. While PAYGO models cater to unbanked populations and those with irregular income streams, they may have higher upfront costs and interest rates to offset the risk associated with minimal credit checks.

Differences between the BNPL and PAYGO device financing models

Eligibility criteria for device financing schemes varies depending on factors like age, customer status and minimum time as a customer. While some impose age limits and require users to be existing customers, others are more inclusive, welcoming first-time customers and those with limited credit history.

Credit assessment methods also vary across financing models, with traditional lenders relying on extensive background checks and the BNPL/PAYGO providers using alternative data sources such as mobile usage patterns and mobile money transactions. While traditional lenders prioritise credit history and collateral, BNPL/PAYG models focus on affordability and usage behaviour, opening access to financing for underserved populations.

Device financing programmes must ensure a range of devices are available to meet the needs and preferences of different users. Entry-level smartphones are popular among new users due to their affordability and basic functionality, while mid- to high-range smartphones appeal to more digitally proficient users. By offering a wide range of devices, financing programmes can be more inclusive and address the diverse needs of underserved populations.

To promote digital inclusion and empower underserved communities, device financing programmes must also adopt targeted marketing strategies, expand low-end smartphone offerings and implement flexible repayment terms. Education on the value proposition of devices and mobile internet, along with enhanced after-sales support, can further empower users and bridge the digital divide.

Smartphone financing can potentially fuel mobile money growth, makes smartphones accessible and drives financial inclusion. For low-income populations, models like BNPL and PAYG may help to overcome the access, usage and affordability barriers. By empowering users and providing flexible repayment terms, smartphone financing can create a more equitable digital landscape.

For MNOs, the future of mobile money hinges on adapting to the changing fintech landscape while enhancing access to smartphones. Addressing these challenges through innovative solutions like device financing can unlock the full potential of mobile money and pave the way to a more inclusive and prosperous future.